Is market fighting the Fed?

Macro context and equity market have different views...

Last Tuesday we got a decline in CPI, but the “fall momentum” is slowing down.

We have to look at the data in detail to get a meaningful interpretation, in order to try understanding Fed next moves.

What are the areas that will likely improve and what factors could force the Fed to keep being aggressive ?

The overall consumer price index climbed 0.5% in January, the most in three months and bolstered by energy and shelter costs, according to data out Tuesday from the Bureau of Labour Statistics. The measure was up 6.4% from a year earlier. However, a key measure that Powell has highlighted earlier – core services ex shelter – cooled to 0.3% in the month from 0.4% previously. Housing contributed the most to the monthly increase in the CPI, but it is a lagged measure, so it is normal that it will take more time.

In the coming months, there will be a lot of attention paid to the core services component, which refers to the cost of services without including housing costs. In January, there was a slight increase of 0.3%, but it was limited by a decrease in healthcare costs. However, excluding healthcare costs, there was an increase of 0.8%, which could be problematic. And we just got the largest 15-days increase in used car prices since 2009: 4.1% so far this month.

The services category is one whose prices are closely linked to wage increases. Signs of persistence in the strength of the labor market make it increasingly risky to witness wage increases requested to cope with the cost of living increase represented by inflation. It is in this sector that the wage spirals so feared by the Fed and the markets could occur. Recent data on real wages in this category show that in January, they contracted by 0.2%. The annual loss is 1.8%. This increases the risk of wage increase demands that would eventually result in future service price increases.

The greatest risk is concentrated in a series of service categories in which we could see a continuation of the current price increases in a context of strengthening bargaining power of workers. And such power, of course, depends on the strength of the labor market. The current context characterized by minimum unemployment levels and NFP exceeding 500,000 units raises concerns about the risk of wage claims. US wage growth has failed to keep pace with rising consumer prices for a record 22 consecutive months.

That is why, in the wake of CPI data, a chorus of Fed speakers talked about the slow pace of disinflation, suggesting the Fed isn’t yet taking comfort in the inflation trends. NY Fed President Williams (voter) repeated there is "still a ways to go" to control inflation and the current levels of inflation are far too high. Philly Fed’s Patrick Harker (voter) noted that how far above 5% the Fed needs to go depends on incoming data, and Tuesday's inflation report shows inflation is not moving down quickly. Dallas President Logan (voter) stressed that tightening policy too little is the top risk. Thomas Barkin (non-voter) said it was about as expected and there's going to be a lot more inertia and persistence to inflation than the Fed thought. However he was slightly more dovish saying that if inflation settles, they may not go as far on the terminal but he stressed data dependence. Markets are now pricing in a higher terminal rate of 5.26% in July, and one rate cut has also been driven out of this year’s pricing.

Most of the analysts expects Fed to keep hiking also because, as Apollo pointed out:

Financial conditions are easier than when the Fed began to raise rates, with inflation still in the 4% to 6% range and capital markets starting to reopen, boosting consumer spending, hiring, and ultimately inflation. In other words, it looks like more Fed hikes are needed to get inflation all the way back to the Fed’s 2% inflation target.

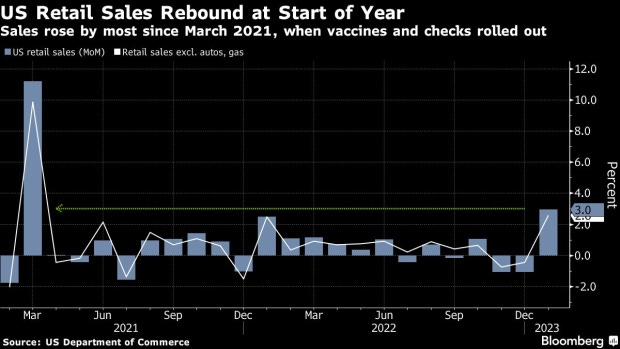

In the meantime, US is showing increasingly fewer signals of a recession, even though classic indicators suggest otherwise. We observed the biggest increase in retail sales since March 2021.

Citi's Andrew Hollenhorst:

"Resilient activity data reduce the probability of recession in 2023, but raise the probability of a more prolonged period of too-high inflation. Scenarios where the Fed leaves rates higher for longer or raises policy rates above our base case terminal rate of 5.25-5.5% are becoming more likely".

Goldman's Jan Hatzius:

"In light of the stronger growth and firmer inflation news, we are adding a 25bp rate hike in June to our Fed forecast, for a peak funds rate of 5.25-5.5%".

Also RenMac rejects the dovish sentiment:

"After 475 basis points of hikes in the federal funds rate, all the Fed has to show for it is the S&P 500 15% off its lows, the unemployment rate at 3.4%, and underlying inflation still running hot… Forget higher for longer, we still need to get higher".

Is US economy is resisting?

Everyone is expecting a recession scenario. However, the opposite is happening. The US economy is holding up and inflation continues to decline, albeit at a slower pace than expected.

As a result, those who had held cash to take advantage of cheaper prices in the event of a sell-off consistent with a recessionary scenario found themselves forced to buy into the stock market driven by FOMO, pushing the stock prices even higher. Initially we saw short positions being closed, followed by purchases by quantitative funds, and then traditional funds that gradually increased their level of investment.

Retail sales data demonstrated the strong resilience of the US economy, with the monthly increase at 3%. Bars and restaurants saw a 7% increase in sales in January. People is spending, keep buying goods and services. Stock indices are rising, the financial conditions of the system are softening, and people have greater monetary dispositions.

Meme stocks are gaining, Crypto are seeing good flows, GDP estimates are raising, US equity is outperforming global peers… market is holding, but fundamental data is not supporting the rally. This is why it seems to be a “Kangaroo market”, in which we can’t observe any strong positive or negative trend.

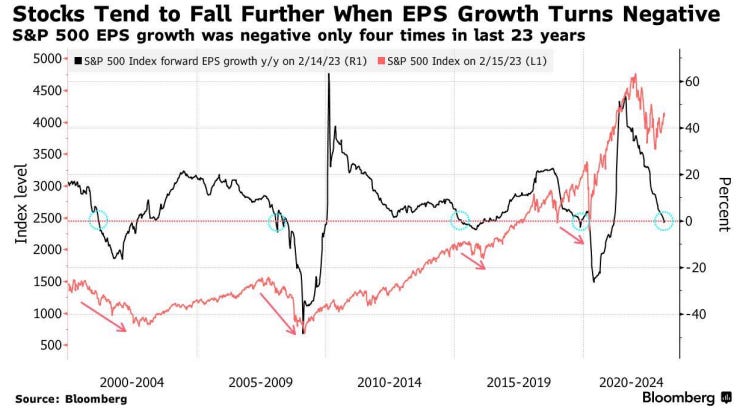

But be careful: we are getting signals of an incoming fall, like the EPS growth turning negative, so be prepared…

great take, thank you!