News are shaping the market

Israel war, Treasuries cooled by Fed, market reaction

Keeping an eye on news is a must

Israel - Hamas on the watch

The big theme of recent news is, unfortunately, another war. Israeli Prime Minister Benjamin Netanyahu said his country is at war with Hamas after the militant group’s forces poured across the border from Gaza on Saturday, clashing with Israeli forces and pushing into a swath of territory in the south of the country. Some hawks in Washington and beyond have been quick to label Tehran as the true culprit behind the Hamas attack. Iran, after all, has long financially and militarily aided Hamas. But groups like Hamas do retain a certain level of independence from Tehran, and U.S. officials have yet to cast blame on Iran.

How big is this going to get? (Politico) - From the threat of a regional war to China’s strange diplomacy, there’s no end to the dilemmas ahead.

What’s now a fight between Israel and Hamas has the potential to turn into a wider war, convulsing a region that hosts many rivalries — and many U.S. troops. Hamas may long for its Iranian backers and sympathetic Arab governments to come to its direct aid. Other armed groups, including Lebanon-based Hezbollah, could provide manpower or seize the moment to spur violence elsewhere.

Earlier this year, Chinese officials said they’d be willing to make a run at peace talks between Israelis and Palestinians. This followed a successful Chinese role in the restoration of diplomatic relations between Saudi Arabia and Iran. But China’s reaction to the latest violence may temporarily sour Israelis on Beijing’s advances. In a statement Sunday, the Chinese Foreign Ministry said Israel and Palestine — it used that term instead of Hamas or Palestinians — should “remain calm, exercise restraint and immediately end the hostilities to protect civilians and avoid further deterioration of the situation.” It went on to call for a two-state solution.

For Israelis, this is infuriating. The latest attacks are arguably the worst violence they’ve experienced in 50 years. They come from a heavily armed outfit that took control of a territory after Israel had dismantled settlements there in the hopes of paving the way for long-term peace. Israelis feel they have every right to strike back against Hamas.

On the market, the risk-off move on Monday morning was largely confined to Middle Eastern stocks and crowded currency trades in Mexico and eastern Europe, though, with losses across wider emerging markets more muted.

Main implications: Oil prices

Before Hamas’ attack, Goldman Sachs said the oil sell-off would be transitory.

We believe the selloff in Brent over the past week reflects three main factors, which we think will prove to be transitory.

First, very weak DoE data on gasoline demand and inventories have amplified a sharp selloff in gasoline margins, which has spilled over into crude markets. We see this as overdone because alternative measures of demand implied by ethanol blending and from the DoE (“unadjusted demand”), and physical prices suggest demand remains robust.

Second, Wednesday’s shift in the crude futures curve, and our conversations suggest investors worry again about a rates-driven 2024 recession. GS believes the soft landing remains on track

Third, technical factors—including last Friday’s expiration of the November Brent contract and CTA selling—have likely contributed to the decline in prompt Brent futures contract.

Now, Crude prices surged to as high as US$ 89 a barrel over concerns that Hamas’s attack on Israel will increase tension across the Middle East and affect output from leading oil producers. Brent, the international oil benchmark, jumped as much as 5.2 per cent in early trading in Asia, before steadying to trade 3.8 per cent higher at US$ 87.83. WTI, its US counterpart, rose 4 per cent to US$ 86.07. FT

Analysts are looking at the effects of the war.

BNP: Limited impact from conflict but price risks skewed upwards

We believe recent developments in the Middle East add a risk premium to crude prices, given risks of escalation and tighter enforcement of Iranian sanctions. However, we consider the impact to remain limited unless there is a significant escalation. Key signposts in this respect would be the narrative on Iran’s involvement; tightening of sanctions enforcement on Iranian flows; and escalation of hostilities to neighbouring regions.

Goldman Sachs: Early Thoughts on Potential Oil Market Effects from Attacks in Israel

Recognizing the elevated uncertainty and incomplete information at this early stage, we note that there has been no impact to current global oil production, and that we see as unlikely any immediate large effect on the near-term supply-demand balance and near-term oil inventories, which tend to be the main fundamental driver of oil prices. We thus continue to forecast that the Brent oil price rises from US$ 85/bbl as of Friday to US$ 100/bbl by June 2024. That said, we identify two potential implications of Saturday’s shocking attacks that may weigh on global oil supply over time.

Reduced probability of Saudi-Israeli normalization and associated boost to Saudi production.

Downside risks to Iranian oil production

UBS: Conflict fears push up oil prices

Hamas’ attacks in Israel weakened the shekel and increased oil prices. The Bank of Israel pledged to intervene in the foreign exchange markets and provide dollar liquidity to domestic banks. There is little sign of a broad safe-haven bid for the dollar, at this stage. Investors’ concerns about an escalation of the conflict to include Iran have prompted oil price moves.

Citi:

The attacks almost certainly postpone any Saudi/Israeli rapprochement, along with any high probability expectation of Saudi Arabia reducing or eliminating its extra 1mln BPD cut if prices resume their recent fall. Risks also grow for an Israeli attack on Iran, given its support and encouragement to Hamas, with timing an open question. Meanwhile, any expansion of battles will have potential repercussions on oil markets. US is likely to be significantly less permissive and encouraging of additional Iranian exports, and might take actions to more rigorously impose sanctions impeding Iranian exports and access to frozen assets going forward.

TD Securities, Cowen:

Terrorist attacks and resulting combat have created risk other regional actors could become involved and/or ISR could retaliate against other parties. We think several next steps will be important to gauging the trajectory of fighting and/or cessation. We do not expect combat to end quickly and believe the risk will be elevated that fighting could spread.

RBC:

The US-led effort to secure a sweeping diplomatic reset with Saudi Arabia appears to be in a very precarious place following yesterday’s deadly events… Iran remains a very big wild card and we will be watching how strongly Prime Minister Netanyahu blames Tehran for facilitating these attacks by providing Hamas with weapons and logistical support. In addition, we anticipate that Israel will escalate its long-running shadow war against Iran; which has entailed assassinations of nuclear scientists and military commanders, mysterious explosions at key nuclear and weapons facilities, and cyber-attacks on critical infrastructure sites.

FED officials went dovish

Vice-Chair Jefferson (voter) said the Fed needs to move carefully to balance risks of tightening too much or too little and it may be too soon to say confidently that they have tightened enough. Furthermore, he said the Fed can 'proceed carefully' amid better risk balance and will keep in mind the tightening impact of higher yields.

Logan (voter), who usually leans hawkish, acknowledged that if higher long-term rates are due to higher term premiums, there may be less need for the Fed to raise rates. However, she warned that to the extent a stronger economy is behind a rise in long-term rates, the Fed may need to do more. Logan added that when it comes to setting the policy rate, the Fed must take account of financial conditions, which have tightened substantially in recent months, adding that higher term premiums have a clear role in higher long-term rates, but it is uncertain how big that role is.

Effects on the market

Treasuries

“The latest comments from Fed speakers have had a clear risk-on influence on the market,” said Benjamin Melman, global chief investment officer at Edmond de Rothschild Asset Management. “There’s been a clear change of tone.”

Treasuries’ had best day since March driven by signs Fed may be done. US 10-year yields slid the most since March after dovish comments from Federal Reserve officials fuelled speculation interest-rate hikes are about done, while jitters over the Israel-Hamas war added haven demand. The move was more pronounced than normal as trading of cash Treasuries had been shut worldwide Monday for a US holiday. US 10-year yields fell as much as 185bps to 4.62%, the biggest one-day decline since March 22.

Yields on BBB corporate bonds now exceed the expected earnings yield of the S&P 500 for the first time since 2009. According to Citi, for pension funds "targeting on average around 7-8% annual returns" these higher corporate bond yields "offer a less risky way" of hitting the target vs stocks.

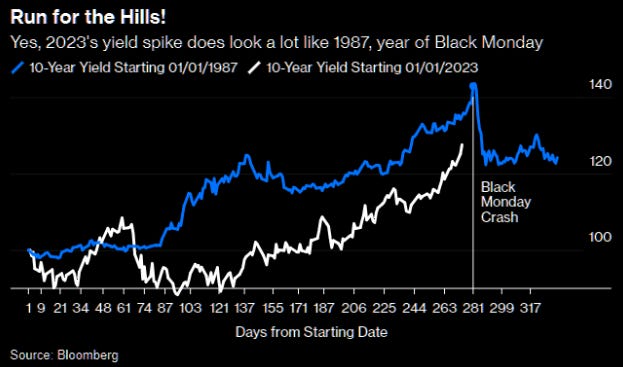

This while just a couple of days ago, we were witnessing closely resembles that of 1987 shortly before the Black Monday stock market crash.

But some analysts were already pointing out the slide in Treasuries was excessive given recent economic data and Fed policy, suggesting it was instead being driven by fears over the swelling US deficit.

”Treasuries are detached from their fundamental drivers”, JPMorgan said.

”The escalating budget deficit will create more supply of bonds than demand can meet”, Yardeni Research's Ed Yardeni said.

Another “good” sign: Fed Balance sheet dropped <US$ 8tn for 1st time since Summer 2021 on QT. Fed's total assets are now equal to 29.4% of US's GDP vs ECB's 50.9%, SNB's 111.5%, or BoJ's 125.7%.

Now, Treasuries rally may peter out unless US and global growth slows down, UBS said. Yields may not fall significantly further from here, with price action in gold and oil suggesting the market views the Israel conflict as contained, according to TD Securities.

Solita Marcelli, chief investment officer Americas at UBS Global Wealth Management:

Against this backdrop, we continue to prefer fixed income to equities. We see a better risk-reward profile for fixed income, and we recommend investors consider buying high-quality bonds in the five- to 10-year maturity range. We foresee further cooling in inflation and slower global growth.

For Bill Gross, the bond market is a “little oversold”: he says stocks are “clearly overvalued” and that bond yields would need to fall “significantly” to justify current valuations. In an investment outlook published last Wednesday, Gross said neither bonds nor equities are attractive, even after the recent selloffs, because inflation leaves little room for the Federal Reserve to lower rates from a 22-year high.

Food for thought: these comments came after Treasuries yields reached alarming high level: at those yields, the financial conditions would been sufficiently high. But if yields come down, we would be back at the starting point.

Equity

European shares rallied after dovish comments by Federal Reserve officials and the prospect of more economic stimulus by China brought some risk appetite back to markets as investors continue to evaluate the potential impact of the Israel-Hamas conflict. The Stoxx Europe 600 index climbed 1.5%, heading for its best day in a month, with all industry sectors in the green.

The S&P 500 approached 4,400, with some analysts citing a rebound from oversold levels.

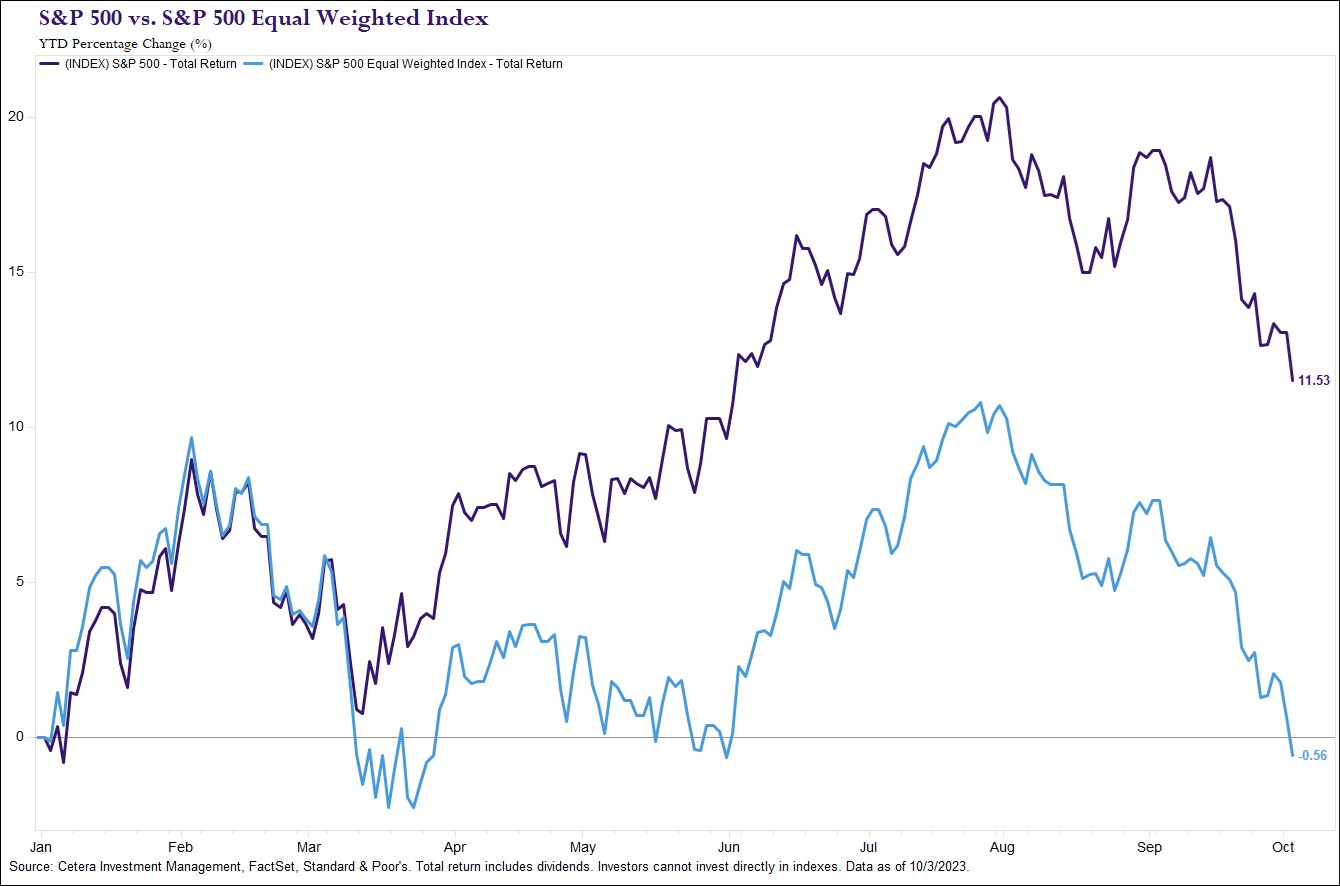

Despite recent weakness, the S&P 500 has a YTD total return of 11.5%. It’s a different story for the equal weight S&P 500 index, which is -0.56% YTD. Most of this year’s returns are driven by the 10 largest stocks in the S&P 500.

The S&P 500 is still 'buy the dip' for the next six months. That's the view of Manish Kabra, head U.S. equity and multiasset strategist at Societe Generale. "We expect the profit cycle to improve in the next six months and cyclical data such as the ISM to rise to 55 before the consumer-spending downturn leads to a selloff in U.S. stocks," said Kabra. Corporate profit expectations are behind much of that forecast for stocks. "We expect profit growth to accelerate over the next two quarters, hence our S&P 500 SPX target range of 4,050 to 4,750. A mild recession in the middle of 2024 should lead to a higher risk premium, riving the S&P 500 back to 3,800," he said. MarketWatch

But Goldman Sachs Michael Wilson sees another risk for US stocks: fiscal policy constraints at a time when the Fed is still fighting high inflation. The strategist — among the most prominent bearish voices on Wall Street — said while the US government narrowly avoided a shutdown last week, “the lack of a resilient long-term structure that supports fiscal discipline” could have an impact on financial markets.