Fed, inflation and S&P. What the Street thinks

A short recap from the main guys in the Street

Fed pivoting & inflation. Analysts opinions:

Goldman Sachs:

"We are raising our Fed forecast to include a 75bp rate hike in September (vs. 50bp previously) and a 50bp hike in November (vs. 25bp previously). We continue to expect a 25bp hike in December, which would take the funds rate to 3.75-4% by the end of 2022."

HSBC:

"Our view has been and is that an imminent Fed pivot is wishful thinking […] which has driven our max underweight in equities. […] While markets increasingly accept this as a reality, sentiment and positioning has only dropped slightly so far".

Citi writes that their global supply chain pressure index has eased a lot in August. We are now at the lowest levels since late 2020. Central drivers of inflation are basically easing according to the investment bank. They also write:

"Our empirical analysis suggests that goods inflation could fall rapidly in coming months. While uncertainty around such estimates is high, at a minimum the easing of supply chain pressures is an encouraging step in the fight against inflation."

Morgan Stanley:

“Sharply lower energy prices will move sequential headline inflation into negative territory […] Core inflation should also remain relatively soft as core goods prices decelerate. […] However, rent inflation is likely to remain strongly elevated for some time, keeping the Fed on a steep tightening path”.

BofA:

"In our view, declining liquidity and resiliency of the Treasury market arguably poses one of the greatest threats to global financial stability today, potentially worse than the housing bubble of 2004-2007."

The relief rally arrived. S&P 500 3900 level looks to be a key magnet since July. But many expect new lows in the next months.

We expect the current rally has legs to meet the 50 DMA around 4’050, then we expect markets will resume the downward path.

Analysts opinions:

Interactive Broker – Thomas Peterffy: US stocks haven’t fallen enough to account for the elevated inflation pressures that will drive the Federal Reserve to keep interest rates high for a sustained period of time. He told Bloomberg S&P 500 won’t hit a bottom until it trades to levels between 3300 and 3500.

“We have these deep issues of de-globalization, ESG, lack of skilled labor and continuing deficit spending and increasing debt service costs. So they all contribute to inflation.”

To prepare for upcoming volatility, his hedge-fund customers are holding record levels of cash reserves, he added.

Goldman Sachs sees three reasons why a genuine bear market trough has not yet been reached:

Inflation and interest rates will likely have further to rise.

Economic growth is likely to weaken.

Valuations and positioning are not at extremes.

The conclusion: "we have not yet met these conditions, suggesting further bumpy markets before a decisive trough is established".

JPMorgan:

"Today’s rally in equities was mainly driven by the bond market and characterized by short-covering."

Deutsche Bank:

“In the event we slide into a recession, the sell-off has much further to go (S&P 500 3000); but if we do not, we expect the market to rally back sharply to its prior peak. […] We maintain our S&P 500 target for year end at 4750.”

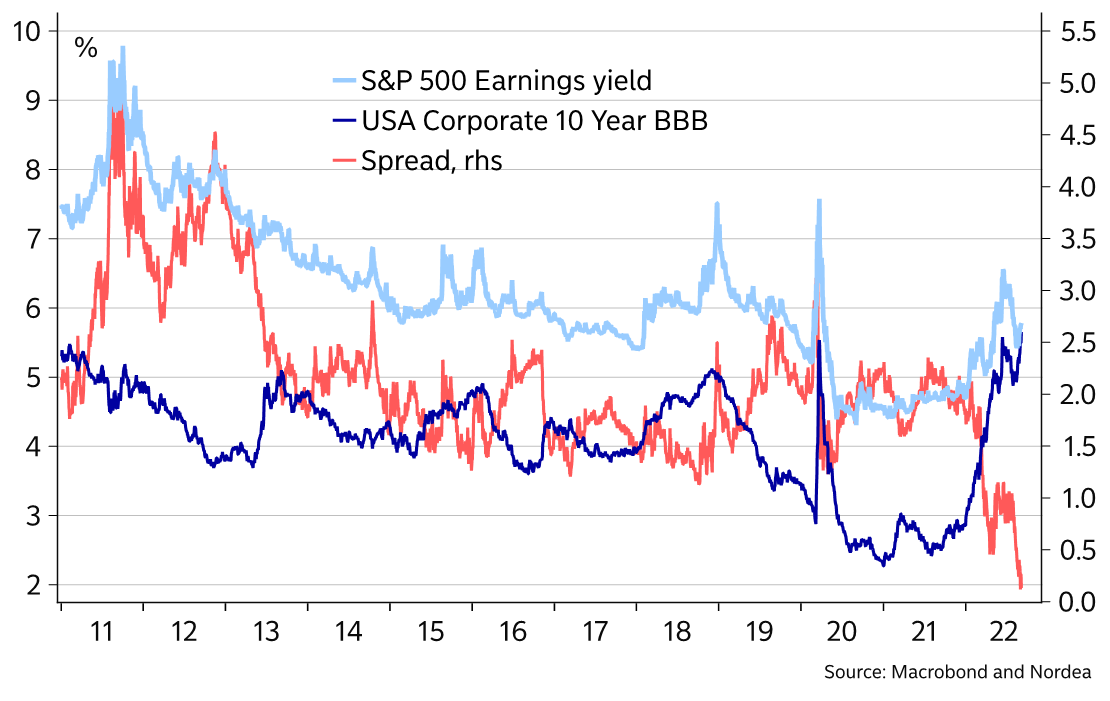

What about valuations? Equity investors not getting paid for the risk.

Macrobond, Nordea and TS Lombard share the same idea, with the latter saying:

"Equity risk premia have fallen to the lowest level since 2009 – except for a short dip in 2020. This points to the same conclusion as credit spreads, i.e. that risk compensation in equities, despite lower p/e ratios the market is trading at compared to the start of the year, remains historically low."

Finally, options activity is at record levels… 3x times 2008 ???

No, not that bad! But still very high volume. If the same metric is normalized by equity market cap, the outcome is less scary.

However, institutional option trading activity is on par with the financial crisis in 2008. Last week, institutional traders bought US$ 8.1bn worth of put options and less than US$ 1bn in calls.