Extreme pessimism built the case for a short term rebound

A relief rebound is needed

Let’s recap few interesting views about equity market valuations and the extreme investor pessimism reached this week.

We believe the current market level offers the case for a short term rebound, before eventually see a new down-leg at end of October-November.

Retail investors are quitting. This has been the first week of the year in which retail investors are heavily selling, for about US$ 4bn.

Investors seeking refuge in options, spending more than US$ 18bn in puts (biggest size since 2020 sell off), paying a high premium to cover themselves from even bigger losses. At the same time, Goldman Sachs highlighted that selling upside Calls to buy downside Puts has not been this cheap since 2008. Matt Fleury writes: “To buy an SPX 3mo 90% put, you can sell an SPX 3mo ~108% call for even money". The crowd is short via 1 delta products.

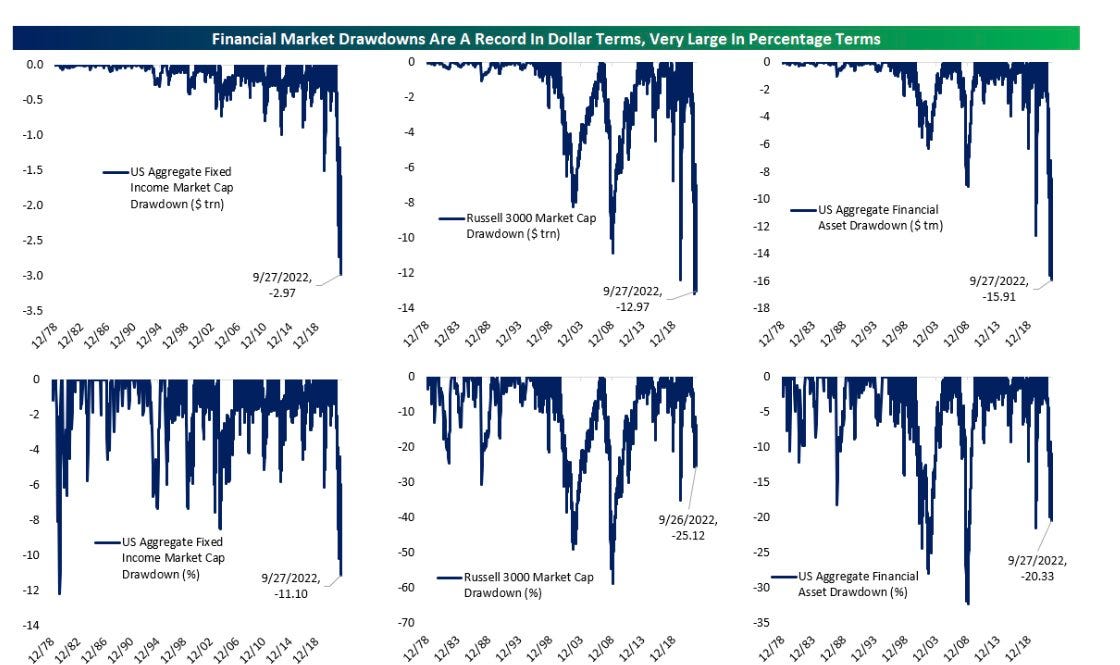

Bespoke talks about “a staggering sum”. From the peak, US$ 16 trillions in lost market cap for equities and high-grade bonds — “larger than the COVID shock, the Global Financial Crisis, or the aftermath of the Tech Bubble”. Gavekal Research, Macrobond

And if we look at the US Aggregate Financial asset draw-down is even worse. This year's downturn has wiped away US$ 57.8 trillions in wealth.

Not surprising that the S&P 500 is on the verge of having its longest quarterly losing streak since 2008-09. When combined with heavy put volume and VIX > 30, it's not a super encouraging picture. Good news is that over the last 20 years, on average, the SPX has gained 4.1% in the Q4.

AAII Sentiment, Bulls & Bears: Last week it was "bears above 60% for only the 5th time ever!" This week it's "bears above 60% in back-to-back weeks for the first time IN HISTORY!" Wouldn't make too much of either as long as sentiment is not reflected in positioning.

Now the good news

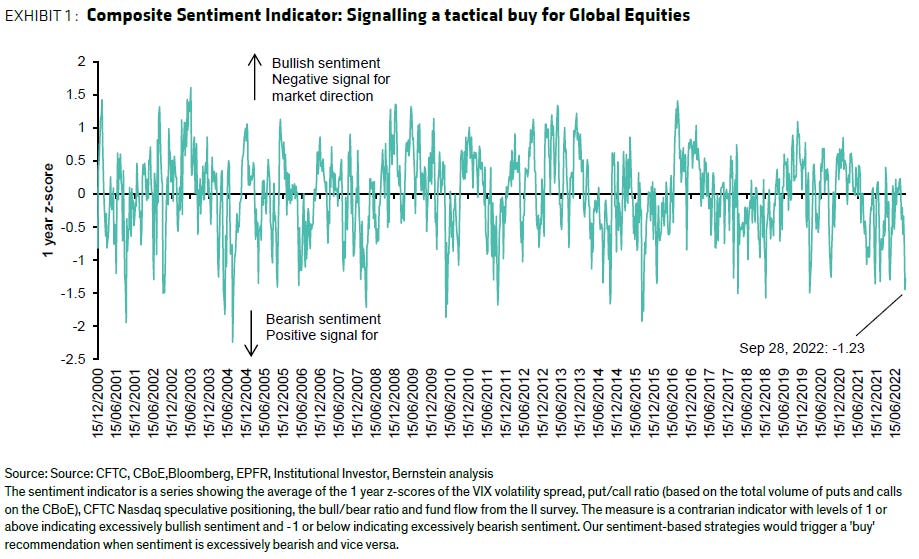

Sanford Bernstein Research strategy team suggests extreme negative sentiment could provide a short term tactical trading opportunity:

"Our Composite Sentiment Indicator (CSI) has just triggered a buy signal. Over the past 22 years buy signals have been followed by positive 4 week forward global equity market returns over 70% of the time. We consider this signal as a potential short term tactical buying opportunity but remain cautious on equities over a medium term horizon".

Since the year 2000, the indicator's buy signals have preceded positive returns over the next 4 weeks > 70% of the time.

And valuations? Are they cheap enough?

For sure they reached an interesting level. It is worth to take a look.

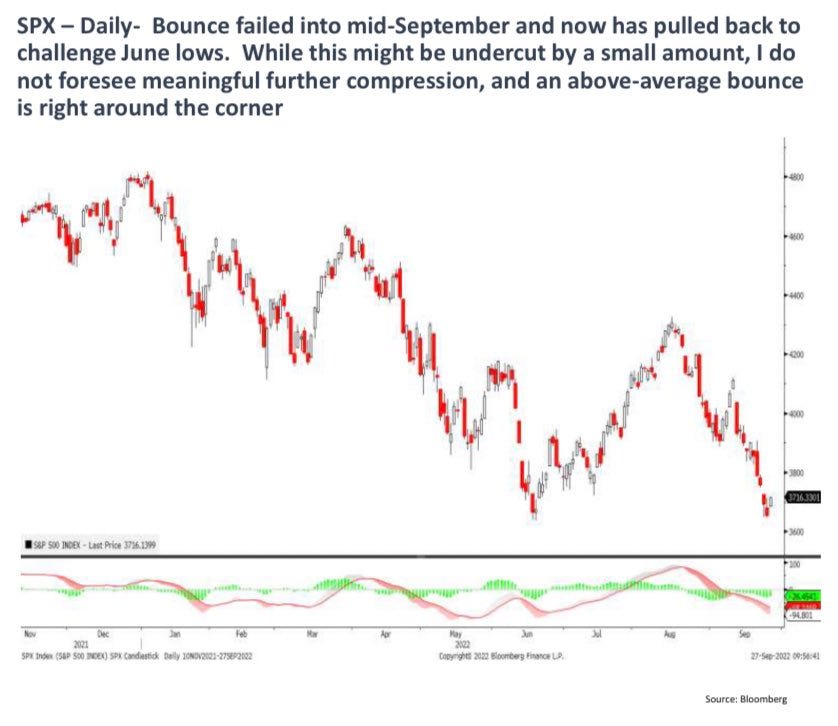

“Stock indices are likely to bottom out in October, initially during the first week potentially. Rallies might encounter some resistance into Earnings, but any late month selloff is buyable for a push up into December of this year”.

Longview Economics equity valuation perspective: the current playbook of how the PE ratios are evolving looks similar to that of in the late 1990s to early 2000s. While 'Mega Caps' valuations have started to normalise, they remain extremely overvalued relative to the S&P500 index.

What about Emerging Market equities? They are cheap! But remember… cheap can get even cheaper.

China shares plunge to lowest valuation on record in Hong Kong. As September draws to an end, the Hang Seng China Enterprises Index has lost more than 14% to rank as the worst performer among major equity benchmarks globally this month. Hovering around the lowest since the global financial crisis, it is now trading at 0.6 times book value, the cheapest ever. Bloomberg article

Emerging Market Equities (in USD terms) are down a whopping 40% from their peak. Most of the time, this would accompany a global recession. With China no longer the world's growth engine, this time is no different. True Insights

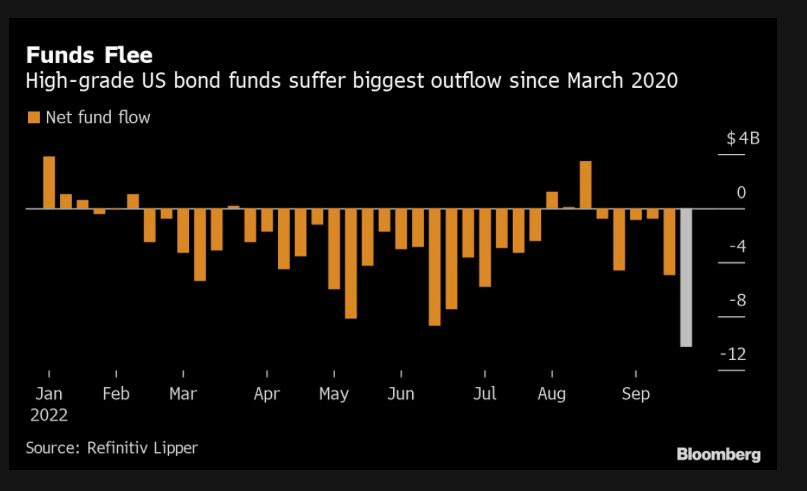

US Investment Grade bond funds suffered their third-largest cash exit on record, with investors yanking US$ 10.3bn out of the funds in the week ended Sept. 28. It marks the sixth straight week of withdrawals. We have already said many times here, that the higher rated bonds are starting to look attractive; in particular the short term maturities (up to 3-4 years). More will follow on this topic.

Conclusion

While we cannot still call for an outright strong bull case, we believe the market is (technically speaking) in the need of a relief rebound. This could last between 2-3 weeks.

As stated above rallies might encounter some resistance into US earnings. They could prove more brutal than market expectations: i.e. yesterday Nike stock drop is a good example.

Overall we maintain a negative view on risk assets. But relief rallies will be strong and can be used opportunistically to create pure alpha.