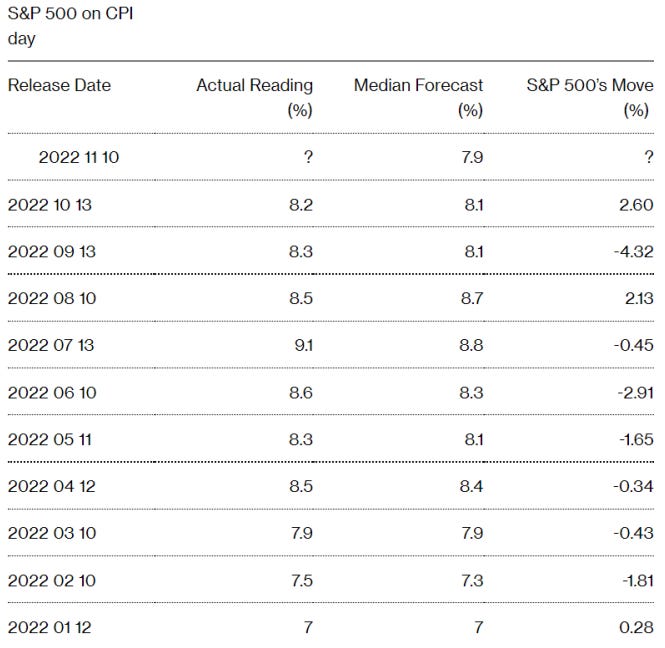

CPI day - the possible market outcomes

The inflation index will be the main market driver for this month

At 14:30 CET, USA CPI will be released. Forecast is at 8% while for core CPI 6.5%: both are seen reducing than the previous.

The result will give an important insight on the Fed future moves and SPX will react.

Yesterday, the market saw a massive risk-off, with all the S&P 500 sectors in red:

This is due to nervousness about the incoming CPI data and the crypto havoc caused by FTX.

JP Morgan outlines the scenarios for markets’ reaction to CPI

Today's CPI report will make or break bear market rally #7 and for a Fed pivot. Regardless of today's data, we believe we are a long way from a market, housing and earnings bottom.

If inflation comes in hotter than expected, Fed panic will worsen. In the Fed's statement last week, we learned that their biggest fear is not raising rates enough. A high CPI reading would be hard to digest.

Even if CPI print comes in lower than expected, any relief rally unlikely to last. Forward looking economic indicators suggest too much damage has already been done, future earnings about to take a big hit. The pace of earnings downgrades has accelerated in the US, especially compared to Europe, as a Citigroup Inc. gauge of US earnings changes has had 23 consecutive negative prints, the longest losing streak since early 2020 – Bloomberg

CPI SCENARIO ANALYSIS

This week's CPI will be the most important factor to shape the expectations for December FOMC. Currently, the OIS market has fully priced in a 50bp hike and sees 45% chance of a 75bp hike in December. Mike Feroli's CPI estimates for Headline YoY is 7.9% and for Core YoY is 6.4%.

5% Prints 8.4% or higher: this would be a move back to July levels of inflation, which we may see on a MoM basis but think Equity investors care most about the Headline YoY level. This would represent the largest differential between actual and estimated in this cycle. SPX down 4.5% - 6%.

30% Prints 8.1% - 8.3%: there have been 4x misses of 20bps or more and the SPX fell 1.6%, 2.9%, 40bps, and 4.3% which is a down 2.3% average. The 40bps outlier came when the SPX was —3820 the day before the print. In the other 3 cases, the SPX was between 3930 and 4000. SPX down 2% - 3%.

40% Prints 7.9% - 8.0%: I think bonds, and thus stocks, take this as a small positive since it meets expectations and does not reprice yields higher. Given that we are at the bottom of our Cash Trading team's range (3700 — 3900), we may see some covering leading to an uptick in stocks. SPX higher 1% — 1.5%.

20% Prints 7.7% - 7.9%: this could be similar to the August 10 print which had a dovish beat by 20bps and triggered a 2.1% rally in SPX, 2.8% in N DX, and 2.9% in RTY. Cyclicals, Value Shorts, Momentum Shorts, and ARKK the best performers that day. Given the increased bearishness, the magnitude of move could be larger. SPX higher 2.5% - 3.5%

5% Prints 7.6% or below: seeing a stepdown in inflation of this magnitude likely pulls the 10Y yield below 4% (currently 4.158%) and triggers a sharp rally in stocks. This may also reset the yield curve lower with terminal rate expectations falling under 5%. SPX higher 5% - 6%.

Potential S&P 500 SPX reactions based on CPI reading

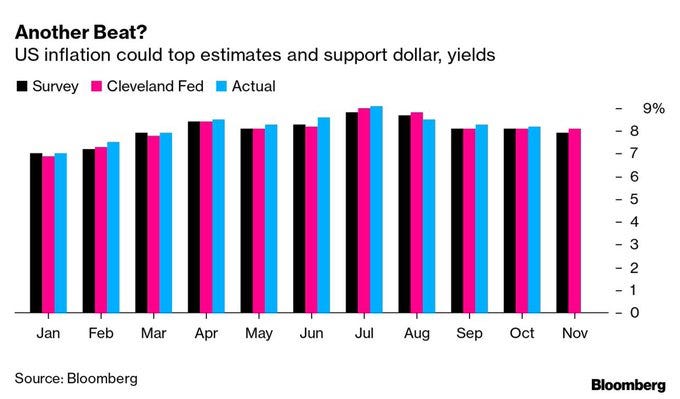

Other forecasts:

Bloomberg survey shows 7.9% expected

Cleveland Fed forecast is 8.1%

Previous month’s CPI was 8.2% (Sept)