Credit Suisse crisis sparkles panic

The Swiss central banks intervention calm markets after the bank collapse

Being headquartered in Switzerland, we couldn’t avoid to put it down few thoughts on the topic. In the past few days the desk has been busy trading and advising its clients on Credit Suisse. We had have selling volumes yesterday and later in the day accounts started to buy both CS Senior and Subordinated bonds. After a gap up at the opening, the interest today is more two-way.

Markets yesterday panicked. Credit Suisse seemed to be on the verge of a crisis, but SNB intervened. This is not the first time we see CS 0.00%↑ in the centre of the storm:

2009: Fined US$ 536m for failing to comply with US laws, including Iran sanctions violations, regarding payments processed for persons from countries subject to US economic sanctions.

2014: Pleaded guilty to criminal charges that it helped Americans evade taxes, becoming the first bank in more than a decade to admit to a crime in the US: fine of US$ 2.5bn.

2021: Risk management failure caused US$ 5.5bn loss on investment fund Archegos after its downfall. And in addition winded down US$ 10bn of supply-chain finance funds linked to troubled financier Lex Greensill.

2022: Admitted to have defrauded US and international investors in the financing of an US$ 850m loan for a tuna fishing project in Mozambique, paying US$ 495m fine.

2023: during the last week…

Postponed the publication of its annual report following a last-minute call from the US SEC. The SEC raised questions regarding the group's earlier financial statements. The SEC wanted to enquire into a "technical assessment of previously disclosed revisions to the consolidated cash flow statements in the years ended December 31, 2020, and 2019, as well as related controls".

The bank found “material weaknesses” in its reporting procedures for the financial years 2022 and 2021 and said it is adopting a new plan to fix them, following a fresh review of its financial statements prompted by concerns raised by US regulators.

Saudi National Bank said it would not buy more shares in the Swiss bank on regulatory grounds.

US Treasury and ECB announce they are monitoring CS situation.

Finally, Credit Suisse gets help from the Swiss National Bank. The SNB said it would provide a liquidity backstop to Credit Suisse after the lender’s shares fell by as much as 30% and sparked a broader sell-off in European and US bank stocks. In a joint statement with financial regulator Finma on Wednesday evening, the SNB said there were “no indications of a direct risk of contagion for Swiss institutions due to the current turmoil in the US banking market”. Separately, the bank announced cash tender offer in relation to 10 US dollar denominated senior debt securities for an aggregate consideration of up to US$ 2.5bn and cash tender offer in relation to 4 Euro denominated senior debt securities for an aggregate consideration of up to € 500m.

The bank’s equity is down more than 80% in last years and its market cap is now down to CHF 7.5bn. The bank’s equity is trading at record lows and at P/B of just 0.2 times reflecting deep skepticism about its turnaround prospects and lack of any sustainable earnings visibility over the next 2 years.

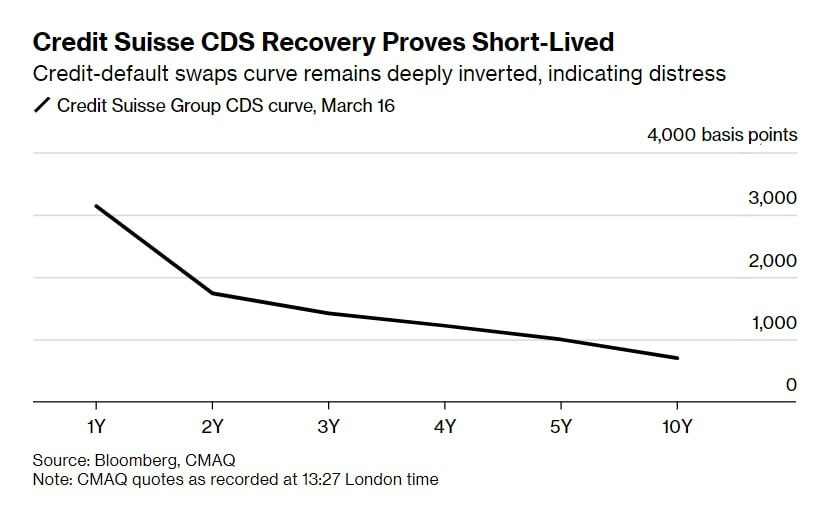

Yesterday, CS Credit Default Swap spread spiked above 2008 levels and pricing in a probability of default of >50%.

The CS headlines drove a dramatic sell-off in markets, especially European. The iTraxx Main widened by the largest day change since 2020. Spiking CDS, used as the credit market’s barometer of risk in the financial sector, shows investor concern.

Credit analysis and views on the market

CS outstanding Senior bonds are issued at Opco and Holdco level, whilst almost all its AT1s are at Holdco level. CS has a huge number of outstanding senior bonds issued across various currencies.

In terms of ratings, CS Holdco Senior bonds are rated Baa2 (neg)/ BBB- (stable). CS Opco Bonds are rated A3 (neg)/ A- (stable) and BBB+ (neg). Credit Suisse Group AG is the Holdco issuer whilst Credit Suisse AG London/NY branch is the Opco issuer.

The banks has still a decent capital situation with CET1 ratio at 14.1%, Tier 1 leverage ratio at 7.7%. While the Liquidity Coverage Ratio has now probably reached 150%.

The high trigger AT1s get written down if CET1 reaches 7% or lower and the low trigger AT1s get written down if CET1 reaches 5% or lower. Senior will be impaired or bailed in if the bank suffers a CET1 drop of more than 910 bps or almost CHF 25bn of unexpected losses.

The bank does not seem to have a liquidity, asset quality or a material capital issues (CHF 15bn of subordinated AT1 outstanding), but it’s paying the years of underperformance, deposit outflows and failed restructurings. CS has an earnings issue and lack of a clear strategy in its investment banking franchise, plus a high cost base, large restructuring charges and ongoing reputational and legal costs. The core issue for the bank is to restore profitability in its investment bank whilst retaining its clients/flows in wealth management/private banking.

A takeover could solve troubles, according to analysts at JPMorgan. Analysts led by Kian Abouhossein laid out three scenarios for Credit Suisse’s future, with the most probable being an acquisition by UBS Group AG. Credit Suisse’s capital position isn’t an issue, but the “situation is about ongoing market confidence issues with its investment banking strategy and ongoing franchise erosion,” Abouhossein wrote in a note. “Status quo is no longer an option.”

Reputation has been badly hit and is subject to constant negative headlines and mismanagement. This has led to loss of confidence amongst investors and market participants leading to a material re-pricing of its debt issues and this impacts earnings.

JPMorgan’s scenarios:

A takeover, likely by UBS. Given the market concentration between the pair, a takeover would possibly be followed by a listing or spinoff of the Swiss Bank, worth CHF 10bn.

The Swiss National Bank stepping in with full deposit guarantee or injecting equity. That would give Credit Suisse time to restructure but it would be highly dilutive for existing shareholders.

A “self-help approach” with the closure of the investment bank. Still, this may not be enough to reduce market concerns.

Thanks to the regulations, bank is allowed to continue without going bankrupt overnight, while imposing losses on equity and subordinated debt holders (for the time being). Senior debt is the last to be hit and CS has a large outstanding amount of AT1 coco subordinated debt (CHF 15bn book value): if CS has to recapitalize, AT1 and equity holders would be forced to take losses and the senior debt would be protected (in fact, CS recently announced a senior debt buy back).

In the meantime, today the ECB just raised interest rates of 50bps, confirming that inflation is the main concern. Asked whether the latest turbulence could herald a repeat of the last global financial crisis, Lagarde said “the banking sector is in a much, much stronger position than where it was back in 2008.”

This suggests that CS event, like SVB, does not seem to be systemic as Lehman bankruptcy in 2008. These banks are paying the huge stress of this market. In a month we could have already moved on from CS, but with risk and volatility premiums likely to remain elevated for some time. However, credit spreads are already pricing in meaningful default risk in both Europe and US.

Our conclusions

We believe earnings are going to be under pressure and bank is unlikely to be profitable soon. They have large restructuring and legal costs, amid a deposit base bleed, requiring more short term funding. Last but not least, they lost market access for their funding and have very limited ability to delever. The Senior ratings will likely be downgraded to deep “junk” category.

We believe that the CS Senior bonds are the best place to be in the medium term, while Subordinated bonds can be only used for trading purposes. Although the serious bank’s problems we don’t believe the Senior bonds will go busted. On the other hands, depending on how the CS crisis will unfold and the kind of intervention the SNB is going to have in the future, the Subordinated bonds can be pretty risky and we see a not negligible probability that they can be converted in equity.

After a gap up at the beginning of the trading day, following the SNB intervention, we saw the bond prices to fade. We are seeing interest from the market in particular on the low cash bonds. The desk is putting all its efforts to serve its clients offering the a deep pool of liquidity.

Please contact us for more insights and updates