Investor positioning remained very cautious in November, according to the Bofa global fund manager survey, which took place before the latest US inflation data. Cash was the most popular asset class, with net 51% of investors saying they are overweight.

Why do we see such levels in cash? Are investors afraid of the market or they are preparing big investments? It seems that analysts cannot agree on the future scenario.

Almost a third of Stoxx 600 members are trading at overbought levels, the highest proportion in five years. The breadth of stocks whose relative strength index exceeds 70, which is greater than during the recovery rally of 2019.

TS Lombard's Blitz with a "gentle reminder"

"...in the wake of the economy’s deceleration from 6% growth last year, inflation will continue to decelerate in fits and starts (look for some upside acceleration in the Nov data), but a return to 2% is not in the cards. There is no impending recession evident in the data, the economy remains well above potential, and against all this, the real funds rate is still too low. I expect a 75bps increase at the December meeting, and a 50bps hike in February. At some point spending sags, unemployment rises, and hikes turn to cuts. The time is nearing – but not if the FOMC slows in Dec and allows financial”.

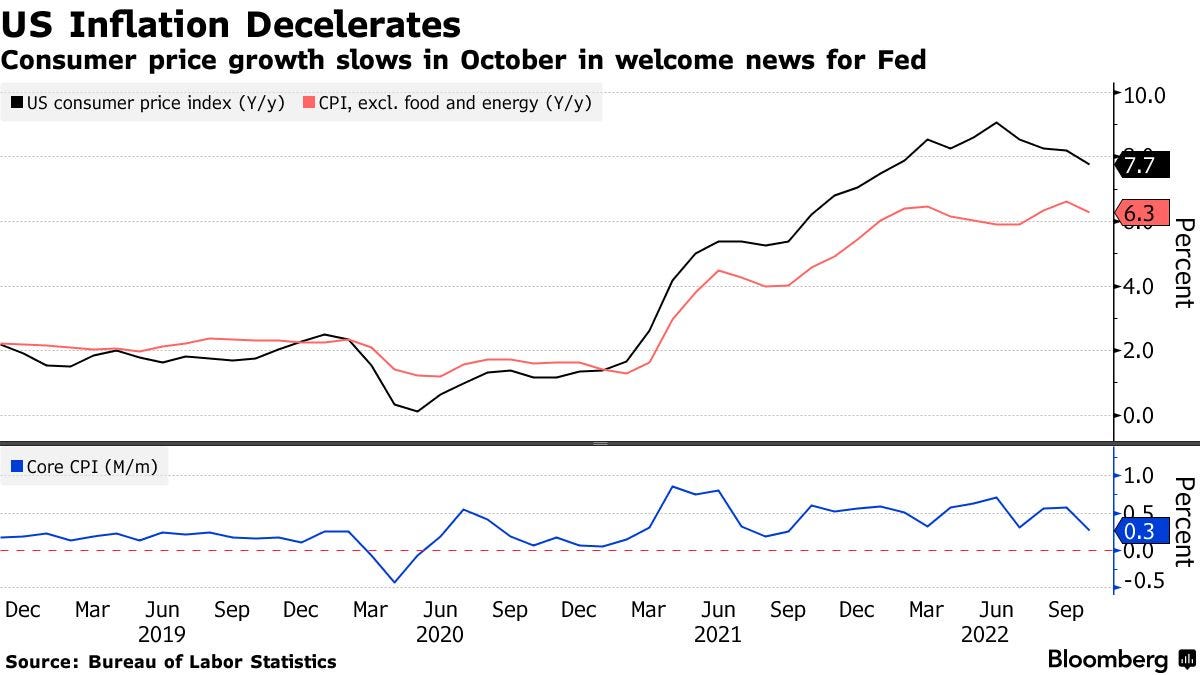

Blackrock: Goods inflation is easing as it needed to, but the labour constraints driving wage growth and core inflation persist. So the Fed is still on a path to create a recession via policy overtightening. Stocks aren’t pricing that in, so they stay underweight.

JPMorgan’s Kolanovic trims Bullish Stocks Call on Recession Risk. Marko Kolanovic took another step in backing off the bullish stocks call that he had maintained throughout much of the market’s rout this year. Kolanovic, co-head of global research at JPMorgan Chase & Co. and the most vocal bull on Wall Street, said in a report that he was reducing his overweight equities position because recession risks remain high.

Goldman Sachs explains why US will “narrowly” avoid a recession. Specifically, the firm is calling for a 35% probability that the US economy pushes into recession, compared with The Wall Street Journal October Forecaster Survey's consensus median forecast of 65%, Goldman Sachs Chief Economist Jan Hatzius wrote in a note to clients Wednesday.

GS expects the Euro area recession to be shallower.

"We now expect the Euro area recession to be shallower. First, the incoming data have remained more resilient than expected. Real GDP in Q3 surprised to the upside and the hard data coming into Q4 (September industrial production and retail sales) showed continued growth. Second, the rebalancing of the gas market—with a build-up of significant gas storage and sharp declines in gas prices—has reduced the risk of energy rationing this winter. Third, governments have provided significant fiscal support to cushion the growth hit”.

On Fed:

"We are adding another 25bp rate hike to our forecast... We continue to expect a 50bp hike in December and 25bp hikes in February and March, and we have now added a 25bp hike in May. This raises our forecast of the peak fed funds rate to 5-5.25%”

Morgan Stanley’s Mike Wilson drops his 2023 outlook: 3900 base case year-end.

“A Volatile Path to 3900… After what's left of this current tactical rally, we see the S&P 500 discounting the '23 earnings risk sometime in Q123 via a ~3,000-3,300 price trough”.

Head of the WTO says risks to the 2023 global trade forecast are to the downside due to the uncertainties surrounding the Ukraine crisis, rising food and energy costs and inflation. There is a real risk of recession in some major economies, with significant consequences for emerging and poor economies.

Investment giants with US$ 2.3tr bet on more market turmoil (Bloomberg)

Tumbling global stock and bond prices this year, together with pain in private equity amid deteriorating deal volume left investors around the world casting their nets far and wide for opportunities.

GIC Pte. (estimate US$ 690bn)

For Singaporean sovereign wealth fund GIC Pte., preparation means having cash at the ready, a willingness to spend it and an ability to buy low-cost assets as other investors sell out. Chief Investment Officer Jeffrey Jaensubhakij has made investments that offer protection from inflation and says that price pressures will continue to rise amid tight labor markets and an underinvestment in commodities.

“It’s been important for us to try to move assets from the asset classes like bonds and equities into things like real estate and inflation where the ability to either be CPI-linked or the ability with high demand to raise rents over time allows us some protection against inflation”.

GIC Chief Executive Officer Lim Chow Kiat said buying secondary private equity funds during the pandemic proved lucrative and has whetted the firm’s appetite to do more of this type of deal.

Fidelity International US$ 613.3bn

Anne Richards, chief executive officer of Fidelity International, said that Asia including China could rebound in sentiment faster than other parts of the world.

“There’s a lot of optimism of where China is in its interest rate policy cycle, and the benefits that will bring for the region as well as the kind of gradual opening up”.

AustralianSuper A$ 272bn (US$ 184bn)

AustralianSuper Pty Ltd. Chief Investment Officer Mark Delaney is taking a cautious approach. His pension firm, the largest in Australia, began turning defensive late last year, reducing its exposure to listed equities and credit.

“We have built up our positions in cash and more recently fixed interest, things that we think could benefit from a downturn”.

Ontario Teachers Pension Plan C$ 242.5bn (US$ 183bn)

Chief Executive Officer Jo Taylor is looking to mining assets, with rare earth minerals and metals a key target.

“Rare metals. Because they are just that -- they are scarce and there aren’t that many that aren’t Chinese owned. You can have the commodity rather than some sort of traded index, it’s not a big market”.

That means targeting copper producers in Canada and Chile, lithium from Latin America and finding sources of cobalt.

Partners Group US$ 131bn

Partners Group Holding AG Chairman Steffen Meister thinks it is a good time to strike deals for firms that anticipated the turmoil. Partners Group has pushed out refinancing until 2025 and hedged much of their rates exposure. The fallout from the UK’s recent volatility in the pound and gilts would help boost other opportunities.

Longer term thematics such as aging populations are also a good sources of deals, Meister added. This could mean housing or residential apartments built for rent with affordability and inclusion becoming a major topic. Other investment ideas include logistics, cold storage and pharmaceutical storage.

Temasek Holdings S$ 403bn (US$ 295bn)

Temasek International’s Chief Investment Officer Rohit Sipahimalani cited investment themes such as sustainable living, growing consumption, longer lifespans and healthcare. But now, Temasek is slowing the pace of investments.

“We’re cautious because we don’t think valuations fully reflect the downside we expect over the next 12 months. The reason we’ve slowed down is because of the valuation environment. There’ll be better opportunities down the line”.

China Asset Management ¥ 1.79tr (US$ 253bn)

Despite steep declines this year, China’s A-share stock market remains a better option than US, European or Hong Kong equity markets, according to Richard Pan, Chief Investment Officer of global capital investment at Beijing-based China Asset Management.

“China is a rare place where the government is still in a loosening cycle, providing ample liquidity. The yuan has also remained stable against a basket of currencies despite depreciation against the strengthening dollar”.

China Asset Management sees opportunities in both new energy and fossil fuels due to the huge demand in the coming decade, and likes healthcare and medical equipment stocks.

On USD

Goldman Sachs expects the recent Dollar weakness to reverse.

"Outside of the US, recent news has also been negative for the Dollar: surprisingly resilient hard data in the Euro area have pushed back severe recession fears, and incremental signals toward relaxing Covid restrictions in China have also supported risk sentiment. However, we also think these developments are insufficient to change the fundamental picture in the near term. The Euro area outlook remains troubling, although those risks could be somewhat backloaded, and still there is an element that more robust global activity could become self-defeating for Europe in a world where energy supply is still constrained. While recent data in the US and abroad have altered some of the tail risks, we still think the baseline outlook is likely to feature relatively resilient US activity, and a longer Fed hiking cycle, with few high-quality alternatives among the majors. We expect the recent Dollar weakness to reverse but it is likely to be a slower, choppier process as positioning adjusts to lower tail risks".

Deutsche Bank’s George Saravelos on Dollar:

“The dollar on Friday experienced its largest two day drop since 2008. Is the move justified? Yes. Would we fade it? No. The peak in the dollar is behind us.”

Technicals are telling an interesting story

Stocks have come roaring back since that cooler-than-expected CPI report on the 10th of November but the equity market has stopped this week as it approaches Friday's monthly options expiration date, pinning the SPX around 4,000 level.

That's likely to change when the option market resets: volatility should come back next week as the S&P 500 releases from the November options expiration date, as open interest levels drop and reset, allowing the market to move more freely.

Currently, the S&P 500 has been stuck around 4,000 because that's the level with the greatest concentration of options gamma that is “sticky” because of the high delta. At these levels volatility is low, which is why the index has been unable to rise further this week.