Is the Fed's plan changing?

A brief view of their comments + analysts forecast for next year

US stocks and bonds ended higher on Wednesday while the dollar closed at its weakest level since August after the Federal Reserve’s latest meeting minutes showed most officials backing slowing the pace of interest-rate hike soon, a prospect that has given some support following the release of weaker than expected economic data.

But did the Fed minutes actually show a possible change of plans?

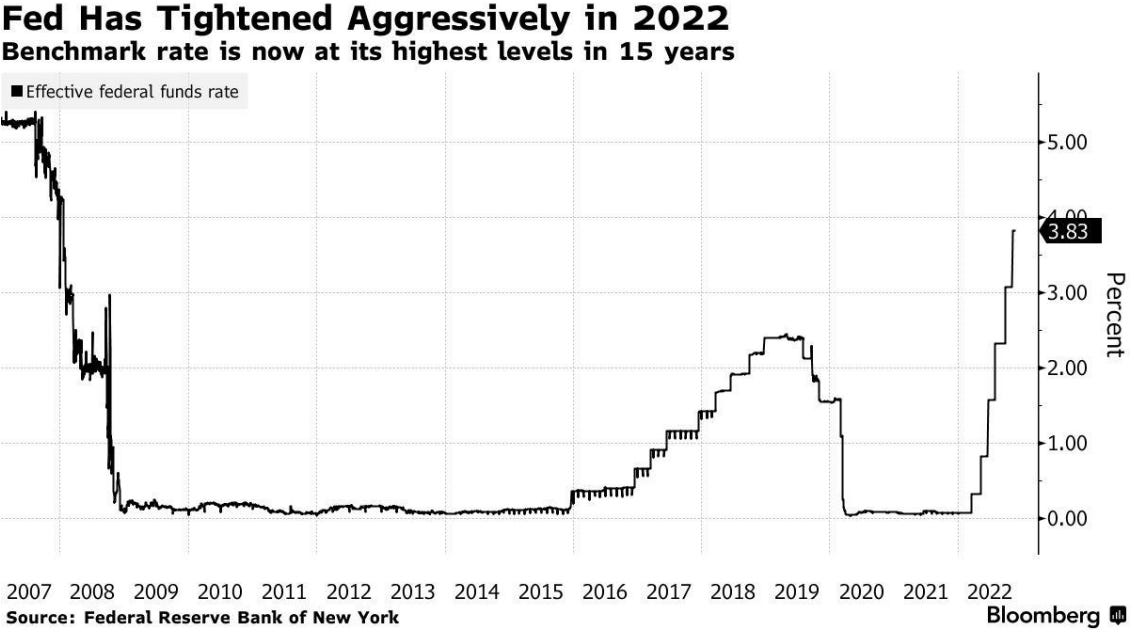

Interest rates

Basically, Fed minutes reiterated the same concept of the last meeting: slower hiking, but higher peak on a longer time window.

“Various officials had concluded that rates would ultimately peak at higher level than previously expected”.

This decision will help Fed to see and study the effects of rates on the economy.

Growth

Fed economists saw the odds of the US entering a recession in the next year as almost at 50%. Market read this view as a positive message (bad news are good news), as it could mean that they will be less hawkish. We indeed have some signals of declines, for example the increasing requests of unemployment benefit, or the SPX Global composite business activity index under 50 level:

But other data show that macro cycle is enduring. Unemployment rate is at a near match of a 50-year low and firms are confident for the future demand as core capital goods orders are increasing.

Bank of America, 2023 forecast and strategy

BofA economists and strategists forecast mild recession in 2023, lower inflation, stronger China, peak rates, yields, spreads, USD, oil prices, flat US stock prices and a very positive year for gold and base metal prices.

By the numbers:

Mild recession. US GDP -0.4% after 1.8% in 2022

Lower inflation. US CPI 4.4% from 8.1%

Higher unemployment. U-rate jumps from 3.7% to 5.5%

Stronger China. COVID reopening sees GDP growth 5.5% up from 3.0%

Peak Fed funds. Peaks 5-5.25 % In March and then Fed cuts 25bp in December

Peak yields. US Treasury 10-year yield drops from 4% to 3.25%

Peak credit spreads. US IG spreads to tighten to 130bps

Peak US dollar. Euro rallies to 1.10, Japan yen to 137, China yuan to 7.00

Peak oil prices. WTI oil forecast to peak at US$ 104/bbl in Q323

Higher gold prices. Gold to rally to US$ 2000/oz

Flat US stocks. S&P 500 year-end 2023 target is 4000

We stay bearish risk assets in H1, likely turn bullish H2; market narrative to shift from Inflation and rates "shocks" of 2022 to recession and credit "shocks" in H123, thereafter more bullish story of "peaks" in inflation, Fed funds, bond yields and US dollar in H223.

We are long US government bonds in H1. Hard landing and credit event risks under-priced; maintain view optimal S&P500 entry points. Nibble at 3.6k, bite at 3.3k, gorge at 3.0k.

We believe June/July 2023 Fed pivot just before US$ 1.6tr of US corporate refi begins and only after interest rate tightening visibly hurts Main St (housing and credit markets force unemployment higher) = most bullish outcome for Wall St; easing financial conditions from mid-year = new bull market stocks and corporate bonds in H223 and 2024.

2023 set-up into 2023 less bearish than into 2022; bear market in bonds and stocks means much greater investor pessimism versus year ago; and it is unlikely central banks hike rates another 280 times in 2023; BofA expected returns cautiously positive. Copper >25%, gold 15-20%, US IG 12-13%, 10-year Treasury 7-8%, oil 5-6%, cash 5%, US stocks 0%, US dollar -6%; strongest returns in "peak USD" and inflation hedges of commodities and EM assets.

Top 10 Trades for BofA:

Long 30 year US Treasury. On recession, unemployment, Fed cuts late 2023, history (US Treasury returns have never fallen for 3 consecutive years).

Yield curve steepeners. As US yield curve always steepens as recession begins and markets anticipate Fed flipping from hikes to cuts.

Short USD, long EM assets. Long EM distressed bonds, Korea won on China reopening, Mexican peso on "nearshoring".

Long China stocks. COVID reopening was bullish for US/EAFE stocks, China has high "excess savings" and China stocks remain contrarian long trade.

Long gold and copper. USD peak, China reopening, metal inventory shortages, energy transition acceleration, need in 2020s for inflation hedges.

Barbell credit. Long credit too consensus in 2023, we barbell long IG tech bonds (>5% yield + strong balance sheets) with distressed HY debt in Asia (17% yield).

Long global industrials and small cap stocks. Secular leadership shift in 2020s from deflation to inflation assets, driven by globalization to localization, monetary to fiscal excess, inequality to inclusion and so on just beginning; capex set to be new macro bull story.

Short US tech. The old leadership, still over-owned, era of QE is no longer, era of globalization no longer, plus peak penetration and regulation risks.

Short US private equity. The old leadership, redemption risks given shadow banking exposures to housing and credit risks.

Long EU banks, short Canada/Aussie/NZ/Sweden banks. EU fiscal stimulus to wean Eurozone off Russian energy dependence, Chinese export dependence, US military dependence vs real estate market busts in Canada/Australia/NZ/Sweden.

Other analysts comments

TS Lombard's Steve Blitz on his 75bps scenario in December: "..activity looks to be rebounding back to an above-trend pace – because money is still cheap and labor is still strong....Anxious to slow, even to stop (they dare not convey that just yet), they even pulled out the global economy and potential financial fragilities (r** enters the conversation) as reasons. No one mentioned that even a scaled back Taylor rule pegs the funds rate at 7.9%. Slowing eases financial conditions. Fed goes 75BP in December, and they will rue the day if they don’t”.

Sanctions won't end...even should the war end. TS Lombard with a not so rosy outlook:

Europe is facing a half decade of a relative loss of competitiveness, with the worst probably yet to come – in the winter of 2023-24.

The exit from this predicament is not an event but a process – of accelerated energy transition, with hard choke points to be overcome.

The imminent playing out of the Russian oil price cap gambit exemplifies this harsh reality for Europe.

Even if the war really does end definitively on a investment-relevant time horizon, the economic break with Russia reflected in sanctions will remain irreparable.

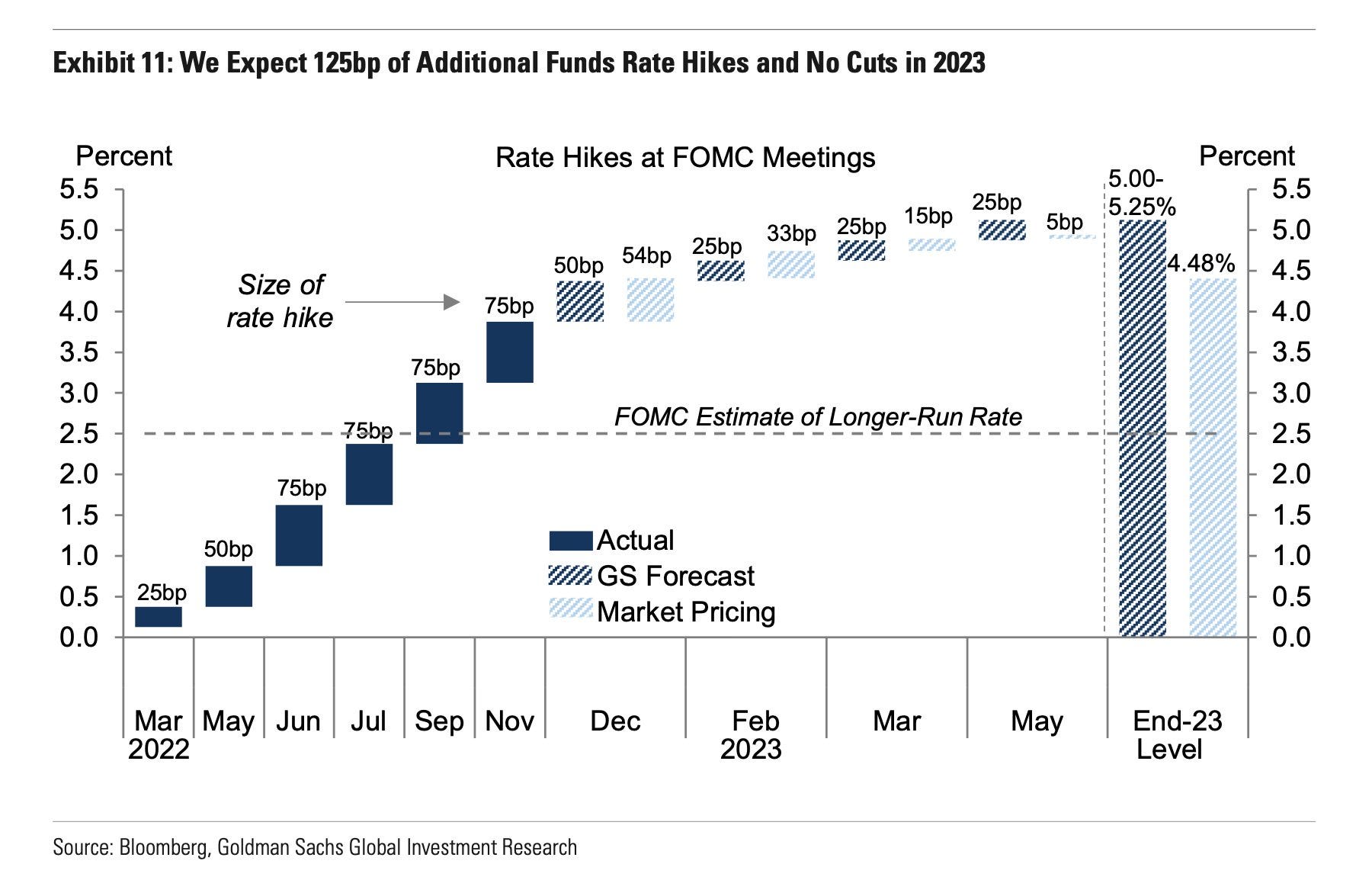

Goldman Sachs now expects an additional 125bp of Fed rate hikes (vs. 100bp prev.) with a downshift in the hiking pace to 50bp in December, and 3 smaller 25bp hikes in February, March, and now also May, with 5-5.25% peak funds rate.

World economy will be as weak next year as it was in 2009 after the financial crisis as the conflict in Ukraine risks becoming a “forever war,” the Institute of International Finance said. Global growth is expected to slow to 1.2% in 2023, economists including Robin Brooks and Jonathan Fortun wrote in a note Thursday. When adjusted for base effects, that’s as weak as it was in 2009. “The severity of the coming hit to global GDP depends principally on the trajectory of the war in Ukraine,” the analysts wrote. “Our base case is that fighting drags on into 2024, given that the conflict is ‘existential’ for Putin.”

JPMorgan sees US$ 1tr demand boost for global bonds in 2023. The key driver will be estimated reduction of US$ 1.6tr in global bond supply, outpacing an estimated deterioration of about US$ 700bn in demand, strategists led by Nikolaos Panigirtzoglou in London wrote in a research note Thursday. That decline in demand will be a major improvement from the US$ 5.9tr slide last year, they said. Bloomberg

BlackRock’s Bisat says now is time to buy Emerging Market Debt. The world’s biggest money manager is loading up on emerging-market debt again. BlackRock Inc.’s head of emerging-market debt Amer Bisat has dropped his 2022 defensive view on the asset class because he sees a peak in US interest-rate hikes nearing and thinks distress in some countries won’t trigger a systemic crisis. He favors bonds from the likes of Mexico, Indonesia and potentially Poland. “A window for bullishness has opened up,” said Bisat in an interview in London. “It is not the time to be extremely defensive any more and it is not too early to deploy capital.”

Morgan Stanley recommends to buy agency mortgages. Why? Three reasons:

Agency mortgages are trading near the widest valuations since GFC.

They have effectively no credit risk.

They are the most liquid fixed income spread assets.