Forget USA: money is flowing abroad

Volumes are surging in Asia, Europe and EM

Everyone goes to Asia

Asia is one of the hot themes of 2023 until now. China’s growth, which, according to many, could lead the Chinese indices to be the undisputed leaders for the year. Moreover, the topic of the BoJ monetary policy is quite trending. It has a number of knock-on effects chain effects of no small magnitude.

Investors are flowing into A shares:

BofA Fund Manager Survey is confirming volumes are shifting away from US:

"China & Fed optimism caused cash level dropping to 5.3%. Market rotating to EM, EU, cyclicals from pharma, tech, US stocks but no “up-in-equity” positioning… Q1 risk asset 'pain trade' remains up".

Being underweight the US market also means being underweight the equity markets since: US market weighs 67.7% of MSCI World developed market and 59.04% of MSCI World. Japan and China just to weigh 6% and 3.32% respectively.

BofA is also saying China is driving USD more than Fed hikes Strategists tracked a measure of Chinese “reflation assets” vs a dollar index. The correlation between the two, tightened since November, suggests sentiment around China emergence from Covid lockdowns will continue to move the greenback.

China’s yuan has climbed more than 2% against the dollar so far this year. It could see more upside in 2023, given the economic forces on the currency:

Covid zero exit

Fed approaching end of tightening cycle

PBoC may also slow the trend

Goldman Sachs upgraded on Tuesday its forecast for China’s gross domestic product growth this year after the government reported stronger-than-expected economic data and the recovery gathers pace. Their economists are projecting China economy will expand 5.5% this year (up from 5.2% previously).

China Q4 GDP grew 2.9% compared to the Q4 22, beating expectations for a 1.6% yoy expansion as zero-COVID winds down.

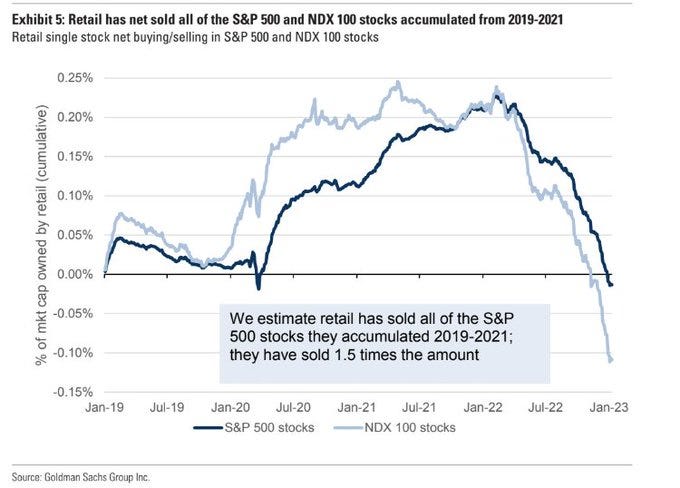

JPMorgan formerly reported retail outflows from equities totalling US$ 3.1bn. According to Goldman, US retails sold all of the stocks they accumulated during 2019~2021, and went further beyond to capitulate.

According to Carrhae Capital (Hedge Fund on Asian EM), Chinese equities will outperform global peers in the first half of this year, and is betting on the nation reopening. Last year Carrhae Capital long-short strategy performed +15.3% (vs average -7% of its competitors.

And then there is Japan.

BoJ decided to keep monetary policy unchanged. The market had speculated another hike of the cap over 10Y yields could come and was left disappointed, which triggered a rally in USD/JPY above 131. A policy rate hike to 0% and another hike in the yield curve control target awaits in 2Q23.

Yen fell against dollar.

Don’t sleep on Europe

European stocks are outperforming their US peers, partly on notions corporate results may meet or beat forecasts. European earnings estimates of 0.6% growth for 2023 are the lowest ever at the start of a year, according to Sanford C. Bernstein, and the market expects fourth-quarter profits to show the weakest growth in two years, Barclays strategists say. There's "room for more short covering if earnings meet expectations" said Emmanuel Cau at Barclays.

Saxo Bank: Rising volume of trades on Euronext Paris. In recent sessions, we have noticed a strong rise in the volume of trades and a sharp increase of volatility for several small and medium companies listed on Euronext Paris. There is also a jump in speculation for companies using dilutive financing in the form of OCABSAs ((bonds convertible into shares with share subscription warrants). In October 2022, the French stock market authorities, the AMF warned against the risks associated to this financing, especially for retail investors.

Europe had also been “lucky”, thanks to the weather. High temperatures of November and December have reduced the demand of Gas, bursting the bubble of these months for this commodity class. This contributed to reducing inflation.

But this could change in the upcoming months as winter is not over yet.

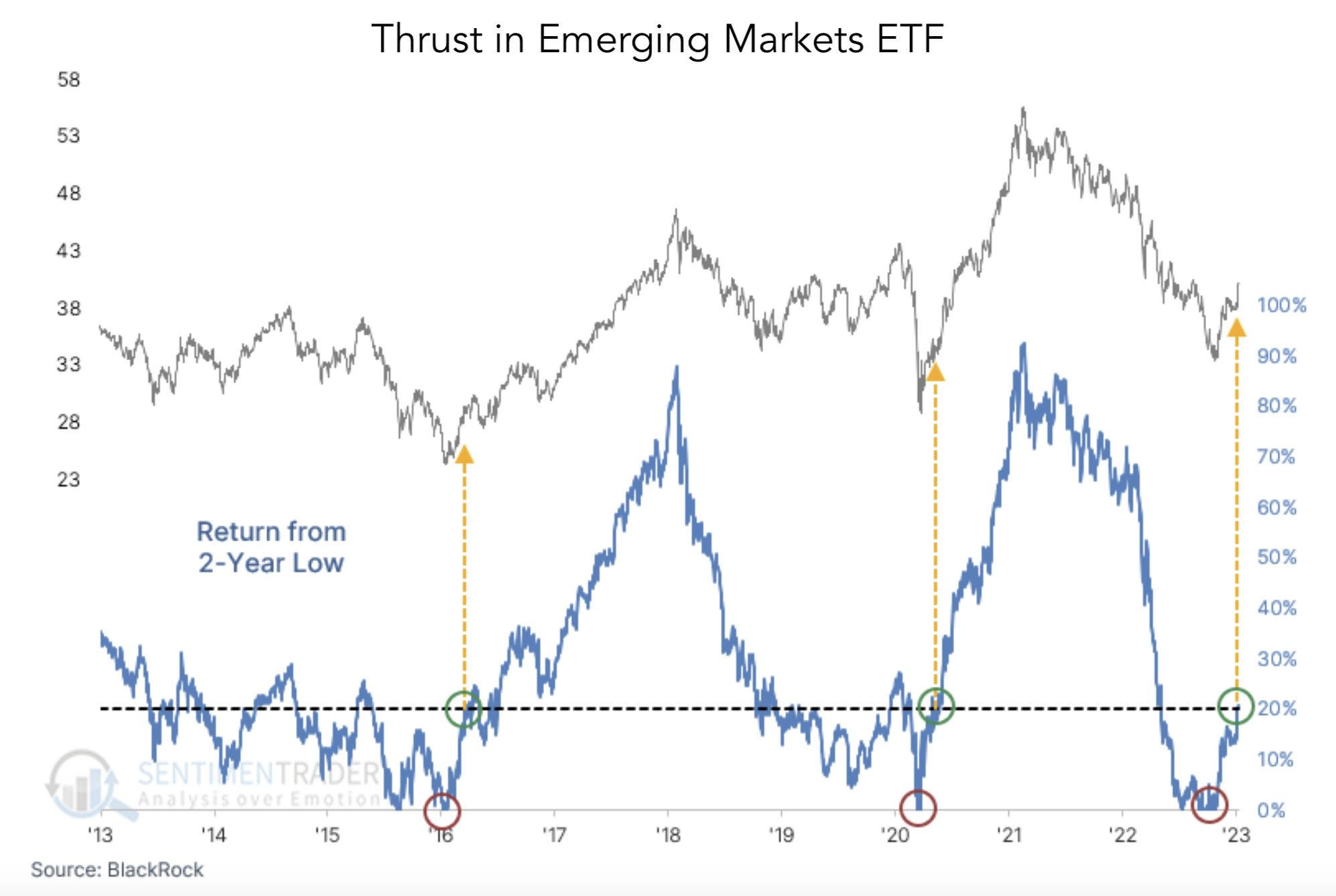

Emerging Markets coming back?

Emerging markets have seen a big shift towards bullish momentum. Return from 2-year low has spiked from 0% to 20% and this has marked the beginning of some incredible runs.

Another factor: dollar weakening has favoured emerging markets. At the same time, a weaker dollar means less expensive raw materials for European countries: lower costs of production and thus more profits (for companies not exposed in US).

Situation could change at any time (China stops reopenings, winter strikes in Europe, inflation slows in Europe and EUR weakens), but shorting US is a hot theme at the moment.

nice take, thank you!