On the brink of Goldilocks: resilient growth, rising yields and policy puzzles

A look at the challenges for a strong economy with elevated bond yields, with also uncertainty due incoming US elections

Dancing on the edge of Goldilocks

Global government bonds have undergone a dramatic sell-off over the past six weeks, with U.S. Treasury yields rising sharply across maturities. Since hitting a low in mid-September, the 2-year yield has increased by nearly 50 basis points, while the 5- and 10-year yields have surged approximately 65 basis points, reaching 4.15% and 4.3%, respectively. These dramatic movements reflect a string of stronger-than-expected U.S. economic releases, including a robust payrolls report and unexpectedly strong retail sales and inflation data.

The swing in market pricing over the last weeks underscores the difficulty investors still have in interpreting the Federal Reserve's reaction function. The sharp rise in yields, traditionally a critical pressure point for rate-sensitive sectors, has intensified uncertainty around the Fed's future rate cuts. Higher yields typically diminish investor appetite for risk, making equities, especially those reliant on financing like real estate, more vulnerable.

Middle East risk and U.S. election uncertainty are amplifying concerns about inflation and fiscal sustainability. Moreover, neither U.S. presidential candidate is willing to address U.S. deficits, and Donald Trump’s recent polling momentum raises the prospect of potentially inflationary tariffs policies. We have seen these risks getting priced into the breakeven inflation levels and gold, for example.

The long-anticipated soft landing scenario is now confronting mounting challenges. The U.S. economy continues to display remarkable resilience, with third-quarter GDP growth tracking at 3.4% according to the Atlanta Fed's GDPNow model. This robust performance, coupled with upside surprises in payrolls, retail sales, and inflation data, has compelled market participants to substantially recalibrate their expectations. The labor market remains particularly strong, with recent jobless claims coming in below consensus, though hurricane-impacted states have introduced some data volatility. This economic vitality, while impressive, has begun to generate its own set of challenges, particularly in the fixed income markets where yields have surged across the curve.

The International Monetary Fund's recent upgrade of U.S. 2025 growth forecasts to 2.2% further validates the economy's resilience, positioning it one of the few economies to receive such an upward revision. However, this strength presents a nuanced dilemma for the Fed, as it becomes increasingly challenging to justify continued monetary easing in the face of persistent economic vigor.

We find it hard to imagine the Fed next year mechanically delivering rate cut after rate cut against a backdrop of sustained GDP growth and persistent inflationary pressures. We believe an economic deceleration remains in the cards for next year.

Market focus has shifted notably from September's carry-trade emphasis to optimism about Chinese market support measures, and now increasingly toward U.S. election implications and next Fed action.

The Bond Vigilantes’ return: a market rebellion

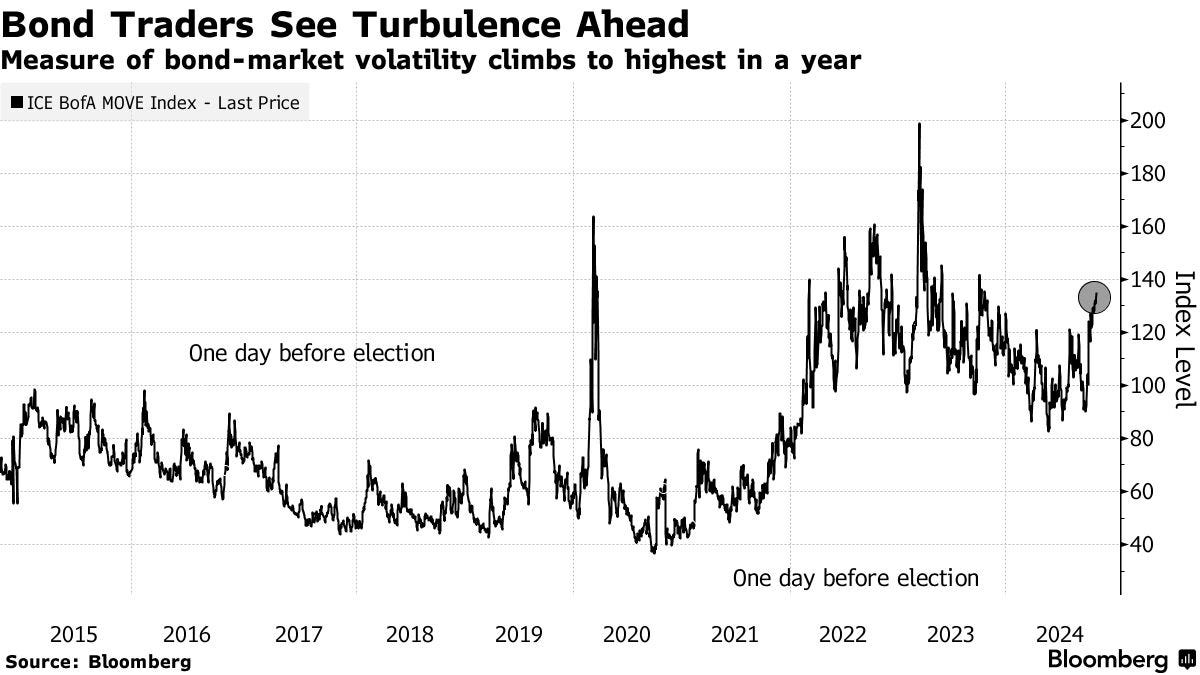

The resurgence of bond vigilantes has emerged as one of the most significant market developments of 2024. Marking a pivotal shift in market dynamics, the bond market has started to vote early, sending a clear message ahead of the November 5 US presidential and congressional elections.

The easing of trajectory of monetary policy stands in contrast to the sharp backing up of markets rates. As we said, since mid-September, the bond market has experienced a dramatic sell-off, with the yields climbing to the levels of late July. This sharp movement reflects growing concern about both fiscal and monetary policy. Recent data showed that UST 10-year yields are at their highest divergence compared to what macro conditions would suggest, signaling that current yields may be overextended relative to fundamentals. Moreover, Treasury securities appear to have transitioned from a recession hedge to a barometer of inflationary expectations, USTs seems no longer serving as a hedge against recession risks, but rather are reflecting inflationary concerns.

The federal government's fiscal position has become particularly precarious, spending $6.75 trillion while collecting only $4.92 trillion in revenues, resulting in a $1.83 trillion deficit – representing 27% of all government spending. This unprecedented fiscal imbalance during a period of economic expansion raises critical questions about long-term fiscal sustainability and potential vulnerabilities during economic downturns.

The bond vigilantes appear to be voting against what they perceive as an overly dovish Fed stance, particularly following the September rate cut. Their collective market signal suggests a deep skepticism about current monetary policy calibration. Their concern stems from the perception that the economy is already running hot and further easing could lead to overheating. This is amplified by the approaching U.S. presidential election, where both major candidates' economic platforms suggest continued fiscal expansion. The term premium on Treasury securities has risen significantly, indicating investors' growing unease about government debt levels and inflation risks. This development echoes historical market behaviors, reminiscent of periods when investors consistently demanded 1-3% premiums for longer-dated maturities in the 1990s and 2000s.

Prominent investors like Paul Tudor Jones and Stanley Druckenmiller have voiced concerns about the potential inflationary impact of a Republican sweep in the upcoming election, particularly given Donald Trump's proposed policies that could significantly increase federal deficits. Their warnings underscore a broader market apprehension about potential fiscal trajectories. The Committee for a Responsible Federal Budget estimates an increase in federal government debt of $7.75 trillion over 10 years under the proposed plans.

However, it's worth noting that any dramatic policy shifts would likely face resistance from both Democrats and Republicans, potentially moderating the most aggressive fiscal expansion scenarios. This institutional check provides a potential counterbalance to extreme fiscal measures. Further we also have to consider that the next administration will face net interest outlays of over $1 trillion on the ballooning federal debt.

U.S. election around the corner

The market seems to be betting on the election’s outcome. Given the deep national divisions, regardless of who wins, we could see riots, looting, or more violent protests weighing on market sentiment.

As JP Morgan penned in a recent note: “As odds of a Trump presidency and Red Wave have increased over the past few weeks, we’ve seen themes that are perceived to be Republican Winners (JPREPWIN) outperform Democratic Winners (JPDEMWIN) by ~7% over the past month. Crypto stocks and small caps have performed better, while Renewables have underperformed. In addition, the wider US equity market continues to make new ATHs and positioning appears to be elevated. Based on the thematic shifts, historical returns around elections, and elevated positioning, there’s room for a bit of disappointment and reversal in coming weeks if odds start to shift the other way.“

While, Harris’ plans are not as deficit-inducing because she wants to increase some taxes on the rich and corporations. Trump’s plan really makes him the “King of Debt.” And that’s a big reason people are talking about soaring yields, soaring Bitcoin and soaring gold prices as Trump trades.

Credit overview: the duration risk come back

Credit markets have shown remarkable resilience despite the challenging interest rate environment, particularly in Europe. The European High Yield market has maintained strong issuance volumes, weathering both geopolitical tensions and rate volatility. This strength is underpinned by robust technical factors, including consistent inflows into Investment Grade and High Yield funds, alongside sustained demand from ETFs and CLOs.

Investors have adapted to geopolitical risks by increasing allocations to traditional safe-haven assets, notably gold, which has diverged from its historical correlation with interest rates over the past two years. European credit markets have effectively navigated ongoing conflicts, including the Russia-Ukraine war and Middle East tensions, which markets increasingly view as temporary disruptions with limited impact on broader equity performance and credit fundamentals.

The high-yield market continues to attract diverse issuers across the rating spectrum (CCC to BB+) and sectors, from restructured retail to sustainable infrastructure. However, recent debut issuances show aggressive pricing, suggesting a potential mispricing of 40-50 basis points, as investors appear to prioritize portfolio diversification over fundamental conviction.

We observe a degree of complacency towards weak credit metrics in some cases, with the allure of 10% yields potentially overshadowing fundamental concerns. The number of troubled credit names in Europe has remained steady in recent months, although investors must remain vigilant for potential deterioration in credit quality as economic uncertainties persist. This environment, coupled with the approaching U.S. election and ongoing geopolitical tensions, demands rigorous credit selection, especially given Investment Grade corporate bond spreads at their tightest levels in nearly two decades.

Our concerns regarding to an unexpected correction that could temporarily impair portfolios have raised. Most notably, investor sentiment is once again very “greedy”, with both retail and institutional investors piling into equities this year despite rising levels of uncertainty. The timing of the next FOMC meeting, scheduled after the election, adds another layer of risk should the Fed signal fewer rate cuts than markets anticipate.

Interest rates continued to back up but on ideas that regardless of the election outcome, the supply of US Treasuries was seen increasing (larger deficits and more debt) and boosting inflation. However, economic data broadly aligns with Fed projections, suggesting a high probability of a rate cut at the November 7 meeting.

Regarding duration positioning, developments confirm our thesis: interest rate markets had been pricing too aggressively for cuts from the Fed. The duration trade has ended in September, and currently, investors with portfolio durations above 5 years are feeling the pinch.

Looking ahead, the interaction between rate markets and credit spreads will be crucial, as a move back to 4.5% in the 5-year Treasury yield could potentially trigger a disorderly exit from corporate credit positions. But we see this window as a good one to moderately add some duration.

We maintain our conviction at the low end of the duration ranges, at around 3.5 years – or about half the duration of the major investment grade benchmarks. Moreover, with investment grade corporate bond spreads as tight as they have been for almost 20 years, we remain cautious on corporate credit.

For investors who need exposure, we continue to recommend a combination of Investment Grade bonds with moderate duration providing quality and specific High Yield and Crossover names, where spreads still offer a thicker cushion.

Source: Ashenden Fixed Income Monthly Report

Every month, we publish the Fixed Income Monthly report. The report is a synthesis of the Ashenden’s team view on Fixed Income, pursuing a global approach through the full spectrum of the asset class and providing bond picks. We range from Investment Grade bonds to High Yields & Emerging Markets.

In the report we disclose our bond model portfolio (6 years track record) with more than 60 individual names. We include new single bond ideas, switches, new entries and exits.

All this is corroborated by a bottom-up analysis for each single position (new and old) and merged with a top-down consideration so to include the key market drivers.

This is one of the research piece our team produces internally. The intent of the report is to support wealth managers/asset managers in their decision and allocation process.

Feel free to ask us more information: write to us at research@ashendenfinance.ch