Market vs Central Banks: Macro round-up of US, EU, Asia

The street has different opinions on the world economy

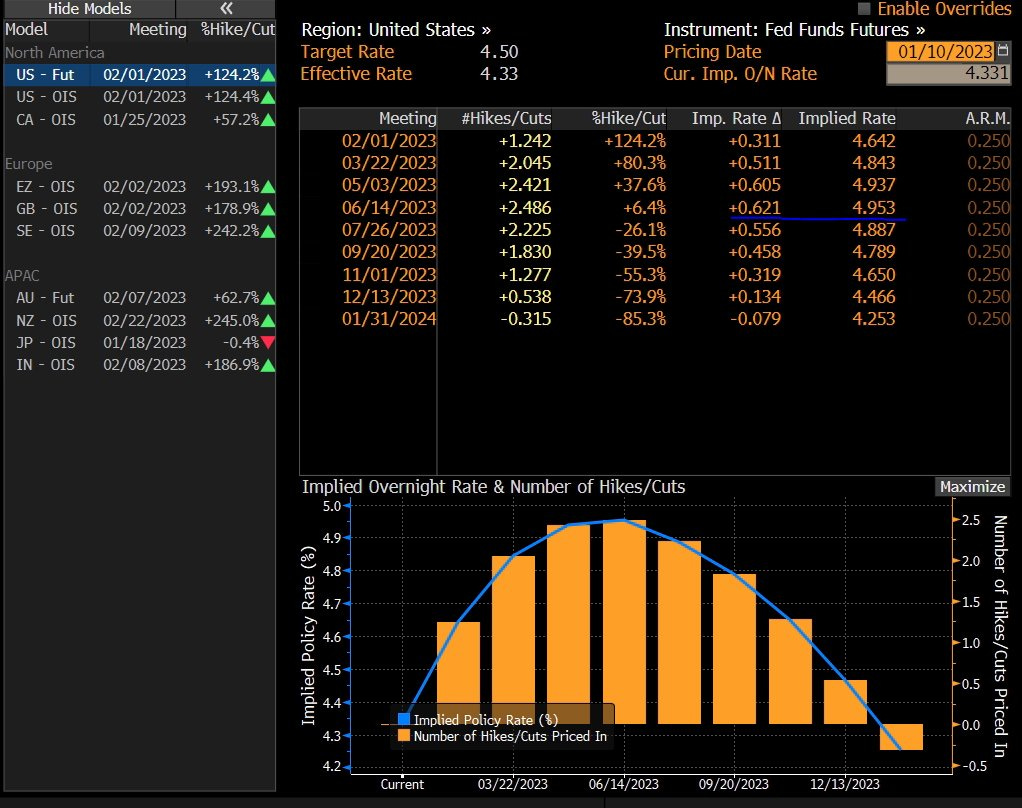

Where will rates go?

Fed says terminal >5%. Markets says <5%. The market is pricing in another step down at the Fed’s next decision on Feb 1 to 25bps rate hike, but the terminal rate pricing still stands at sub-5% levels compared to a unanimous voice from the FOMC members calling for rates over 5%.

The market is really confident three things.

Fed will ONLY hike 25bp in February & signal final 25bp hike March

The Fed will signal lower terminal rate than December dot plot >5%

Fed cuts 2023

The MARKET is FAR too CONFIDENT

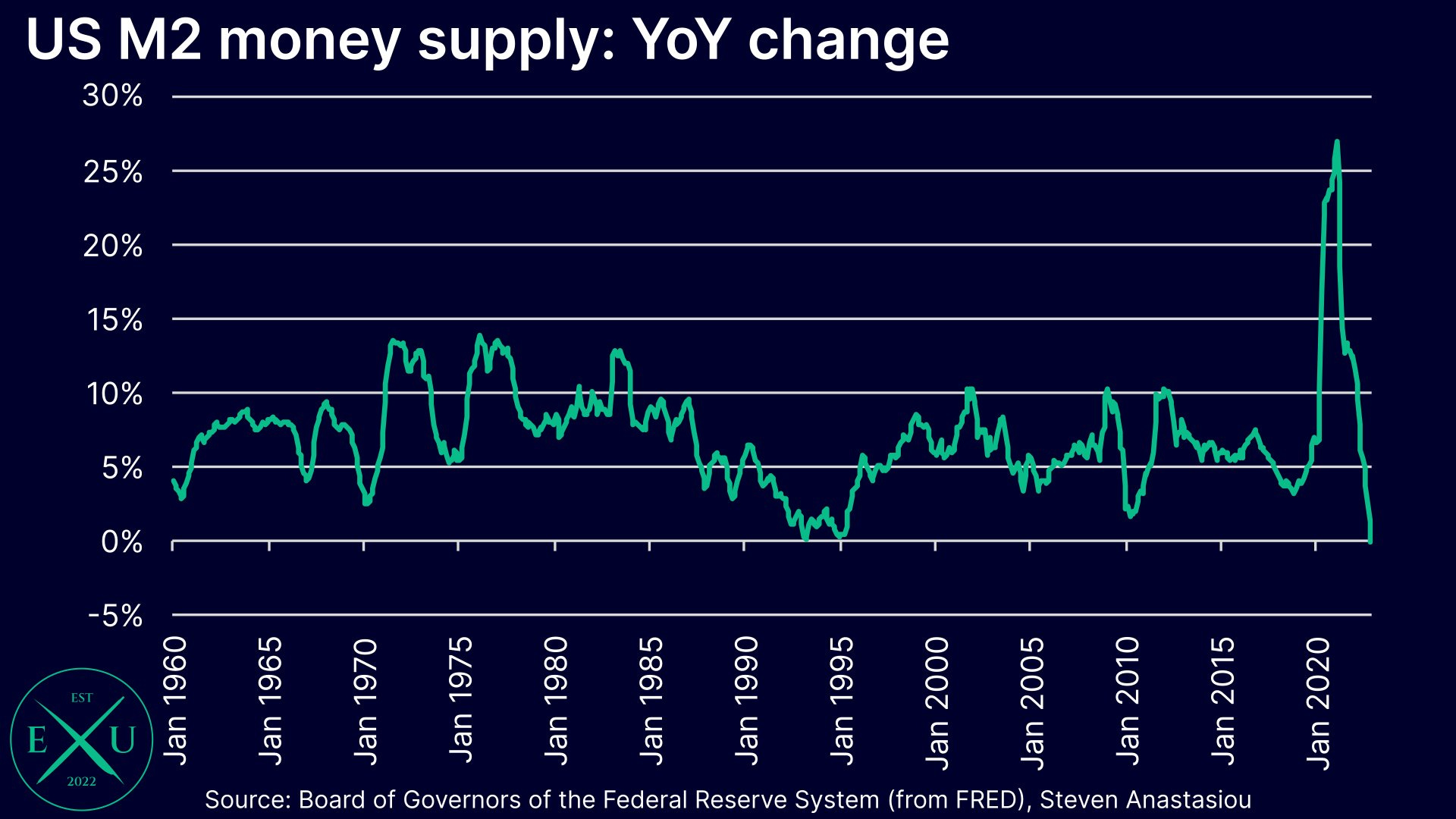

The Fed believes that the money supply isn't a key metric to target or monitor. Yet they also believe that higher rates are needed to fight inflation. But rate rises alter the price, and thus the supply & demand of, money.

M2 shows the Fed is WAY too tight.

What does the street think?

Citi:

"We continue to think Fed concern about loosening financial conditions amidst tightening labour markets imply unappreciated hawkish risk - including of a 50bp hike on February 1. This is even more the case after the dramatic decline in Treasury yields last Friday".

BofA:

"We do not see the Powell Fed as facing a new 'conundrum'... The Fed should worry less about markets pricing cuts in 2023... If the Fed commits itself too strongly to 'no cuts in 2023n, then it risks leaving policy too tight for too long".

JPMorgan CEO Jamie Dimon joined the party, saying there’s 50% chance rates could go to 6%, while money managers BlackRock and Fidelity (among others) warned that markets are underestimating the ultimate rate peak.

Separately, the prominent fixed income manager Jeffrey Gundlach said:

“My forty plus years of experience in finance strongly recommends that investors should listen to what the market says over what the Fed says”.

Macro and Market Context

US CPI came at 6.5% for December, in-line with expectations of 6.5% and lower than last month's 7.1% print. Core CPI came at 5.7%, in-line with the surveyed 5.7% and lower than last month's 6% print.

The World Bank slashed growth forecasts in half, saying new adverse shocks could tip the global economy into a recession. The World Bank cut its global growth forecast to 1.7% this year, halving down the estimate of 3.0% in June. This marks the third weakest pace of global growth in nearly 30 years, overshadowed by only the 2009 and 2020 downturns. Growth estimate for 2024 was also slashed, down to 2.7%, as persistent inflation and high interest rates weigh. Meanwhile, the agency urged for global action to mitigate the risks of a global recession and debt distress.

Real Investment Advise – Lance Roberts: Earnings estimates are finally starting to come down fairly quickly. IF there is a recession, they will need to come down more. However, we are finally moving in the right direction.

IMF chief expects to keep 2023 global growth forecast steady at about 2.7%. IMF Managing Director Kristalina Georgieva said 2023 would be another "tough year" for the global economy, and inflation remained stubborn, but she did not expect another year of successive downgrades like those seen last year, barring unexpected developments. Reuters

Some investors are optimistic about the prognosis for a soft landing. JPMorgan's David Kelly sees inflation continuing to ease, and Ed Yardeni puts the odds of a soft landing at 60%:

"Optimists and pessimists agree that 2022 was a terrible year for stocks and bonds but it doesn't go on forever".

Most investors expect this earnings season to push the S&P 500 down. Still, almost a third of respondents see cooling inflation as a positive driver of S&P 500 Q4 earnings.

Stifel lays a Bullish H1 2023 for stocks:

“There is a window for a strong 1st half 2023 equity rally: Our view is for sharply lower inflation, a 2Q23 Fed rate pause and no official recession […] the combined result of which should be […] 4,300 for the S&P 500 by 2Q23E”.

Companies have rushed to borrow money in the US corporate bond market in the first week of the year, taking advantage of easier financial conditions as investors scale back their expectations for the path of future interest rates. In the first seven days of 2023, companies from Credit Suisse to Ford issued US$ 63.7bn worth of US-marketed debt, according to data from Dealogic, compared to a total of $36.6bn in the last five weeks of 2022. Financial Times

Hedge funds are growing ever more bearish on the dollar, underscoring speculation the Federal Reserve will slow the pace of its interest-rate hikes. Short dollar positions are highest since August 2021.

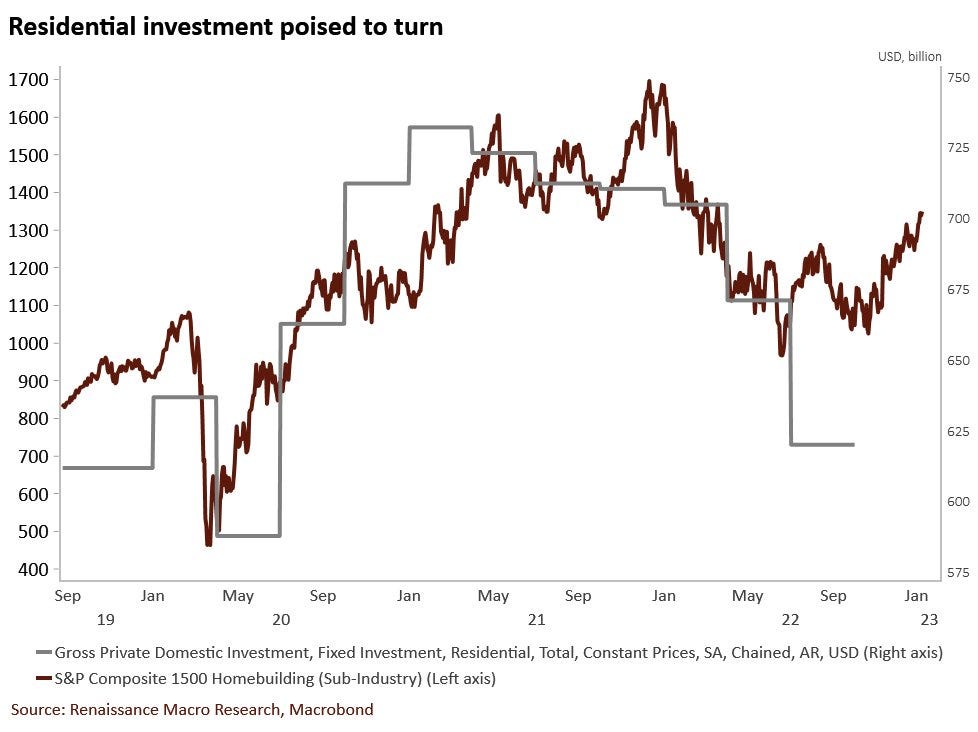

US Homebuilding stocks have been rallying sharply lately. For all the talk about the housing leading the economy, note that stock prices are telling us that residential investment (in GDP) is likely to turn around sometime in H1 2023. Tough for the Fed to break housing twice.

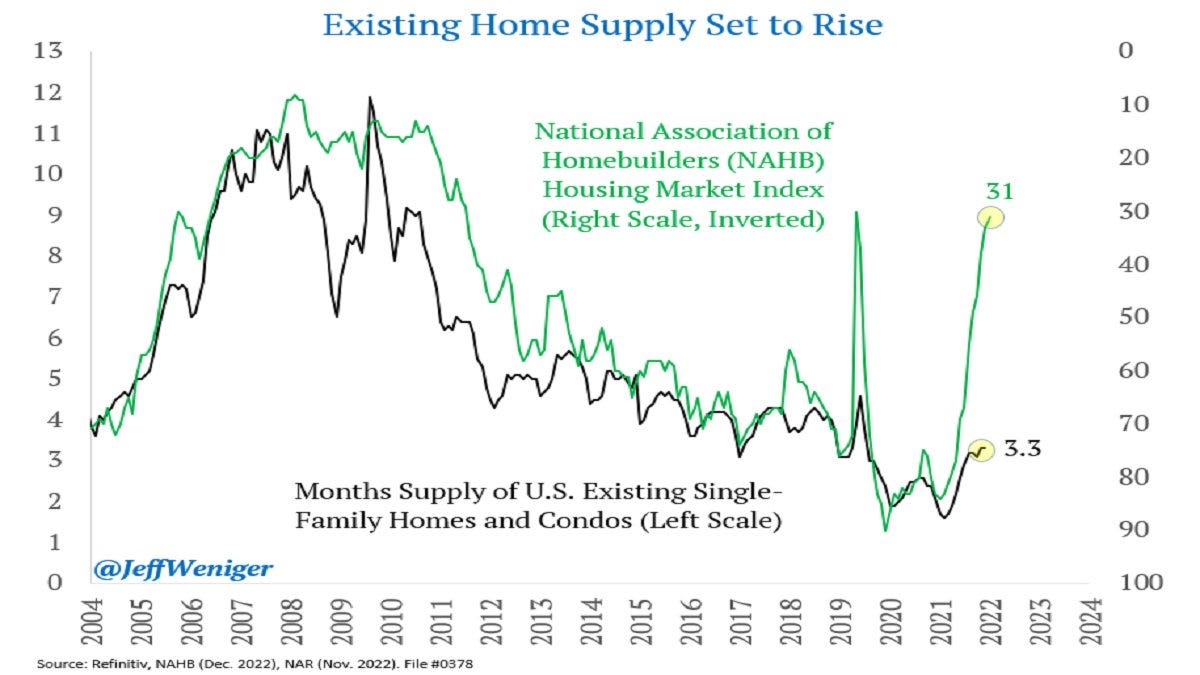

BUT… The National Association of Homebuilders Housing Market Index has collapsed (green line rising). Existing Home Supply of 3.3 months won't last long. So, home supply could rise for the entirety of 2023.

Mortgage activity is down 67% since the end of 2021 and down 81% since the peak in early 2021. Home prices are likely to trend down for a while, which should help reduce Shelter CPI later in 2023 & hopefully improve home affordability.

On Oil

Goldman Sachs: another bullish view from Goldman on oil. The bank expects growing demand - mainly from China - could push the market back into deficit from June, and cause Brent to rally to US$ 105 by Q4. A tighter market would allow OPEC to unwind output cuts made in October. Demand may grow by 2.7 million b/d year on year in 2023, with 1.7 million b/d coming from China.

Bernstein bullish oil. With the US E&Ps continuing to show capital discipline, OPEC is back to being the key driver of the oil price. OPEC has your back and there isn’t a wave of Russian oil to come back as they are already selling almost all of it. If anything Russia is supportive as the sanctions & price caps kick in properly. Demand is trickier because of the macro uncertainty. The good news is that China is getting better no matter what. Bernstein thinks the marginal cost of producing oil will rise to US$ 80 this year.

After a weaker 1Q, Morgan Stanley sees the oil market coming into balance in 2Q and turning tight again in 2H. While MS suspects that not all of the macro-headwinds have fully played out, the medium term “Seven Uncertainties” that they highlighted in late Nov. are mostly turning into tailwinds. This includes China’s re-opening, further recovery in aviation, downside risks to Russian supply, the slowdown in US shale and the end of SPR releases. When demand growth returns, the market will likely find that the supply ceiling is still not far way; this should support Brent in the US$ 100-US $110/bbl range by 2H.

Europe

The European growth outlook is brightening. "Despite severe weakness in the business surveys until very recently, the hard economic data held up surprisingly well in 2022 given the massive terms-of-trade shock resulting from the natural gas crisis. Now, the economy is experiencing two positive shocks, namely the warm winter (which has pushed wholesale natural gas prices below pre-war levels) and the China reopening (which should disproportionately benefit export-oriented economies such as Germany). Consequently, the recent bounce in business expectations in the PMIs may have further to run and the Euro area economy may well avoid a recession after all"

ECB Lane said price pressures in the euro area will remain elevated even if surging energy costs are starting to ease. "This is not conclusive for the overall inflation dynamic. The original energy shock resulting from Russia’s war in Ukraine and pandemic reopening effects will feed into wages 'for the next two or three years'."

Goldman Sachs no longer expect a technical recession in the Euro area, and recently raised their 2023 growth forecast to 0.6% (vs. -0.1% previously). Here the reasons: 1) the region’s activity outlook has improved notably in recent weeks as incoming data has remained resilient; 2) a warmer-than-expected winter and strong energy conservation have weighed significantly on natural gas prices, and led us to recently lower our Summer 2023 TTF price forecast to 100 EUR/MWh (from 180 EUR/MWh previously) and 3) China’s earlier-than-expected reopening should provide a growth boost to the region.

Europe’s inflation anxiety is fading more quickly than prices. Euro-zone inflation remains near a historic high, but consumer expectations about the path for prices have largely receded back to their long-term norm. In Germany, Italy and Spain — three of the currency bloc’s top four economies — anxiety at inflation over the next year is close to or below the average since the euro was introduced in 1999, European Commission data show. Bloomberg

Saxo Bank on EU inflation: this is still a high number. Looking at the main components, energy had (without surprise) the highest annual rate in December at 25.7%, followed by food, alcohol and tobacco (13.8 %), non-energy industrial goods (6.4%) and services (4.4%). What is worrying is that core CPI continues to increase at 5.2 % versus prior 5.0 % and expected 5.1 %. This will push the European Central Bank (ECB) to keep hiking interest rates in the short-term. But the peak in interest rates is getting closer (Mario Centeno) and the eurozone macroeconomic outlook is not that bad actually (if there is a recession underway, it is at the mild end according to the ECB chief Philip Lane).

Economic surprises are improving significantly in the eurozone. The consensus forecasts a drop in GDP of minus 0.1% this year. Based on hard data, this seems excessively conservative. The German economy is especially very resilient. While gas consumption has collapsed by double digits, industry output has remained largely flat. Based on the latest data on industrial production (for the month of November), no recession in German industry in Q4. However, the year 2023 will be challenging in the eurozone: credit stress is on the rise (first time in a decade we start the year with European IG credit yield above the 4 % level), and the market will need to absorb about € 700bn of liquidity due to the ECB quantitative tightening.

The collective hive mind of Wall Street is backing a view that the euro rally is just getting started. With energy prices tumbling and calls for a region-wide recession falling to the wayside, a clear narrative is emerging that the worst of the economic damage is over and European assets are cheap. Deutsche Bank AG and Morgan Stanley strategists say the euro can rally to US$ 1.15, up from the current seven-month high of US$ 1.07. Nomura International Plc is forecasting a rise to US$ 1.10 by the end of the month, while Aegon Asset Management’s Gareth Gettinby is planning to add to his position in the currency.

Asia

China re-opening and has caused a strong breadth thrust in Chinese stocks. 60% of Hang Seng stocks are now above their 200-day moving average.

Asian and EM equities enter bull market (Saxo Bank). The leading MSCI indices tracking these two segments of the global equity market have entered a bull market up 20% since their lows in October fuelled by gains in China and a weaker USD. The market is betting on a shallow recession in some parts of the world, while inflation keeps coming down, and on top of a successful kickstart of the Chinese economy. All three wishes may not be able to be fulfilled simultaneously and our view is that the market is getting too excited about growth too early as a lot of uncertainty persists. The rally has been fast and furious, so it is only natural to expect some profit-taking. There are also some risks to keep a tap on, such as BOJ's hawkish shift and company earnings. But that being said, there is still room for Asian markets to outperform its global peers in 2023.

Morgan Stanley is Bullish on Chinese assets now: “We believe the market is under-appreciating the far-reaching ramifications of reopening and the possibility that a robust cyclical recovery can occur despite lingering structural headwinds."

thank you!