Global economy temporary resilience

Market insights, data and analysts thoughts on this economy

The market now

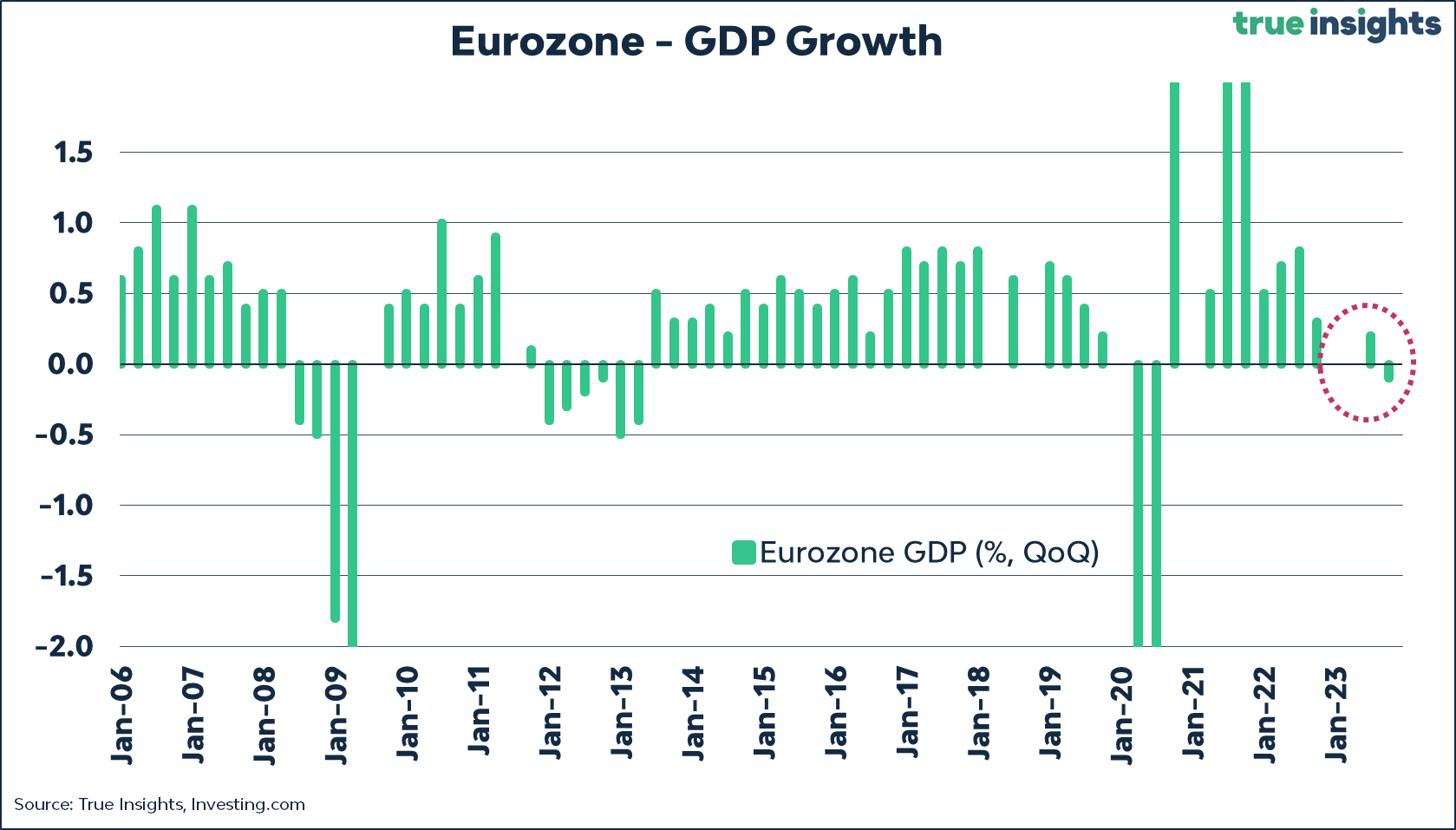

IMF: Europe’s economy is unlikely to crash — even as a more-than yearlong bout of rate hikes tames inflation. “The outlook for Europe is for a soft landing, with inflation declining gradually,” the fund said, forecasting 0.7% growth for the Eurozone in 2023 and 1.2% in 2024. While that seems a bit too optimistic – the Eurozone economy has grown a paltry 0.025% on average during the last four quarters – it hardly matters from a debt perspective. The Eurozone is expected to run a budget deficit of 3.6% of GDP this year and 3.0% next. Debt-to-GDP ratios – already elevated – will further increase even without a crisis or recession (which may still come by the way).

US Interest Rates. The bond market is betting on a “dovish pivot” for the seventh time since the Federal Reserve and other central banks embarked on a tightening cycle, raising the prospect of another false dawn, according to Deutsche Bank macro strategist Henry Allen. US Treasury yields turned sharply lower and bonds rallied in the wake of last week’s Fed policy meeting, at which US central bank Chair Jerome Powell hinted that the current rate-hike cycle may be near an end. The buoyant mood gained further momentum from signs of a softening US jobs market.

Treasuries are the most attractive they've been relative to U.S. stocks since 2001.

A record flood of cash has poured into opposite ends of the Treasury yield curve, seeking either to seize on the highest short-term interest payments in over two decades or to profit from a long-bond rally once rates finally peak. “The current shape of the yield curve definitely makes it compelling to park cash in the front-end, but with people more worried about the potential for a slowdown and the recent bear steepener, the long-end is looking much more enticing,” said Winnie Cisar at CreditSights.

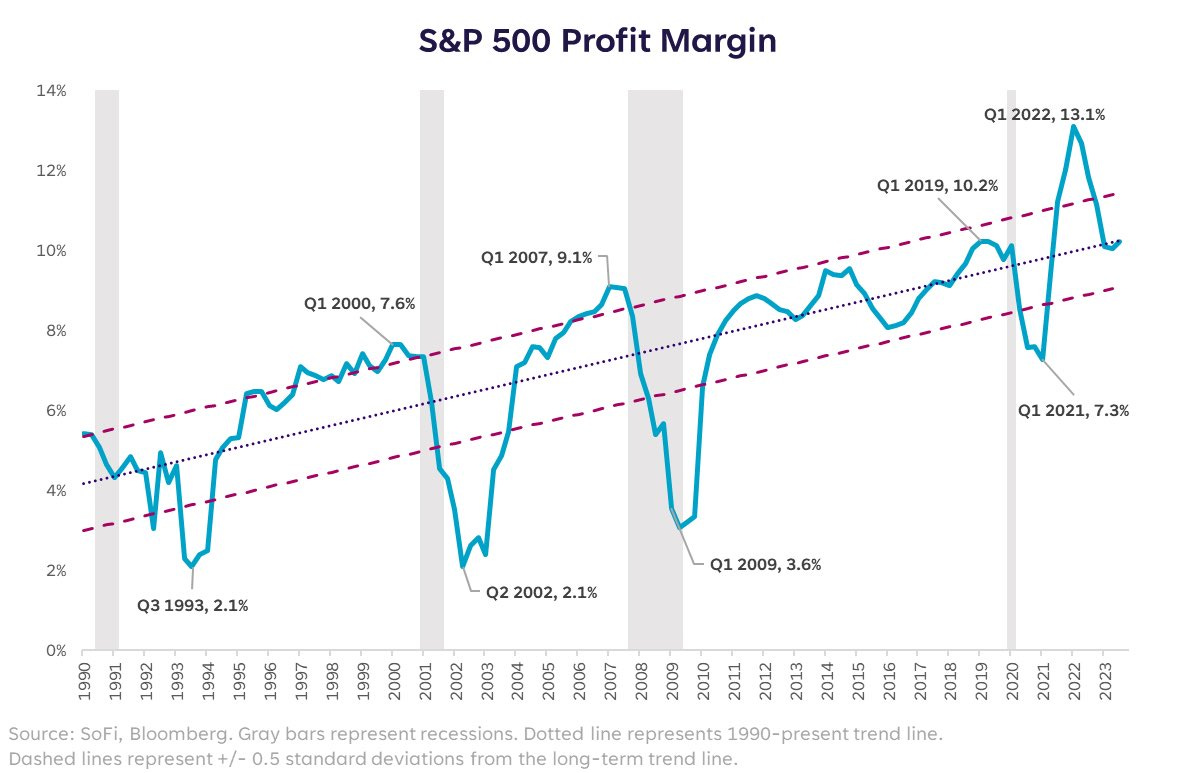

Equity side: for now, S&P 500 margins seem to have stabilized right around the historical trend line.

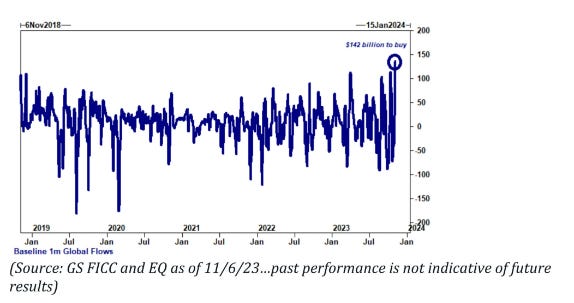

CTAs will need to buy approximately US$ 142bn in U.S. Equities over the next month, the highest amount ever recorded.

Nasdaq has traded green for 8 consecutive trading days, the longest winning streak in 2 years.

Goldman Sachs actually says there is no need for a recession.

"Despite the good news on growth and inflation in 2023, concerns about a recession among forecasters haven’t declined much. Even in the US, which has outperformed so clearly on growth in the past year, the chart shows that the median forecaster still estimates a probability of around 50% that a recession will start in the next 12 months. This is down only modestly from the 65% probability seen in late 2022 and far above our own probability of 15% (which in turn is down from 35% in late 2022).”

What is actually happening

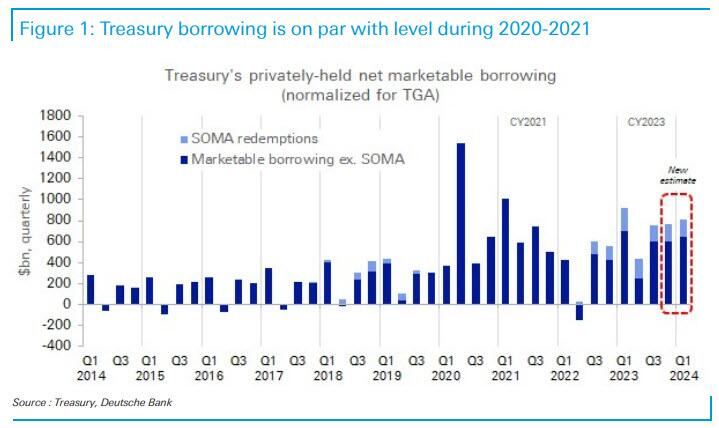

As analysed by ZeroHedge, Treasury averted a bond market "earthquake" last week, but everyone is missing some key points in TBAC's refunding presentation. Recall that last week's refunding announcement sparked a powerful rally under Treasuries (which sent yields tumbling at a time when everyone was terrified of a spike above 5%) because contrary to Wall Street expectations of a US$ 114bn in coupon offerings during this refunding week, the Treasury projected "only" US$ 112bn.

But what really hammered the nail in the coffins of Duration bears was what may have been the first instance of "forward guidance" in the Refunding Announcement, traditionally a mechanism of nudging market expectations used by the Fed, now being adopted by the Treasury!

Specifically, the Treasury said that it now expects a single additional step up in quarterly issuance of longer-term debt, hinting that there will be at most another burst of new issuance during the next refunding... and that's it. To wit:

"Based on projected intermediate- to long-term borrowing needs, Treasury intends to continue gradually increasing coupon auction sizes in the upcoming November 2023 to January 2024 quarter. As these changes will make substantial progress towards aligning auction sizes with projected borrowing needs, Treasury anticipates that one additional quarter of increases to coupon auction sizes will likely be needed beyond the increases announced today.”

But as underlined by Deutsche Bank, total debt issuance would still be massive, only instead of coupons, it would be more focused on Bills.

And it is full of worrying signals pointing to an incoming recession.

In Europe, Mario Draghi sees a nearly certain recession by the end of 2023. Former European Central Bank President said (Financial Times):

“The starting point of this recession is pretty high — we never had such low unemployment. So we may have a recession, but maybe it is not going to be destabilizing.”

While in America, US credit slowing for the 3rd time in 50 years. For only the 3rd time in the last 50 years, commercial bank credit has declined by more than 2%. The other 2 times were the peak of the Dot Com Bubble and the aftermath of the Global Financial Crisis.

Morgan Stanley expects continued credit deterioration. 1) reserve builds came in higher than expected at 6 of the 9 Consumer Finance names MS cover. 2) several management teams expressed more cautious expectations. 3) average credit card delinquencies continued to accelerate - the latter development was contrary to the MS team’s expectation of stabilizing Y/Y growth.

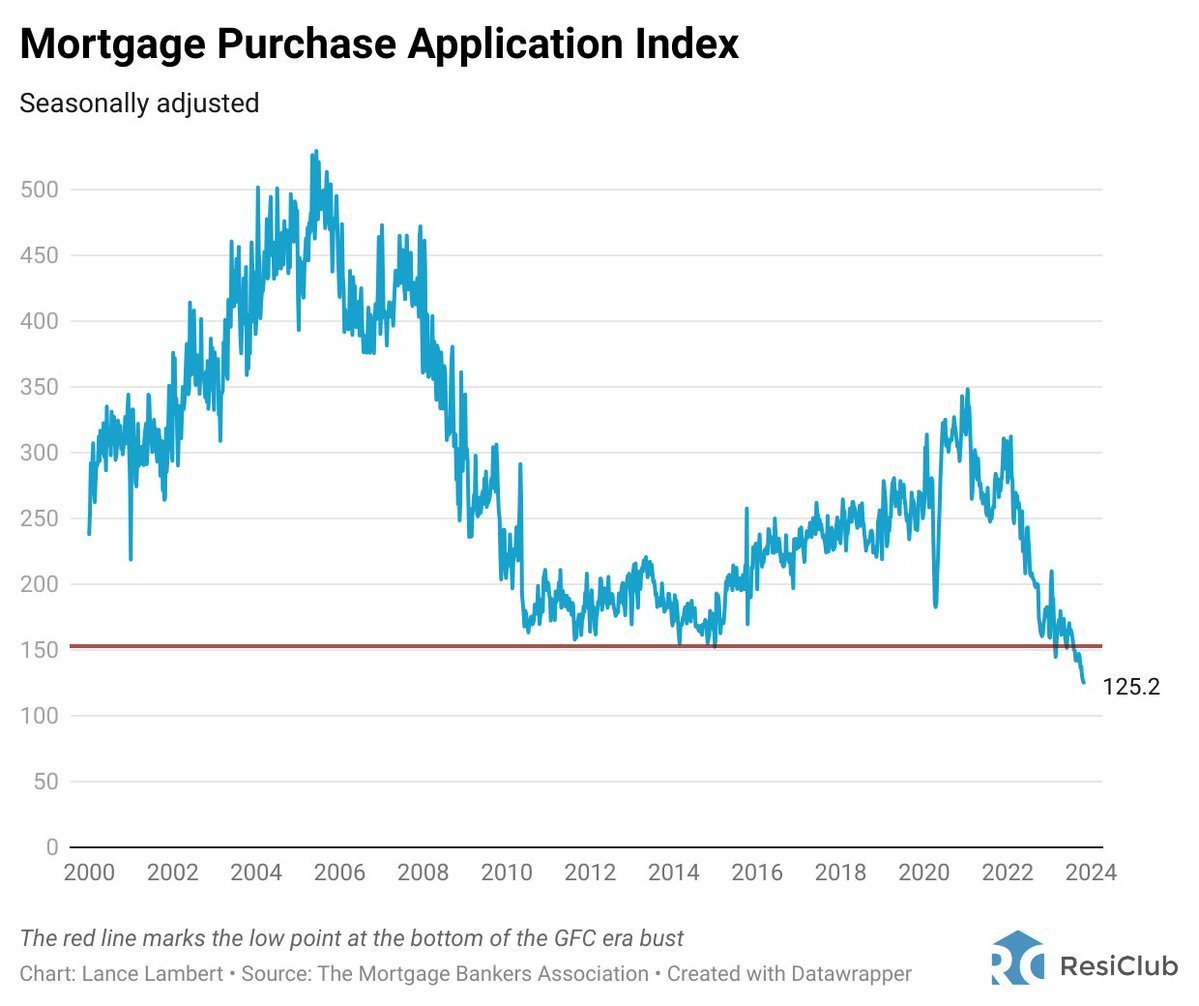

US mortgage market is experiencing a severe recession. It's one of the worst downturns in mortgage market history. And last week, mortgage purchase apps hit the lowest level of the post 1995 era.

Morgan Stanley: The proportion of consumers being late or missing a bill or loan payment rose last month to 40% from 34%. Low-income consumers are more likely to have missed or late payments. Consumer electronics and computers continue to post lower negative net spending compared to essential categories. Alcoholic beverages, durables and clothing/apparel are also trending negative, similar to last few months.

Largest cuts to S&P 500 EPS estimates over the first month of a quarter since Q2 2020. During the month of October, analysts lowered EPS estimates for the fourth quarter by a larger margin than average. The Q4 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q4 for all the companies in the index) decreased by 3.9% (to US$ 55.61 from US$ 57.86) from September 30 to October 31.

CTAs are currently short US$ 134bn worth of global equities, the largest short position in 5 years.

SocGen sees a case for equity volatility moving higher, but not yet. This is a very long term chart, but something to keep in the back of your longer term hedges: "In the event that the Fed keeps rate high for a longer period, our model is likely to forecast an even sharper rise in equity volatility over 2025 – leading to an extended period of high volatility."

Morgan Stanley's Mike Wilson: Open-minded...but it looks like a bear market rally.

"While we will keep an open mind, the move thus far looks more like a bear market rally rather than the start of a sustained upswing, particularly in light of weaker earnings revisions and macro data…"

JPMorgan's uber-bearish Marko Kolanovic rages at JPMorgan uber-bullish trading desk. Kolanovic said that while "falling bond yields and dovish central bank meetings were “knee-jerk positive for equities” for short term, but growth-policy tradeoff will remain challenging into year end" while the prospect of sustained elevated interest rates and slowing growth come back in focus. And “as the Fed is set to remain higher for longer at the short end, markets could start to price in a policy mistake, leading to lower long yields down the line, and that might not ultimately be helpful for stocks, especially if 2024 earnings projections start to reset lower.” Meanwhile, "divergences between softer activity momentum and the elevated equity prices, as well as market internals that opened up in the summer, have not closed yet" and while yields might be peaking, "the real rates vs P/E gap remains meaningful. In addition, Brent and USD moves could impact stocks unfavourably." ZeroHedge

Goldman Sachs: Buybacks do not care about your bearish feelings. US$ 5bn per day keeps the bear market away. Nothing new, but the unrelentless un-emotional buyer is here in full force. GS buyback desk:

"79% of S&P 500 is currently in the open window ending 12/8/23. We estimate US$ 5bn worth of daily VWAP demand during this open window with some of the largest repurchasers coming back online now. November and December are the best two month period for executions of the year. For those corporate running a lower execution pace YTD, November would be the month to increase above our expectations."

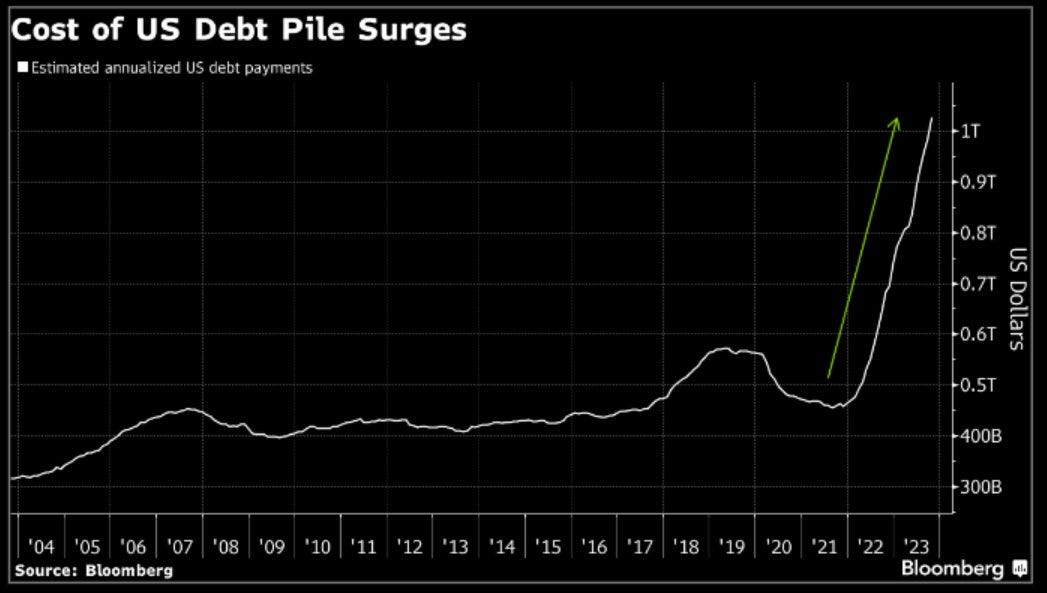

Estimated annualized interest payments on the US government debt pile climbed past US$ 1tn at the end of last month, an amount that has doubled in the past 19 months.

US Deficit: BlackRock’s Wiedman said “no one’s paying attention” to the fiscal unsustainability of the US and that the risk isn’t priced into the markets. “One morning, people are going to wake up and decide that this is one of the most important forces in global capital markets,” said Wiedman. “Yields will rise and every asset in the world will be repriced.”

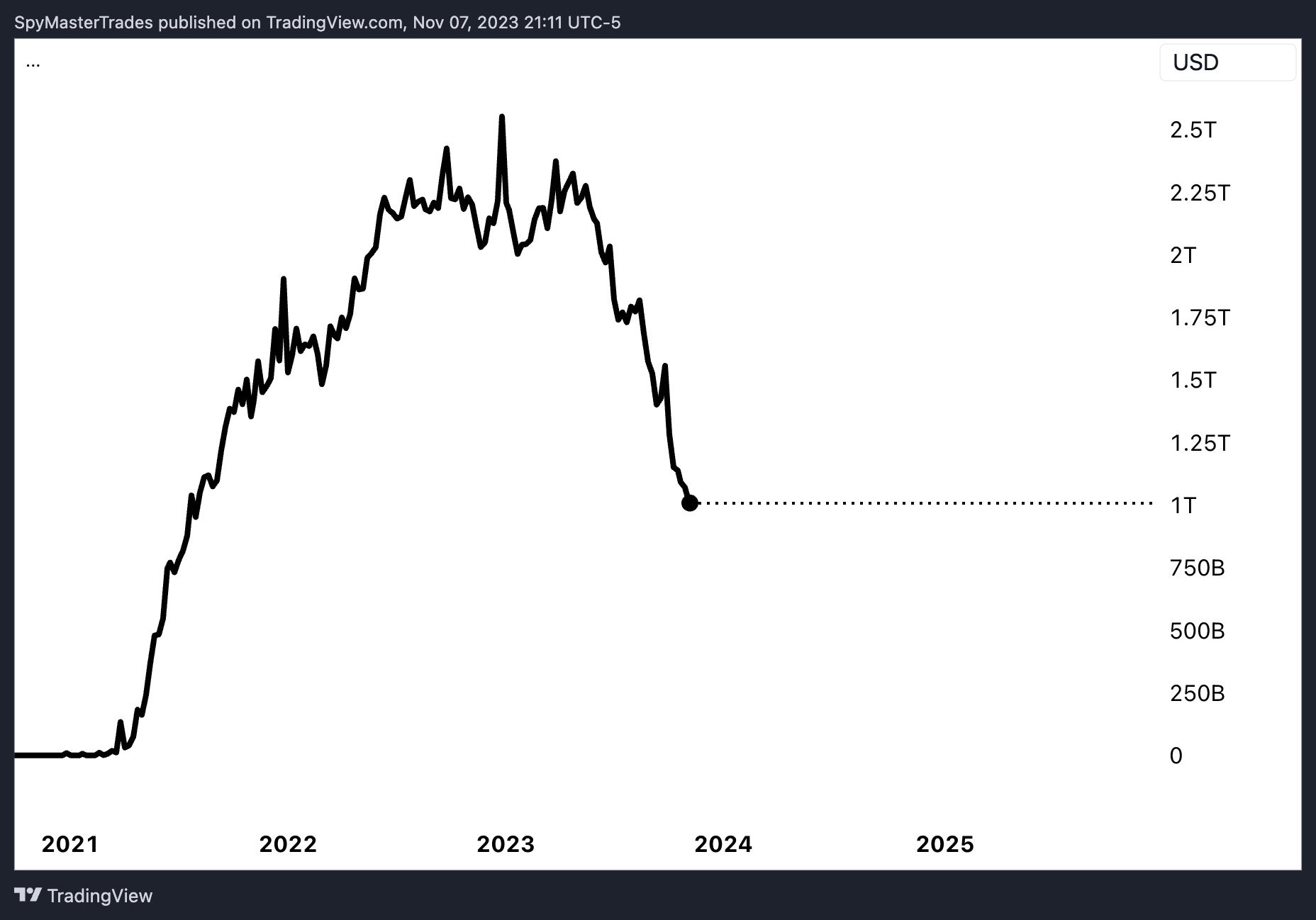

Demand for the Federal Reserve’s overnight reverse repurchase facility dropped on Tuesday to the lowest level in more than two years as counterparties withdraw cash to finance purchases of Treasury bills. On Tuesday, 97 counterparties parked US$ 1.009tn at the RRP, the lowest since August 2021, and down from US$ 1.063tn the prior session. Time is rapidly running out for the Fed to pivot. The Fed will soon have to resume massive new currency creation, even as inflation remains high.

BlackRock says a US$ 4tn pile of idle cash is a major issue facing global investors as they figure out where the capital is going. “There’s about US$ 4tn of cash that is sloshing around waiting for action. We don’t know when that cash will come back in but that’s the first big overhang that clients talk about all the time.”

U.S. banks have found a new way to unload risk as they scramble to adapt to tighter regulations and rising interest rates. JPMorgan Chase, Morgan Stanley, U.S. Bank and others are selling complex debt instruments to private-fund managers as a way to reduce regulatory capital charges on the loans they make. These so-called synthetic risk transfers are expensive for banks but less costly than taking the full capital charges on the underlying assets. They are lucrative for the investors, who can typically get returns of around 15% or more. U.S. banks mostly stayed out of the market until this autumn, when they issued a record quantity as a way to ease their mounting regulatory burden. WSJ

Big banks are sitting on US$ 650bn of unrealized losses, Moody's has estimated. It's a sign even Wall Street's best-known names are feeling the heat from the Treasury-market rout. Crashing bond prices sank Silicon Valley Bank earlier this year, and there may be more chaos to come. BusinessInsider

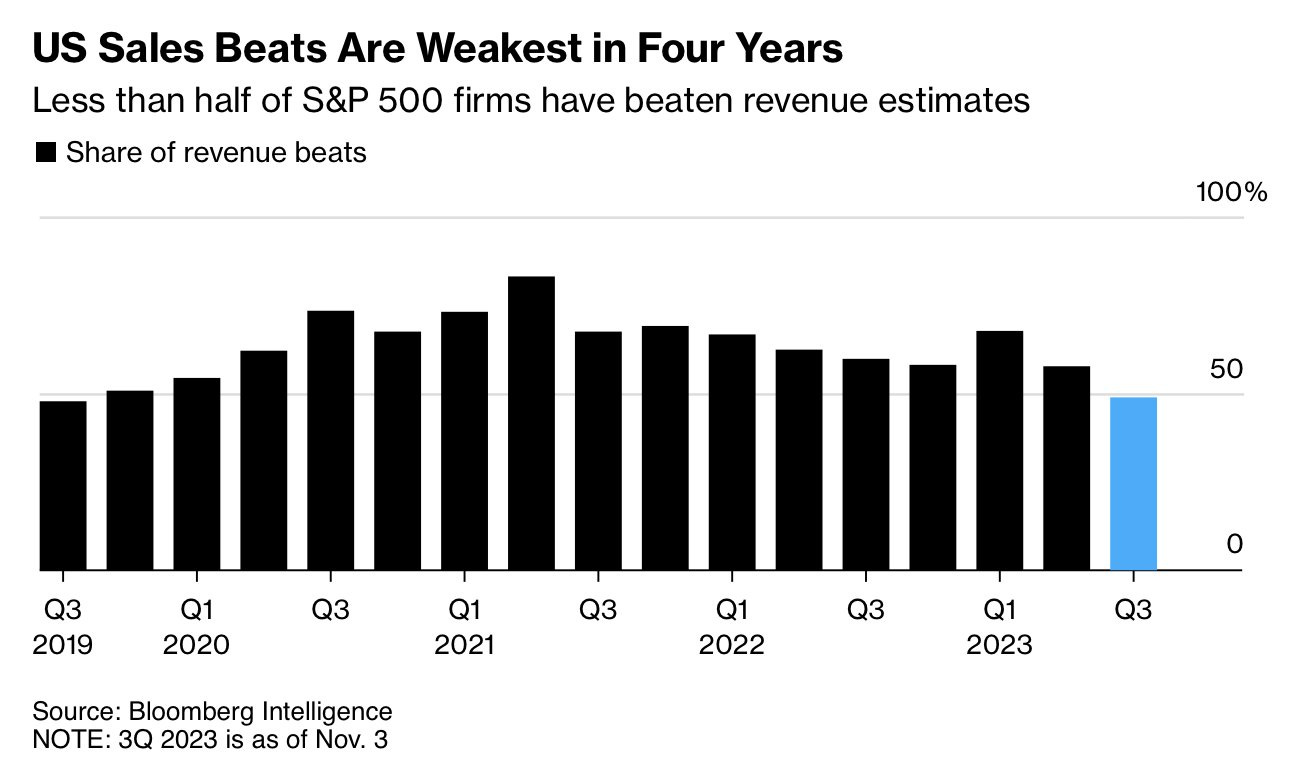

Corporate America is delivering the bleakest sales reports in four years this earnings season, a sign that weakening consumer demand is limiting companies' ability to raise prices further.

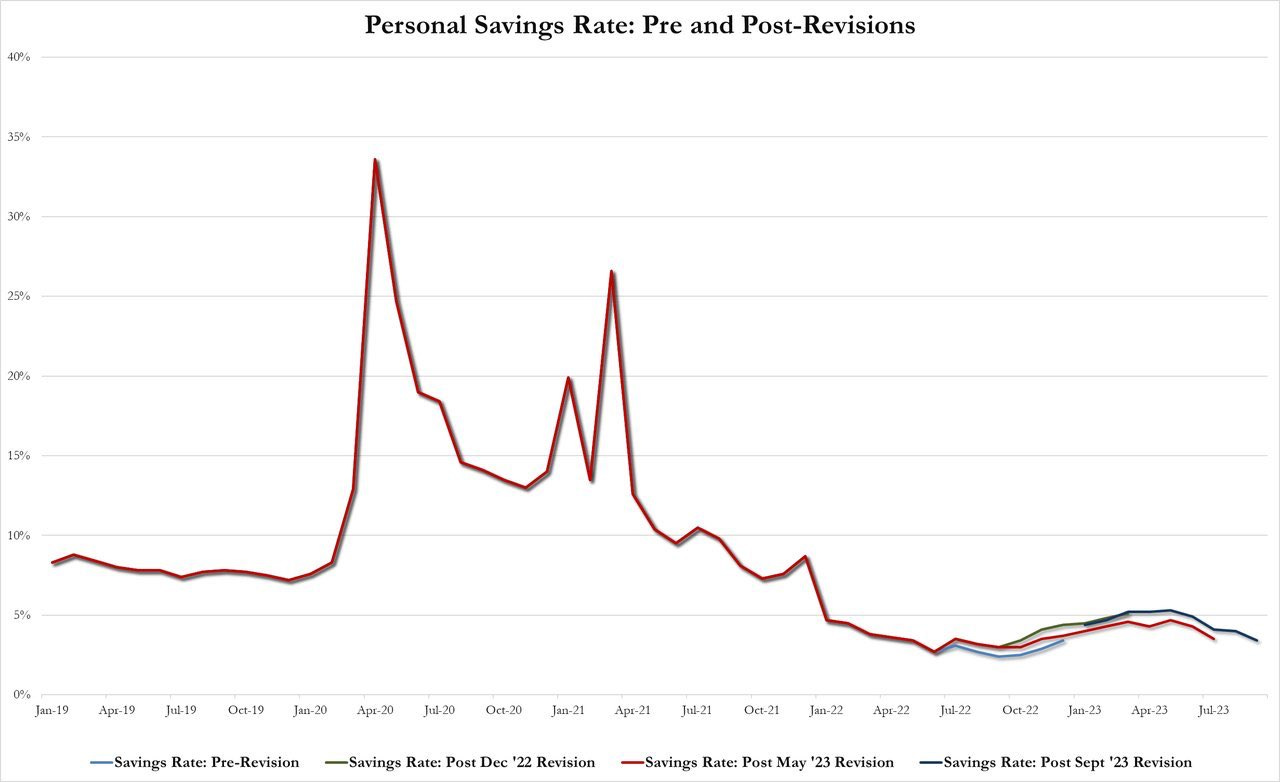

Personal savings rates are near their lowest levels on record, at 4%. Meanwhile, US$ 2tn in excess savings from pandemic era stimulus have been depleted.

Auto loans and credit cards delinquencies are rising. Newly delinquent loans are picking up rapidly according to the New York Fed's quarterly consumer credit report. For credit cards, the share of loans that are newly delinquent is at its highest level since Q3 2011. More people are failing to make on-time auto loan and credit card payments. “Despite sub-4% unemployment, delinquencies on auto loans and credit cards continue to rise sharply.

Wholesale used car prices are at their lowest levels since March 2021, down 19% from the peak. Should lead to lower retail prices in the coming months.

Excellent report, thank you!