Now Deutsche shakes the markets

Deutsche Bank CDS are rising

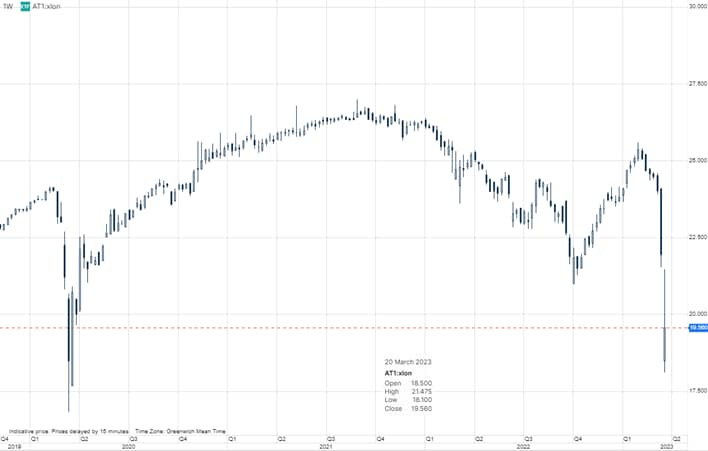

AT1 bond yields surpass return on equity (Saxo)

European banks were down 5% on Monday morning trading with Deutsche Bank that lead the declines following a big jump in its 5-year CDS price. Not even redeeming a tier 2 bond despite fears of calling the bond calmed the market. Other bank stocks also fell Friday, albeit by less: Barclays and BNP Paribas were down roughly 4% and 5%, respectively. Deutsche Bank offered to redeem a junior bond Friday at face value in an apparent effort to bolster confidence.

Also adding to the negative sentiment is the Deutsche Pfandbriefbank AG deciding not to call one of its AT1 bonds citing financial conditions and costs: the coupon resets from 5.75% to 8.45% which 270 basis points increase in the funding costs on that part of the tier 1 capital structure. The AT1 bond market was already weak post SVB, but the shotgun wedding between UBS and Credit Suisse wiping out the AT1 capital holders. AT1 bonds are down 22.7% from the peak in early February.

Putting it all together funding costs for banks are on the rise and thus interest rates into the economy will go up which in turn will tighten credit conditions and increase the likelihood of a recession. As soon as this logical chain is understood by the equity market it will stop treating falling yields as a panacea but as a sign of bad times ahead.

Deutsche case

Thanks to an investor update on Monday afternoon, Deutsche Bank shares rebounded and the cost of insuring its debt against default eased after sell-side analysts reassured that the German lender’s financial health was sound. As summarized by Unicredit, the slides include an updated LCR ratio as of 23 March 2023 of 137% (down from 142% as of 31 Dec 2022) but still well above the 130% internal target and 100% min requirement. The slides also contain more info on the deposit base. 71% of deposits are from German home market. 16% of deposits are term deposits with 8 months weighted maturity and 40% are retail deposits (thereof 76% are deposits below 100k so more sticky). Corporate deposits are with 28% high, but thereof 16pp are operational corporate deposits and only 12pp is non-operational corporate overnight which can be more volatile.

On their deposit base: "76% of German retail deposits insured via statutory protection schemes; 33% of total deposit base insured. 87% from retail, SME, corporate & sovereign clients; only 2% from Treasury-sourced unsecured wholesale funding".

“Deutsche Bank is not the ‘weak link’ in the European banking landscape,” Kepler Cheuvreux analyst Nicolas Payen wrote in a note, flagging that the lender had “very solid” fundamentals.

“Deutsche Bank has de-risked and refocused its business model in recent years which should help the bank to generate less volatile and higher profit levels,” Oddo BHF analyst Roland Pfaender said in a note Monday, after reiterating an outperform rating.

Deutsche Bank resembles neither Credit Suisse nor Silicon Valley Bank. According to Moody’s, Europe’s top banks are unlikely to face the kind of downward spiral as Credit Suisse. None of the region’s 11 remaining mega-banks, which include Deutsche Bank, show the “credit profile weaknesses that led to investor and depositor loss of confidence” in Credit Suisse which built up over almost two years, Moody’s said in a report on last Wednesday.

“Those banks that started deep and costly restructuring exercises have largely completed the process”

WSJ: Deutsche seems to be in a good shape: net profit equivalent to US$ 6.1bn last year was the highest since 2007, and contrasts with almost US$ 8bn in net losses at Credit Suisse. Deutsche Bank is benefiting from rising interest rates, just as it long struggled with negative rates. Net interest income (the gap between the money it makes on lending and the cost of paying depositors) rose 39% last year in its bread-and-butter corporate lending division. Capital and liquidity ratios were solid at the year-end.

Recently, also JPMorgan published a report on Deutsche bank, stating that it has solid fundamentals.

DBK ‘s recent CDS widening is in our view related to one way trades of de-risking across all market participants and we don’t see this and the associated share price decline as a reflection of the fundamentals of the bank.

JPM highlights Deutsche’s strong capital ratios (13.4% CET1 ratio) with limited litigation concerns, strong liquidity ratios (142% LCR) with limited deposit outflows in 2015-18 even at times of stress and most importantly strong profitability of the Group at € 5bn Net profit in 2022 compared to losses in the past.

Liquidity surplus of € 64bn above LCR requirements

Loan to deposit ratio of the Group is 79% at YE 2022 with liquidity reserves accounting for 25% of net balance sheet

2023 issuance plan of €13-18bn (around 13% of capital markets issuance outstanding)

Total CRE exposure at YE 2022 was € 48bn of which € 33bn was non-recourse and a focus portfolio for DBK

Significantly higher earnings generation in 2022 compared to in the past

All 4 core division profitable on a stated basis in 2022

Capital ratios well above requirements

Worried creditors raise Deutsche Bank’s funding costs and make investment-banking counterparties more reluctant to deal with it. It is a different dynamic than the vicious spiral of asset outflows at Credit Suisse, but it is still perilous for the German company.

But Deutsche Bank isn’t completely healthy either. A cost to income ratio of 75% in 2022, while better than the 85% achieved in 2021, was above the European average: In the third quarter of last year, big lenders tracked by the European Central Bank had a ratio of roughly 61%. Deutsche Bank’s “core” business looks stronger, but its overall numbers are dragged down by its “capital release unit”—the bad bank it created in 2019 to wind down unwanted assets. Its leverage as measured by total assets against equity is also still on the high side.

These weaknesses, even as Deutsche Bank has emerged from its crisis days, have contributed to a persistent share-price discount. After Friday’s moves, the stock trades for just 32% of its tangible book value, compared with 45% and 62% for Barclays and BNP Paribas, respectively. In a sector where a nervous market can turn a low valuation into a self-fulfilling prophecy, Deutsche Bank’s old problems are coming back to haunt it.

The company these days may not have much to fear but fear itself, but in banking that can be everything.

thank you for the coverage, have a great week!