Are we at the top?

Market reached ATH. Will it go down from now on?

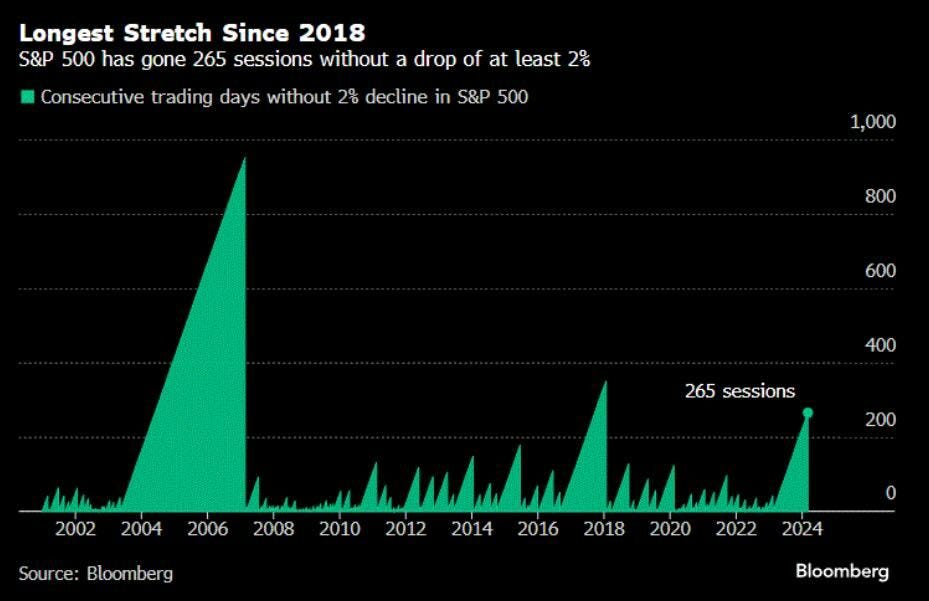

S&P 500 has now gone 265 sessions without a drop of at least 2%. The longest streak since 2018.

And 82% of S&P 500 stocks are now trading above their 150 Day moving average, the highest level since July 2021.

But why market keeps going up?

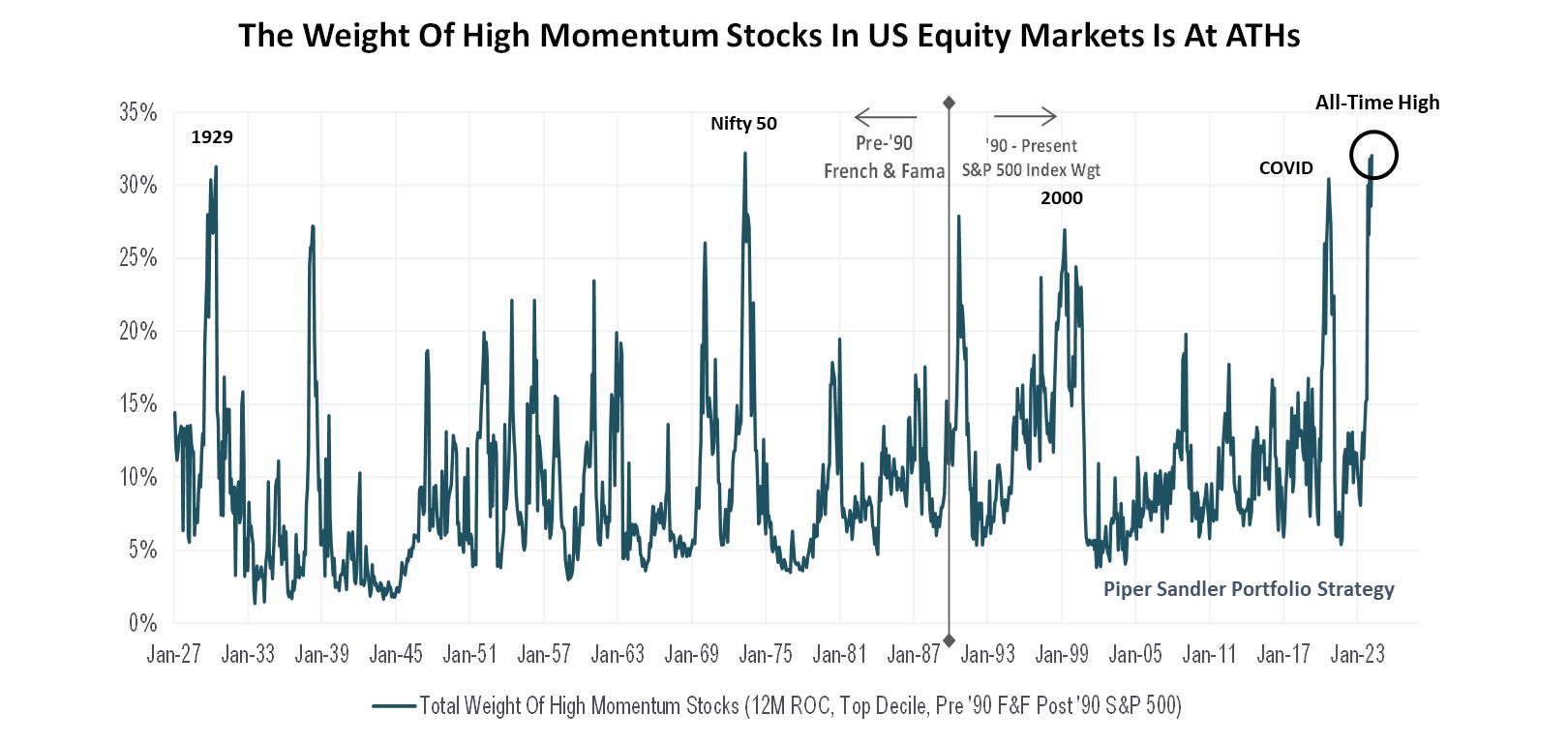

Is the S&P 500 more momentum-driven than ever? The weight of high-momentum stocks in U.S. markets has never been this high over the past 100 years.

JPMorgan on equity momentum. Momentum crowding flashing RED at 99.8%ile – fastest increase ever. Last seen at the peak of 2000 Tech Bubble. Equity investor positioning near prior highs. Momentum often becomes crowded – leading to inevitable momentum crash.

Some analysts think that the trend could change soon

JPMorgan Chase strategist Marko Kolanovic has issued a cautionary note regarding the recent surge in momentum stocks, often referred to as the “Magnificent Seven.” Historical patterns indicate that such surges are typically succeeded by corrections. Investors should remain vigilant and consider these insights when navigating the market.

“Momentum is a dynamic stock factor that changes its exposure depending on macroeconomic and fundamental conditions. As such, it often becomes crowded, followed by an inevitable and often sharp correction (i.e. momentum crash)”.

Three such episodes have happened since the global financial crisis in 2008. The year-to-date performance of the top five stocks has pushed market concentration to “even more extreme levels,” widening the spread between largest 10 and the next 40 stocks. Higher for longer interest rates and the “halo effect” of artificial intelligence stocks are the reason for crowding into megacaps, while most US and global companies struggle to grow earnings and preserve margins, Kolanovic said.

“Given this relationship coupled with very bullish investor sentiment and positioning, we caution investors that this relationship is likely to work in reverse when the AI euphoria peaks”.

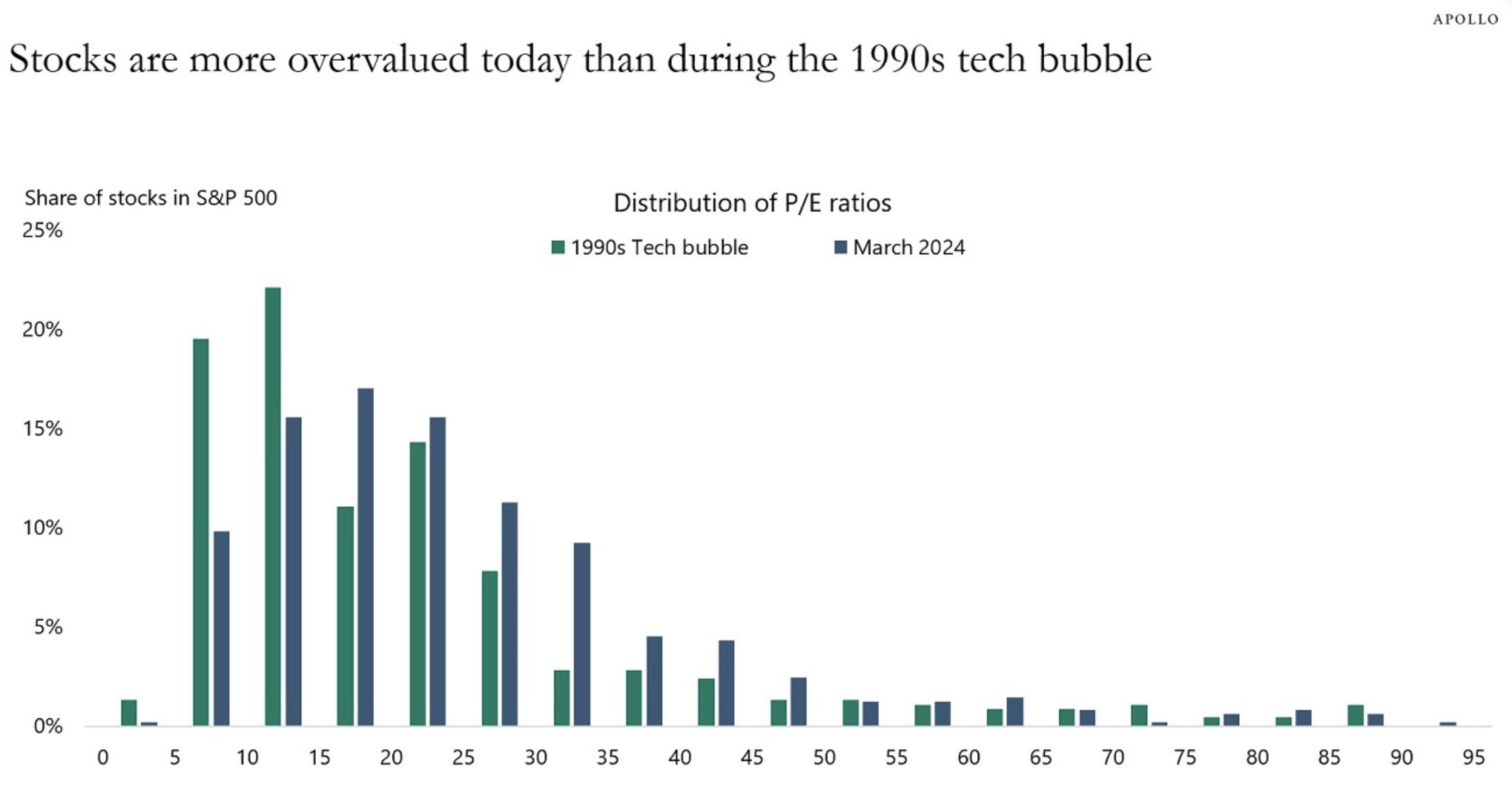

Apollo says stocks are more overvalued today than during the 1990s tech bubble. Apollo just doubled down on their view that we are in a bigger bubble than the 2000 Dot-com bubble. 3 weeks ago, they said the current bubble is "bigger than the 1990s tech bubble." They note that the Forward P/E ratio for the top 10 tech stocks right now is ~40x. Compared to 2000, at the peak of the Dot-com bubble, the Forward P/E on the top 10 tech stocks was ~26x. Now, Apollo says that ~30% of stocks have a P/E ratio of 30x or more. Overall, Apollo says that P/E ratios now are much higher than they were in 2000.

BMO’s Brian Belski, who correctly predicted the advance in US equities last year, now says it’ll be challenging for the S&P 500 to close 2024 much higher than current levels. Belski predicts volatile price action in remainder of year, with investors placing too much emphasis on timing and magnitude of Federal Reserve interest-rate cuts.

“We do not view the current pace of US stock market gains as sustainable over the coming months. […] Therefore, we believe it will be difficult for US stocks to finish the year at significantly higher than current levels”.

Strategist emphasizes he does not suggest avoiding US stock exposure — instead, the environment is good for stock picking. Growth-at-a-reasonable-price is a “worthwhile fundamental stock picking strategy,” he says, while a significant number of factors are appealing from a quantitative perspective.

Even Morgan Stanley’s Mike Wilson won’t budge, arguing he sees no justification to upgrade his outlook given an absence of broad earnings growth. The strategist stuck to his year-end S&P 500 Index forecast of 4,500 in an interview on Tuesday with Bloomberg Surveillance Radio, even as a growing list of peers at firms including Bank of America, Goldman Sachs Group, and UBS have raised projections for the benchmark.

Wilson’s call is roughly 12% below the S&P 500’s closing level Monday of around 5,118, and 8% short of the average year-end call of Wall Street strategists tracked by Bloomberg, of 4,915. Among the big banks, only JPMorgan has a lower 2024 forecast than Wilson’s.

“A lot of folks have raised their price targets because of higher multiples; we’re not willing to do that”.

His scepticism comes in the face of a sharp rally in US stocks since October. The S&P 500 gained in 16 of the past 19 weeks amid enthusiasm around corporate earnings, artificial intelligence and economic strength. The index resumed its climb Tuesday after declining the past two sessions. The day’s advance followed a hotter-than-forecast inflation reading that left intact expectations for at least three Federal Reserve interest-rate cuts by year-end.

Wilson’s more optimistic counterparts at rival banks have pointed to strength from US firms and the economy in the face of tighter monetary policy. But he said Tuesday that broader earnings growth is still missing. Earnings for the S&P 500 grew 7.4% in the fourth quarter from the same time a year ago. Excluding the Magnificent Seven group of technology giants, profits in the index posted a 1.7% contraction, data compiled by Bloomberg Intelligence show. Wilson also added that “the risk of a hard landing has still not been exterminated.”

In Wilson’s view, speculative activity across the market has picked up in a “meaningful way.” He pointing to the rising popularity of zero-day options trading and use of leverage, noting that exuberance is high.

“Now, it doesn’t have to end in tears. Leverage isn’t always bad. We have a situation where people are reaching for risk because there is FOMO”.

Thank you for a brilliant read!