Fixed Income Monthly Report - September 2023

Preview of our monthly publication with macro themes and single bond ideas

Every month, we publish the Fixed Income Monthly report. The report is a synthesis of the Ashenden’s team view on Fixed Income, pursuing a global approach through the full spectrum of the asset class and providing bond picks. We range from Investment Grade bonds to High Yields & Emerging Markets.

In the report we disclose our bond model portfolio (6 years track record) with more than 60 individual names. We include new single bond ideas, switches, new entries and exits.

All this is corroborated by a bottom-up analysis for each single position (new and old) and merged with a top-down consideration so to include the key market drivers.

This is one of the research piece our team produces internally. The intent of the report is to support wealth managers/asset managers in their decision and allocation process.

Underlying you can find a summary of what you can find inside this report.

September edition

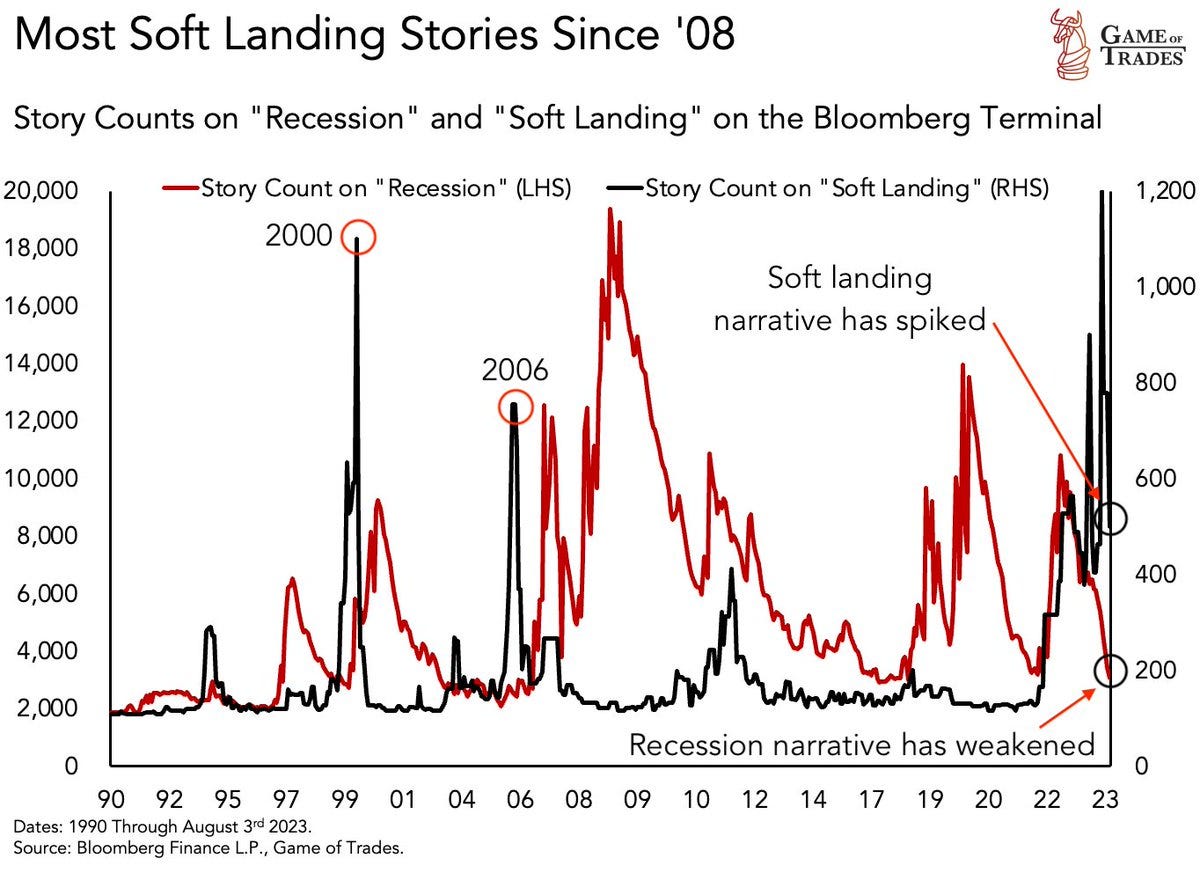

Goldilocks narrative is fading

In August the narrative that the Fed had delivered a rare soft landing has peaked. A steady stream of news helped drain enthusiasm from equity markets through most of August, snapping a five-month growth streak, with a near 5% drop in the S&P 500 since late July.

Expectations around disinflationary growth, fuelled in part by assumptions about the transformative potential of generative AI and a Goldilocks setup, have finally faded.

During the past couple of weeks markets have rebounded with hopes of no more hikes on the back of weaker economic data. So, it is not surprising that rates pulled back and has been the driver for the recent equity performance.

As Canaccord recently commented:

“The violent moves in both directions for opposite reasons over such a short period of time make clear that investors have no idea what comes next”.

The S&P 500 is down 1.8% for the month; the Dow Jones Industrial Average is down 2.4% for the month and, finally, the Nasdaq Composite is down 2.2% for the month. The 10-year Treasury note yield closes the month at 4.098%, after peaking at 4.34%. World debt is now around US$ 225tn.

China growth faltered

China’s post-pandemic economic recovery has faltered in recent months, as exports weakened and a housing crisis intensified. Signs of financial stress are aplenty, with a property giant on the verge of default and a major shadow bank’s missed payments triggering fears of worsening contagion. The real estate sector, accounting one third of the Chinese gross domestic product, is in a full slowdown with sales by the country’s largest developers falling 34% in August from a year earlier.

Issues of demography, slackening rural-to-urban population migration, geopolitical fracturing and subsiding private sector dynamism represent structural economic challenges not easily mended with normal controls like looser monetary policy. As the consequence of top-down political policies, they will demand a political policy solution.

Last week, China unleashed a slew of measures to halt a slide in the country’s residential property and shore up its ailing economy. The policies have drawn mixed reactions on whether they will be sufficient enough to instill confidence in the economy and spur growth. Those include fiscal incentives, mortgage easing, home-loans cuts, down payment reductions, urban renewals and others.

Disappointments in China are also likely to reverberate, impacting global demand, currencies and US rates, as policymakers could scramble to revive confidence.

Credit overview: stay defensive and take advantage of generous rates

Global risk sentiment is less than ideal as healthy economic data from the US and darker clouds over China cast a shadow on both stock and bond markets. The fear of a decidedly hawkish Fed is already priced in, and if there is no more hawkish surprise during the next central bank meetings, tensions among investors could ease and give markets some breathing room in the short term.

We remain convinced that the prospects of a “soft landing” are very unlikely. Consensus opinion is of the view that a meaningful economic recession will be avoided. The heavily lagged effects of central bank policy changes often result in hopeful expectations of a no landing (or at worst for a soft landing). Ironically, such optimism is often at its greatest just before evidence of a recession becomes apparent.

Having said that, we continue to see High Yield bonds as expensive given the deteriorating performance of many companies in the space. Risk premiums, or spreads, on junk bonds averaged about 385bps, close to the lowest level of the year and below the average of the last decade of 430bps. In times of market turmoil, high yield spreads can reach 700bps or higher.

High-yield spreads are below their long-term averages:

Also, spreads between the lower tier of Investment Grade corporate bonds and treasuries shows no signs of stress in the credit markets (not yet).

The last time High Yield spread was this low was the 2007. Then, spreads had just begun widening in front of what would soon evolve into the Great Financial Crisis. We are not suggesting we are going into the same turmoil, but better to keep in mind how tight credit spreads are.

One technical driver that definitely helped junk bond valuations during the past couple of months have been the relatively light sales this year, which supported to keep risk premiums low for many issuers.

On the other hand, we should factor in the approaching maturity wall, that becomes increasingly heavy, starting in 2024 and going into 2026. We should expect a wave of corporate debt refinancing over the next six months. For companies, many of which borrowed heavily during the pandemic, the big refinancing wall is about to start and should peak in 2026. High Yield firms in Europe have over €450 billion of debt due in the second half of the decade.

Borrowers are currently not feeling the full pressure of the interest rate because they are sitting on locked rates at low levels, which is about to change. And this is going to be a huge shock because company will refinance at 3/4x or more, given the higher rates environment today.

Meanwhile, corporate earnings show that key measures of income are falling relative to interest expenses, among other signs of deteriorating performance. Corporate profits contracted by 6.5% YoY in 2Q23, acceleration to downside from prior quarter’s 1.8% decline; worst drop since pandemic.

The combination of deteriorating corporate performance plus low risk premiums means it makes sense to look away from High Yield, into other more appealing segments as Corporate Hybrids, Financial Subordinated, Emerging Markets or looking to park into the safer short term Investment Grade space.

Moody’s forecasts that the global default rate for junk-rated companies will surpass the historical average by the end of this year, before peaking at 4.7% in March 2024. For Europe, it is predicted to peak around 3.8% in the middle of next year.

We continue to overweight Investment Grade bonds and, in general, credit quality, with attractive yields. Higher yields reflect the view that monetary policy in US and Europe can remain sustainably tight. We want to surf this temporary narrative, as we believe we are close to the rates peak.

Emerging Market bonds: they will come back in focus soon

Emerging Markets remain an interesting case, as riskier nations and companies will need to keep exploring new ways to raise money or revamp their finances as the door to international debt markets stays shut.

Tighter global financing conditions as central banks battle to bring inflation to heel has kept the door to international debt markets firmly closed for Emerging Market issuers with a riskier credit profile. Higher global borrowing costs are, however, forcing issuers to embrace austerity and get more serious about debt sustainability.

For example, the sale of dollar bonds from developing countries sunk to the lowest since 2021 in August as global yields spiked to multi-year highs and 15 emerging nations traded at distressed levels. Only $1.4 billion has been raised in emerging debt this month, compared with $4.5 billion in August 2022 and average monthly sales of $15.4 billion this year.

Partly due to the dearth of new sales, the average yield on Emerging Market sovereign debt has recently hit a nine-month high of 8.43% when China’s economic troubles sparked a selloff.

For the reasons above, it is a good time to explore specific stories in this EM lower rated space on a very opportunistic basis. The next quarters will be very interesting from this point of view and we expect a come back of focus and inflows in the asset class.

Next, we updated our monthly model portfolio, studying its performance and adding new bond ideas:

New ideas

Ideas reiterated and business case updates

Exits

The fixed income model portfolio includes Investment Grade and High Yield bonds.

If you would like to receive a copy of the publication and subscribe to the monthly releases, contact us in order to have more information!

The hope for a soft landing has now become a certainty among many but I think you're going to be right about this; "...that the prospects of a “soft landing” are very unlikely." Thank you.