Is everyone secretly bullish?

Market keeps going up, but the street keeps reminding it is bearish

This week is significant and full of events: we will see earnings of major companies (Exxon Mobil, Apple, Meta, Amazon, Alphabet) and, on Wednesday 1st February, Fed will announce their first decision of 2023 for the Federal Funds rate.

We will probably get a rate hike of 25bp, as analysed by Morgan Stanley. Their Macro team expectations:

The FOMC delivers a 25bp rate hike at its February meeting.

The statement will continue to highlight elevated inflation, even as recent data prints have pointed to a slowdown.

In line with recent commentary, Chair Powell will justify the step down in pace as a means to more carefully calibrate the stance of monetary policy while maintaining the Fed's commitment to fighting inflation.

The Fed is now reaching an estimated peak rate, but the FOMC is unlikely to signal the end of the tightening cycle.

During the press conference, Chair Powell is likely to emphasize the importance of the incoming data for the next policy decisions and may indicate that it will be appropriate to keep rates "restrictive for some time".

So, it will also be important to pay attention to the words used by Powell.

Investors are being cautions both in the equity and bond market, waiting for these major events before allocating their money. Plus, earnings are disappointing as commented by Barclays:

"Q4 results confirm what everyone seemed to have expected, i.e. slowing demand, margins pressure and an uncertain outlook for 2023, but are not a shocker either. The Fed and ECB meetings next week may matter more for the near term fate of the equity rally than earnings".

Nevertheless, 2023 started in green for both markets and hedge funds are betting on a downfall. They are mass shorting treasuries following the narrative that a peak in rate hikes is near and a US recession will push investors back into bonds.

The bearishness is also reflected in equities: investors have little confidence in US stocks even after this month’s surge, fearing weak corporate earnings could drag them back down, according to the Bloomberg MLIV survey.

70% believes bottom has not been hit yet and 35% thinks that we will reach lows on the second half of 2023. Even if the survey is just a small indicator, it is interesting to see that only a minority is bullish.

BofA January 2023 Credit Investor Survey: Recession remains the #1 investor concern, followed by Inflation and geopolitical risk.

Morgan Stanley Mike Wilson gives a suggestion for those still long: investors flocking to the equity rally will be disappointed as they’re in direct defiance of the federal reserve.

"We think the recent price action is more a reflection of the seasonal January effect and short covering […] investors seem to have forgotten the cardinal rule of ‘Don’t Fight the Fed.’ Perhaps this week will serve as a reminder".

JPMorgan's Mislav Matejka joins the party, saying investors should sell the rally even if markets keep moving higher:

"Q1 will, in our view, likely mark a turning point, as the fundamental confirmation for the next leg higher might not come, and instead markets could encounter an air-pocket of weaker earnings and activity, as they move through Q2 and Q3".

Even JPMorgan's Marko Kolanovic believes stock traders should fade this year's rally on expectations that markets will likely move lower as recession risks build.

"We believe investors should fade the YTD rally as recession risks are merely postponed rather than diminished".

This means that this year the risk seems to be on the upside. Investors are prepared for a decline: it is a potential rise that could cause panic (FOMO).

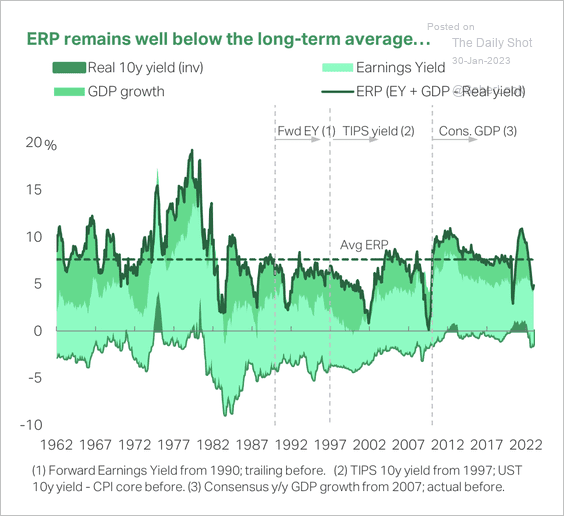

According to TS Lombard, the US equity risk premium is well below its long-term average. Lower valuations compared with 2022 mean earnings yields are more attractive. However, recession risks and higher Treasury yields put bonds ahead of stocks in terms of risk compensation.

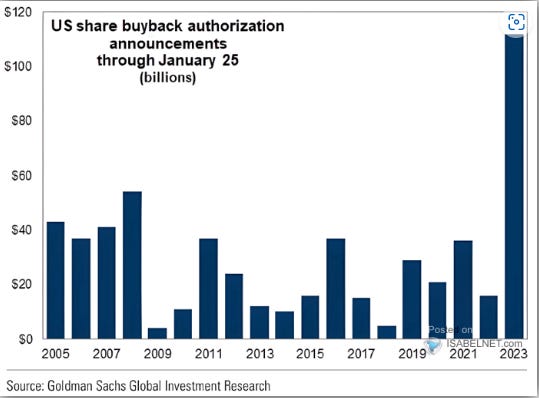

And why is the market rallying? For Goldman Sachs, stocks buyback is the answer.

But this does not provide a full picture. We have to take a deep look in Europe to understand what is happening.

According to top asset managers including BlackRock, European markets are too sanguine about the risks ahead. While the region is enjoying its best ever start to year, with stocks up 10% this month, there are five risks threatening the rally (Bloomberg).

War in Ukraine

Russia’s control of gas supplies to Europe continues to threaten economic growth. While a milder winter helped the region avert an energy crisis this time around, more policy intervention may be needed if Russia halts supply.

The energy war “could continue for a long duration,” said Aneeka Gupta, a director at Wisdomtree UK Ltd. “As we can’t always rely on favorable weather, measures such as shoring up gas reserves and rationing of energy demand will need to continue.”

Earnings Pain

Analysts have been slashing earnings forecasts going into the reporting season, with some strategists calling for even deeper cuts against the backdrop of slowing growth. With inflation easing, companies are also finding it more difficult to raise prices at a time when demand is slowing.

In credit, the combination of persistent inflation and higher rates is going to strain the liquidity position of many companies, as margins shrink and it becomes more expensive to service their debt. Early indication from the reporting season shows there’s cause for worry across industries.

Wrongfooted on Policy

The latest messaging from ECB policymakers suggests they will stay on the course on interest-rate hikes until they see a more meaningful pullback in inflationary pressures. Yet stock investors are optimistic about a soft-landing for the economy and rate cuts later this year.

That dissonance has seen equities move in sync with bonds - where investors are focusing on a recession - and could lead to shares tumbling if the ECB does stay the hawkish course for longer.

Liberum Capital:

“Elevated inflation through 2023 means policymakers will have “little to no room to cut rates even in a recession. If central banks don’t want to repeat the mistakes of the 1970s, they need to wait until inflation is close to 3%, something we do not expect before 2024”.

Recession Woes

Some economists including at Goldman Sachs say the euro zone could avoid a recession altogether this year, citing signs of resilient economic growth and the averting of the energy crisis. Other market participants say it’s too early to call it.

“We expect a sharp loss of growth momentum in response to aggressive monetary tightening, but markets are not priced for this,” said Bank of America strategist Sebastian Raedler. He sees a downside of almost 20% for the Stoxx 600 Index as data start to show slower growth.

Uneven China Recovery

With early optimism about China’s reopening from Covid-related lockdowns now priced in, the path ahead may be rocky. Consumer confidence remains near record lows in the world’s second-biggest economy, the population is shrinking for the first time in six decades and the property market is still in the doldrums.

great take, thank you ... European Stocks & Bonds yields divergence is quite something to be noted ... . Have a great week!