A hawkish cut

The new dot plot and hawkish comment from Powell scared the markets

IN SHORT

Yesterday's FOMC in bullets:

Fed cuts rates by 25 bps for a total of 100 bps in 2024

Cleveland Fed President Beth Hammack dissented

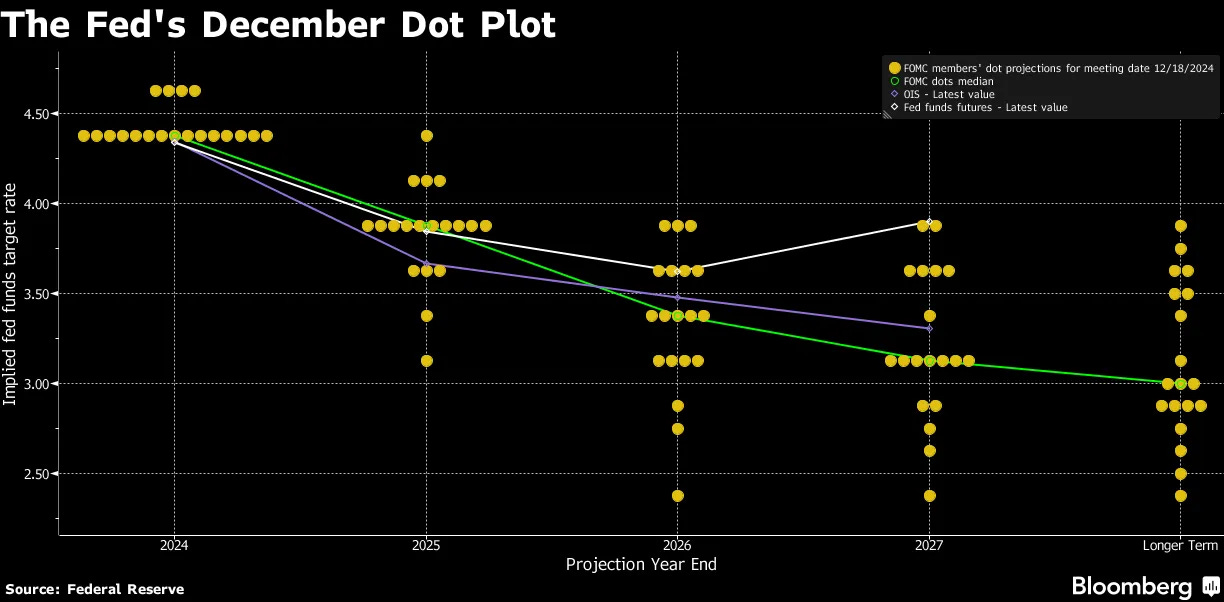

Fed median forecasts shows 2 cuts in 2025 for 50 bps (from 4 cuts)

Fed revises end of 2025 inflation projection from 2.1% up to 2.5%

Fed sees unemployment at 4.3% at end of 2025

One Fed official sees no rate cuts in 2025

Summary of Powell statements:

Inflation is "much closer" to 2% Fed target

Activity in the housing market has been weak

Wage growth in the United States has eased

Labour market is not a source of inflation pressures

Fed can be more cautious in reducing interest rates

Inflation expectations remains "well anchored"

Market Reaction:

STOCKS: Sold off across the board and SPX saw its worst "Fed day" since 2001, according to Bloomberg.

BONDS: Dived after Fed signals slower rate path ahead; US 10-year yield rose above 4.50%.

FX: DXY surged against major peers to a 108.27 high as the Fed delivered a hawkish cut - i.e. a 25bps cut as expected, but raising FFR projections above expectations, particularly in 2025.

COMMODITIES: Sold off post-settlement after the hawkish FOMC.

CRYPTO: Extended on recent losses with Bitcoin slipping under US$ 100k.

MARKET IMPLIED FED RATE CUT PRICING: January 2bps (prev. 4bps), March 12bps (prev. 17bps), May 15bps (prev. 23bps), December 2025 34bps (prev. 48bps); (prev. = pre-FOMC and incorporated for today's rate cut).

A new path

Fed cut rates by 25bps, as expected, to 4.25-4.5% in an 11-1 split, with Hammack voting to leave rates unchanged. The statement was little changed from the November meeting, but added in considering the "extent and timing" of additional rate adjustments (prev. In considering additional adjustments), the Fed will assess incoming data, evolving outlook and balance of risks.

Further hawkish skew came in the updated Summary of Economic Projections (SEPs) whereby the median dot plot for 2025 and 2026 FFR forecasts were lifted above expectations. Recapping, the median 2025 dot rose to 3.9% from 3.4% (exp. 3.6%), while the 2026 median rose to 3.4% (exp. 3.1%, prev. 2.9%). 2027 and longer run median dot plots rose to 3.1% (prev. 2.9%) and 3.0% (prev. 2.9%), as expected. As such, the 2025 median dot plot looks for just two cuts in 2025.

Core PCE inflation is now seen at 2.5% for 2025 (exp. 2.3%, prev. 2.2%) and 2.2% for 2026 (exp. 2.0%, prev. 2.0%). Forecasts for the unemployment rate were largely as expected, with all horizons, ex-longer run, seen at 4.3%, although 2027 was expected. In addition, and as was alluded to in the latest Minutes, the Fed lowered the repo rate by 30bps to 4.25% (lower end of FFR target, vs 5bps above lower end previously).

In Chair Powell's pre-prepared remarks he stated the Fed is squarely focused on two goals, and that the economy is strong, the labour market remains solid, and inflation is much closer to the 2% goal. Ahead of November PCE on Friday, Powell said total PCE probably rose 2.5% in the 12 months ending in November, while core PCE prices probably rose 2.8% in November. The Chair added that the policy stance is now significantly less restrictive, and going forward they can be more cautious, something which was indicated from the updated SEPs and statement tweak.

In the Q&A, the distinct hawkish remark came from the first question, which accentuated hawkish market moves, as Powell said that today's decision was a "closer call", but the "right call", suggesting there was a discussion surrounding holding rates at this meeting. Powell added risks are two-sided, and trying to steer between those two risks. Powell stated that "extent and timing language" shows Fed is at or near the point of slowing rate cuts, and the slower pace of cuts reflects expectation. Powell said that cuts they make in 2025 will be in response to data and as long as the labour market and economy are solid, they can be cautious as they consider further cuts. In addition, looking at US President-elect Trump's term, Powell said some people did take a very preliminary step and incorporated conditional effects of coming policies in their projections.

Finally, Powell said the central bank is not allowed to hold bitcoin and is "not looking for a law change" in the face of a promise made by President-elect Donald Trump to create a strategic bitcoin reserve. "We're not allowed to own bitcoin," Powell said. "The Federal Reserve Act says what we can own and we're not looking for a law change. That's the kind of thing for Congress to consider, but we are not looking for a law change at the Fed.”

MLIV: The worst Treasuries selloff since 2013 on a Fed day may prove short-lived. The 10-year yield will be 4.4% at the time of the central bank’s March gathering from about 4.51% now, according to the median in a MLIV pulse survey.

Volatility is back. The VIX spiked 74% higher yesterday, the 2nd biggest 1-day % increase in history. It soared for its largest gain since Volmageddon (February 5, 2018).

Investor positioning also played a significant role in amplifying the sell-off. Many participants, including both retail and professional investors, were heavily exposed through leveraged products such as futures and options. This exposure left markets vulnerable to sharp moves, especially as a result of technical factors like the imminent expiration of futures and options contracts. A striking example was Tesla’s 8.3% drop, exacerbated by market makers unwinding delta hedges during the sell-off.

Broader indices, including the S&P 500 and Russell 2000, experienced steep declines as high valuation levels combined with these structural pressures. This culminated in heightened volatility, as seen with the VIX spiking to its highest level since the summer, and significant losses across speculative and tech-heavy sectors.

Street comments

Goldman Sachs:

“Despite the hawkish message from the dots, we kept our more dovish baseline forecast of three more cuts in March, June, and September 2025 unchanged, though we added a bit more probability weight in our Fed scenario analysis to an outcome with a higher terminal rate. The gap between our forecast and market pricing is now a bit wider.”

“We acknowledge that the data—either worse employment news or better inflation news—will need to make the case for the next cut. We do not expect further labour market softening, though either further actual softening or a softer report or two driven largely by noise are certainly possible in the near term.

We do expect better inflation news by the March meeting, especially when looked at year-on-year to avoid being misled by residual seasonality distortions. In particular, we expect year-on-year core PCE inflation to fall from our 2.84% estimate for November to 2.56% in February.”

Moreover, Goldman Sachs think yesterday’s events provided both support for and risks to their relatively dovish forecast. They see support in their thesis as Powell reinforced confidence in inflation returning to target and noted labour market cooling, emphasizing that monetary policy remains restrictive. Plus, he dismissed inflationary pressures from the labour market and attributed recent inflation surprises to isolated factors. However, there are risks: there was unexpected hawkishness from some FOMC participants (with four dissenting on 2024 projections) and concerns about tariffs potentially complicating rate cuts. Powell acknowledged the need for caution amid policy uncertainty, suggesting a slower approach to avoid premature easing.

Morgan Stanley

Analysts now expect the Fed to deliver two 25 bps rate cuts in 2025 (prev forecast of three 25 bps cuts) following the December FOMC meeting. They still expect the Fed to cut rates at least thrice in 2026, but now see a higher terminal rate of 2.6%, compared to prior forecasts of 2.4%.

“The Fed's hawkish turn appeared to reflect the incorporation of potential changes to trade, immigration, and fiscal policy by some members that led to a firmer inflation path and, in turn, a firmer policy rate path”.

TD Securities:

"The Fed has sent a signal that they're not going to be quite as dovish as they've been in the past, that they are leaning towards fewer cuts next year, and I think that's a signal for markets to continue to price in even fewer than two and possibly move in the direction of none if the data comes in strong enough. The Fed is not willing to keep cutting if they don't see inflation coming down enough, and their summary of economic projections suggested that they still expect inflation at two and a half percent on core PCE by the end of next year. The takeaway here is somewhat higher for longer rates, and you do see risky assets not loving this particular backdrop... Rates are moving higher but the saving grace for rates is that they've already been selling off for the last week or so, already expecting a relatively hawkish Fed, and it sounds like the Fed really delivered on the hawkishness."

Barclays

“We retain our baseline projection that the FOMC will cut rates only twice, by 25bp, next year, in March and June, with core PCE inflation rising again in H2 25 amid increased import tariffs and tighter immigration restrictions. We then expect the FOMC to resume its rate-cutting campaign around mid-2026, with two 25bp cuts that year, bringing the target range to a modestly restrictive 3.25-3.50%. The median dots for 2025 and 2026 now align with our call.”

Ned Davies’ Joseph Kalish:

“Although Powell indicated the Fed would proceed cautiously as it approaches neutral two additional rate cuts in 2025 seem easy to do. Whether they do more will depend on policy actions and the economic data. As for when they might pause, January seems likely. Our baseline is for three cuts in 2025 on a quarterly cadence on slightly weaker labour markets. There would be a reasonable case for another cut in January should the December employment report prove to be weaker than expected”.

Yardeni:

“Today's panic selling was triggered by the Fed's hawkish rate cut and indications that there might be only two rate cuts next year, not four because inflation is turning out to be hotter and the economy is proving to be more resilient than the FOMC expected. That's been our forecast since August.

We think that the stock market might remain sloppy through January. Some investors might be planning to take their substantial profits early next year rather than now to defer capital gains taxes. There could be a longshoreman's strike in mid-January because they oppose automation at the ports. Trump publicly declared that he agrees with the dockworkers. Furthermore, on day one of Trump 2.0, a blizzard of executive orders will likely include a bunch imposing tariffs and authorizing deportation of illegal migrants.

We can't rule out a 10% stock market correction, but we would view that as a buying opportunity rather than as a reason to panic out of the market since we don't expect a recession or a bear market. We are still targeting 7000 on the S&P 500 by the end of next year.”

CreditSights:

“We remain comfortable with our call for the policy rate to finish 2025 at 4.25-4.50% and now think the more likely path is that the Fed remains on hold for an extended time after today's cut (rather than cutting in Q1 and later reversing course). The path of inflation appears to be sticky for at least the next couple of core PCE deflator prints, and the Fed has clearly raised the bar for future policy adjustments. The 10y Treasury yield is up nearly 10bp from just before the 2pm release and the 2y yield is up just a touch more than that. The S&P 500 is also selling off, and we think we could see spreads widen a bit over the next couple days. With monetary policy potentially shifting from a tailwind to headwind for fixed income markets, we are comfortable with our Underweight recommendation for both IG and HY corporates in anticipation of spread widening as focus shifts to fundamentals, and the technical tailwind from cash coming off the sidelines may fade as economic expectations shift and the policy rate remains higher for longer.”

Datatrek:

“Chair Powell’s press conference was bookended by his observations that today’s rate cut was a “closer call” than previous decisions and that he could not rule out a rate hike in 2025. The rest of his commentary filled in the gaps between those two statements. Inflation is proving stubborn. Labour markets remain in decent shape. The effect of tariffs and tax cuts are unknowable. The US economy is in good shape despite still-high policy rates. In short, the Fed can afford to wait and rule nothing in or out. We think that’s fine and remain bullish.”