Navigating the Bond Market in 2025: A Year of Transformation and Challenges

Insights on Interest Rate Volatility, Policy Shifts, and Investment Opportunities

The Fed’s hawkish cut

A long and challenging year for the bond market has ended. It is clear to all that we have passed the end of a secular bull market on rates, but we haven't entered another one yet. 2024 has brought heightened volatility in interest rates, and we have seen only short-term trends in play. We expect the 2025 to be as much as volatile as the last one.

Perhaps the most significant development in the very last few months has been the dramatic response in bond yields to the evolving policy landscape. The 10-year Treasury yield has surged approximately 100 bps since the Fed began its easing cycle in September, reaching 4.82% at the end of December and marking its highest level since November 2023. This counterintuitive movement, with longer-term yields rising as policy rates fall, represents more than just a technical correction; it signals a fundamental reassessment of the neutral rate and term premium.

The surge in yields comes at a critical moment as the U.S. Treasury faces a significant “debt wall” in 2025, when $7.6 trillion of outstanding debt will need refinancing. This represents 27% of the total $28 trillion Treasury outstanding market – a substantial portion that has captured market attention. Investors are particularly focused on how the incoming administration might restructure its debt issuance strategy. One widely discussed possibility is a shift away from short-term Treasury bills toward longer-duration bonds. If implemented, this transition could create additional upward pressure on long-term interest rates, with some analysts suggesting the 10-year Treasury yield could approach 5%.

The structural implications of these movements extend beyond mere rate levels. With neutral rates potentially much higher than the previously assumed 2.8%, the entire framework for monetary policy implementation may need recalibration.

The Federal Reserve's decision on December 18th to implement a 25 bps cut, bringing the federal funds rate to 4.25%-4.50%, marked what Chair Powell described as a “closer call” than previous policy adjustments. This hesitation, coupled with a markedly hawkish revision to the dot plot projecting only 50 bps of easing in 2025 (down from 100 bps in September), signals a new phase in the monetary policy cycle where adjustments will likely be more measured and data-dependent.

The Fed's cautious approach reflects multiple concerns: deteriorating inflation dynamics, the potential inflationary impact of the incoming administration's policy mix, and the need to maintain credibility in the face of persistent price pressures. The upward revision to inflation projections, with PCE now expected to reach 2.5% in 2025 (up from 2.1% in September), and the timeline for reaching the 2% target pushed back to 2027, underscores the challenges ahead. The lack of significant revisions to GDP and unemployment projections suggests that policymakers are primarily focused on inflation risks rather than growth concerns.

The draining of liquidity from the reverse repo facility and its shift into longer-duration assets could reduce market leverage precisely when stability is most needed. This dynamic, combined with the substantial Treasury refinancing calendar, creates a challenging environment for both fixed income and equity markets.

It is not surprising that in December, the Federal Reserve has been the scapegoat for the selling pressure on equity and bonds after policymakers delivered a hawkish rate cut earlier this month.

U.S. Manufacturing weakness and Global economic signals

On the other hand, the U.S. manufacturing sector continues to flash warning signals about economic momentum. December's Chicago PMI reading of 36.9 marked the 13th consecutive monthly contraction and the second-lowest reading since 2020. The final S&P manufacturing PMI for December, while better than the flash reading at 49.4, still indicated contraction for the sixth consecutive month. New orders showed particular weakness, with survey respondents noting customer reluctance to commit to new projects ahead of the administration transition.

The global context adds another layer of complexity. Structural weaknesses persist in various major economies: China faces ongoing property sector challenges and years of easing measures, Brazil grapples with economic instability, Europe contends with weak growth and rising populism, and geopolitical tensions continue in the Middle East. While the U.S. has emerged as a relative haven, the risk of global spillover effects cannot be ignored.

Credit Markets and Risk Assets: pretty stretched

The credit markets in 2024 significantly outperformed initial expectations, with European investment grade delivering excess returns of +3% and high yield posting +6%. However, these strong returns mask growing concerns about valuations and fundamentals. High-yield issuers, particularly those with stressed capital structures, are offering increasingly unattractive risk-adjusted returns at current yield-to-worst levels. The B-rated cohort appears especially stretched, with limited cushion against near- and mid-term tail risks.

Sector-specific vulnerabilities have become more pronounced, particularly in areas such as automotive, where declining sales volumes show strong correlations with broader industrial value chains. The persistence of weak operating momentum observed throughout 2024 raises questions about the sustainability of current spread levels, especially for borrowers with cyclical revenue streams and over-levered capital structures.

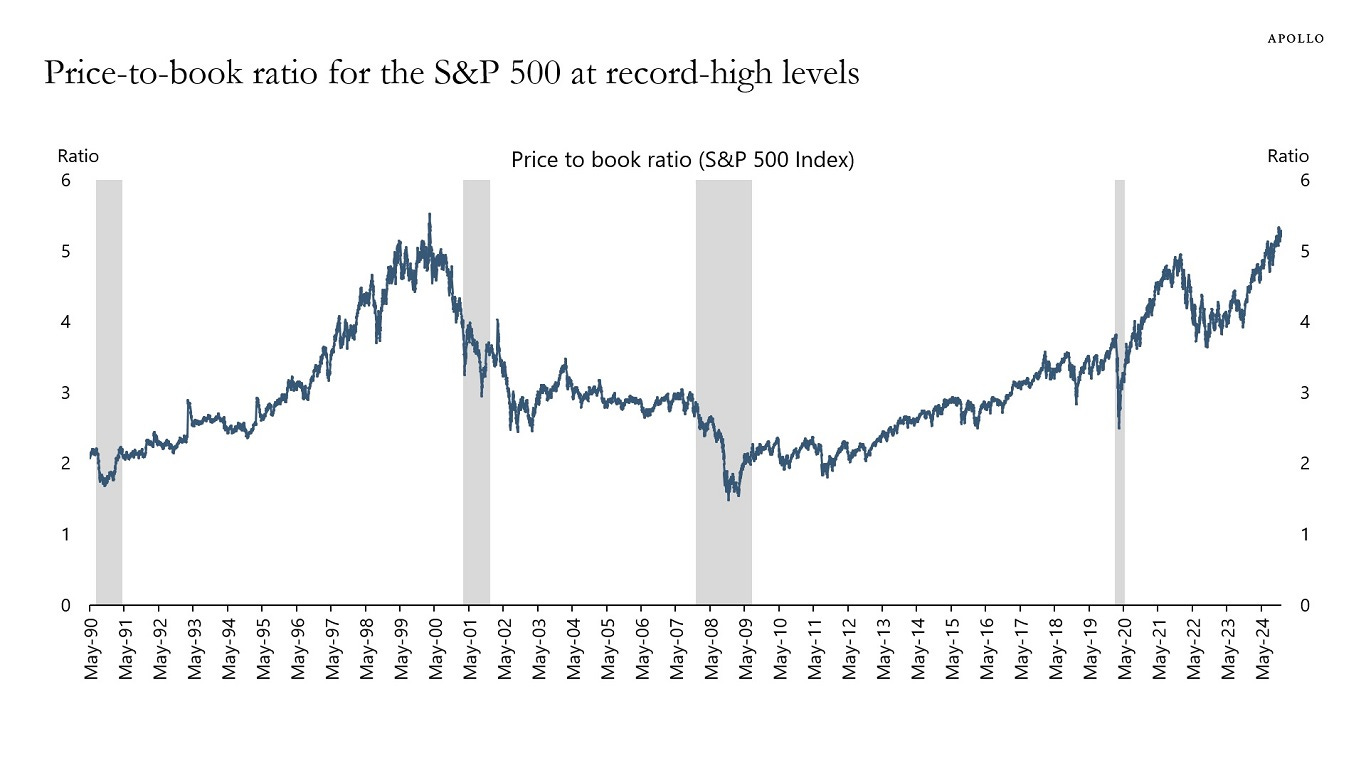

Equity markets have reflected these tensions, with the S&P 500 pulling back from its December 6 record of 6090. Market concentration has reached historic levels, with the top 10 stocks in the S&P 500 now almost 800 times larger than the 75th percentile stock – a concentration exceeding even that of the Great Depression era. Equity valuations are also expensive, with the price-to-book ratio for S&P 500 is at record-high levels.

This narrow market leadership, combined with elevated valuations, suggests increased vulnerability to shifts in sentiment or monetary conditions.

Looking Ahead: 2025 challenges

The investment landscape for 2025 presents a complex set of challenges for investors. Let’s briefly touch what is on our minds.

The spectre of policy uncertainty has put investors on edge, with demand for protection rising across assets (i.e. options hedges).

As we said, investors had to dial back their expectations of rate cuts over the coming year. The latest Federal Reserve forecasts indicating fewer rate cuts than anticipated triggered significant market volatility, including the S&P 500's steepest single-day decline in four months during early December. This sharp reaction tempered the market optimism that had followed the November presidential election results.

The drawdown in bonds now matches some of the historically worse drawdowns for stocks. And investors don't seem to price in an imminent counter-rally. Bond investors are pricing an environment in which a very hawkish Fed won't affect the economy down the road. Basically, Fed Funds around ~4% are priced to be the “new normal” – this used to be 2-2.50% before the pandemic. This paradigm shift raises critical questions about the economy's and housing market's resilience to sustained higher rates.

The Federal Reserve's reaction function remains a key source of uncertainty. The possibility that this cutting cycle might be paused until “something breaks” cannot be dismissed, especially given the robust fiscal support that has buffered the economy through the hiking cycle. Market expectations for the path of policy rates appear increasingly disconnected from the Fed's more cautious outlook, setting the stage for potential volatility as these views reconcile.

Credit markets present an intriguing paradox. Despite spreads across U.S., European, and Asian markets approaching multi-decade lows, some analysts maintain a constructive outlook. They cite factors such as reduced index duration, improving credit quality, and the pull-to-par effect of discounted bonds. However, this optimism must be weighed against historically tight spreads and emerging fundamental weaknesses in certain sectors. In addition, the European context, with structural economic weaknesses and political uncertainty, could potentially limit the scope for organic demand-led growth.

An argument for tighter U.S. bond spreads is that hedging against default risk is near the lowest on record. Fund managers have taken advantage of similar periods of cheapness in the past to build up insurance, but so far there hasn’t been enough buying pressure to increase credit default swap risk premiums. The spread between 2y and 10y Treasury yields highest since May 2022.

On the other hand, while fixed income spreads are tight, we believe a combination of deteriorating fundamentals and weakening technical dynamics would be needed to trigger a more concrete turn in the credit cycle. We still don’t see signs of such dynamic.

In the equity market, while some market participants maintain optimism about potential deregulation and fiscal stimulus under the new administration, the combination of elevated valuations, concentrated market leadership, and potential inflation risks suggests a challenging environment. The dominant market view is that equities will continue climbing a wall of worry, but the obstacles to keep delivering gains will get bigger.

For institutional investors, these conditions necessitate a strategic recalibration. The potential for higher neutral rates could significantly impact both equity and fixed income allocations. We are pretty sure the AI theme will continue to support the current market valuations and we still do not any sign of fatigue.

In conclusion, while we are not bearish, it is prudent to be careful and ready to tactically return to the side-lines. As we enter 2025, we have also to remember that the era of abundant liquidity and predictable central bank support appears to be giving way to a more nuanced and stretched investment environment, where traditional assumptions about market relationships and policy responses may need reassessment. Success in this environment will likely require greater flexibility in asset allocation and a big focus to risk management.

Source: Ashenden Fixed Income Monthly Report

Every month, we publish the Fixed Income Monthly report. The report is a synthesis of the Ashenden’s team view on Fixed Income, pursuing a global approach through the full spectrum of the asset class and providing bond picks. We range from Investment Grade bonds to High Yields & Emerging Markets.

In the report we disclose our bond model portfolio (9 years track record) with more than 60 individual names. We include new single bond ideas, switches, new entries and exits.

All this is corroborated by a bottom-up analysis for each single position (new and old) and merged with a top-down consideration so to include the key market drivers.

This is one of the research piece our team produces internally. The intent of the report is to support wealth managers/asset managers in their decision and allocation process.

Feel free to ask us more information: write to us at research@ashendenfinance.ch