Recap of the market topics

Earnings, China, Red Sea, new US equities high, there are the big themes now

Earnings season

Investors are monitoring growth trends in AI to understand if it is worth to pay high multiples (not only for the Magnificent 7).

Tech’s fourth quarter earnings season started this week with results from Netflix, Tesla and Intel. The so-called Magnificent Seven are expected to deliver combined profit growth of about 46%, according to data compiled by Bloomberg Intelligence. That’s down slightly from the third quarter’s 53% expansion, but it still dwarfs almost all of the main sectors in the S&P 500 Index.

Netflix reported record revenues US$ 8.8bn in Q4 2023, up 12.5% YoY. This was the highest growth rate since Q4 2021. Netflix reported an incredible 13.1m new subscribers this quarter, crushing the 8.9m estimate. That makes Q4 of 2023 the second-best quarter for customer additions in the company's history. Stock was up 9% in after-hours trading to a new 52-week high. Netflix has signed a 10-year deal valued at more than US$ 5bn to become the new home of hit wrestling show “WWE Raw” starting in January 2025.

Considering how important these companies are to the overall stock market — they accounted for virtually all of last year’s 24% advance and drove the S&P 500 to an all-time high on Friday — earnings season doesn’t quite get going until they show up with their results.

Anthony Saglimbene, chief market strategist at Ameriprise Financial:

“The dominant growth in the market is coming from Big Tech. If they disappoint, that’s a real risk to the overall market”.

China’s rescue package

China is considering a CNY 2tn (US$ 278bn) package to stabilize the stock market mainly through the Hong Kong exchange link, after earlier attempts to restore investor confidence fell short and prompted Premier Li Qiang to call for “forceful” steps. They have also earmarked at least 300 billion yuan of local funds to invest in onshore shares through China Securities Finance or Central Huijin Investment.

BNY Mellon said the plan may not be enough. Vey-Sern Ling, managing director at UBP:

“A rescue package may be insufficient on its own to prop up the market in terms of value injected, but will certainly help dispel the idea that the government doesn’t care”.

Marvin Chen, a strategist at Bloomberg Intelligence:

“The potential support package should be able to stem declines in the short term and stabilize markets into the Lunar New Year, but state buying alone has historically had limited success in turning around market sentiment if not followed up by further measures”.

Onshore Chinese shares pared an earlier rally to end just 0.4% higher. A gauge of Chinese stocks listed in Hong Kong rose 2.8%, easing from an intra-day gain of 4.1%.

However, China’s stock-market rescue package should help boost sentiment in the short term, market participants say, though they question how easy it will be to implement. The moves come as Chinese and Hong Kong shares continue to drop, with the CSI 300 Index off more than 6% year-to-date. Snowball derivatives, which trigger losses below certain levels on some indexes, may also be playing a role. First market reaction has been positive, with Alibaba, Baidu and NetEase closing in green.

Some street comments:

Daisy Li, fund manager at EFG Asset Management:

“The biggest question I have is how the SOEs will come up with 2tn yuan from their offshore accounts and why they will choose to invest onshore through the Hong Kong exchange link”.

Liu Xiaodong, partner at Shanghai Power Asset Mgmt:

“It’s a huge piece of good news at first glance — but there are a lot of overhangs and complications, which means it might not materialize as soon as people hope. If they seek funds from SOEs, there are a lot of questions, such as how much cash is available, how willing are these firms to take part, and whether the funds would be moved all at once or in phases”.

Rajeev De Mello, a global macro portfolio manager at GAMA Asset Management in Singapore:

“Frequently, packages which target the stock market do have an effect but it can be very short-lived if not accompanied by more fundamental changes. Without more forceful economic and regulatory policy actions, it will not lead to the beginning of a bull market in China”.

Michelle Lam, greater China economist at Societe Generale HK Branch:

“An equity rescue package will help sentiment, especially if the recent selloff could be driven by technical factors such as snowball derivatives. The 2015 experience shows that even when the government steps up buying, the rally is not necessarily sustainable unless we have a bigger stimulus package to address the economic issues”.

Vey-Sern Ling, managing director at Union Bancaire Privee:

“The selloff has reached irrational levels due to a crisis of confidence. Much of it is due to the perception that the government doesn’t care about the markets. A rescue package may be insufficient on its own to prop up the market in terms of dollar value injected, but will certainly help dispel the idea that the government doesn’t care”.

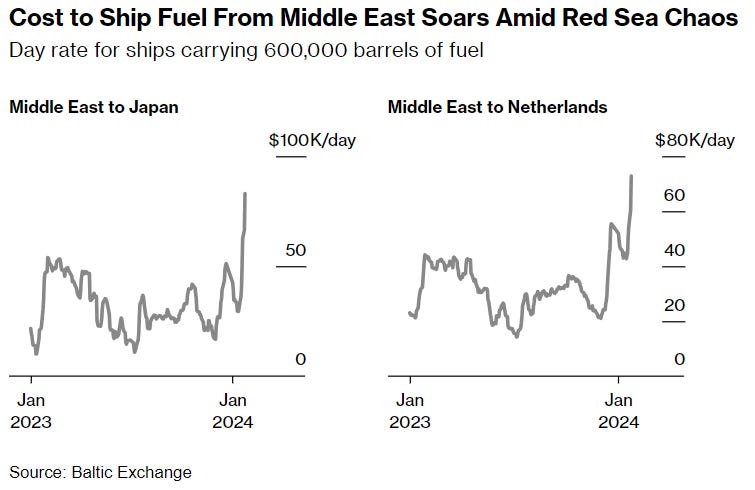

Suez Canal

The Red Sea route has become a key corridor for Russian oil cargoes in the wake of Europe's decision to stop buying from Moscow over its invasion of Ukraine. The Houthis have said they won't target those ships, though two have been struck, apparently by accident. Some other producers are also using the route, hoping to avoid the Houthis’ wrath. Most Middle East crude bound for the US Gulf Coast already goes around the Cape of Good Hope because it’s carried in tankers too big to fit through the Suez Canal when fully loaded. Transit volumes are plunging. Firms that highly depend on these routes could face lower margins (e.g. Primark, H&M, etc.), and other companies like Tesla and Volvo already announced a stop in production.

Fuel costs 3x now since the start of the conflict.

China has so far steered clear of the Red Sea conflict. The world’s biggest trading nation imports about half of its crude oil from the Middle East, and it exports more to the European Union than the US. The Houthis have said they won’t target Chinese ships.

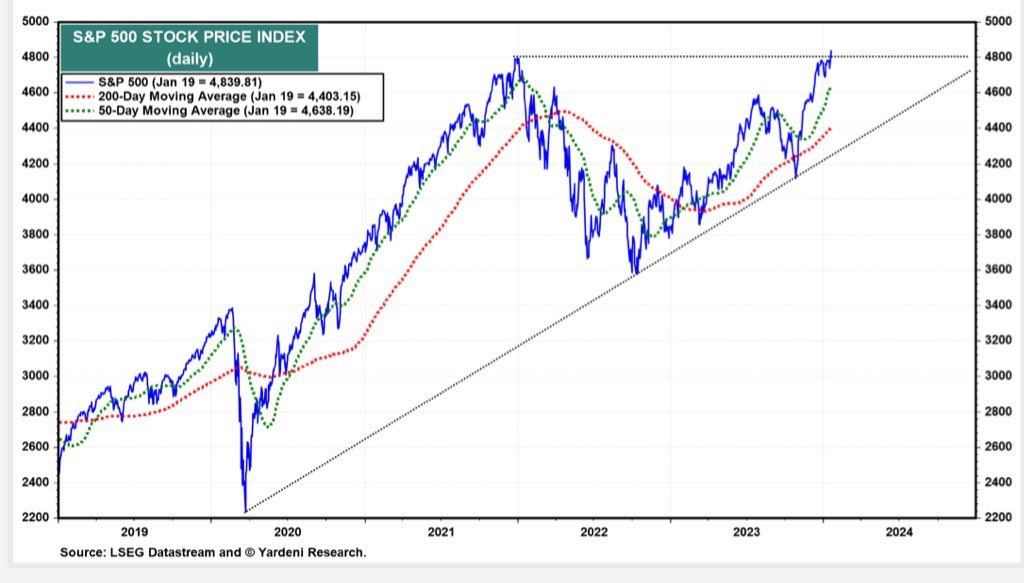

What’s happening in the markets

S&P 500 hits its highest closing price in history for the 3rd consecutive day on Tuesday.

Yardeni Research on the US equity market: “Now that investors’ recession fears have abated, they’re focusing on company fundamentals .. The possible result: an exuberant meltup phase, which might already be under way and might become irrational .. funded by money moving from interest-paying vehicles into stocks and bonds.” “a new scenario that we haven't discussed before”: We see a 20% probability of “a meltup in the stock market with technology stocks leading […] The forward P/E of the $SPX Info Tech sector is currently 26 […] it rose near 50.0 in 2000, so has room to soar […] in this scenario”.

Goldman Sachs: momentum traders sell stocks in ‘Every Scenario’. Cullen Morgan, an equity derivatives and flows specialist at the bank, expects that commodity trading advisers, or CTAs that surf the momentum of asset prices through long and short bets in the futures market, could be forced to sell after building US$ 129bn in long positions. The trend-following cohort are modelled to sell US$ 10bn in a rising market, and up to US$ 42bn if stocks decline, over the next week. On a longer time frame of one month, CTAs are likely to buy US$ 42bn in a rising market versus US$ 226bn to sell should markets start to trend lower again.

While the standout bond-market position over recent months of long Treasuries is showing signs of cracking, as traders bail on futures positioning into the back-up in cash Treasury yields.

In the week up to Jan. 22, JPMorgan client long positions dropped 2ppts, shifting into neutrals with shorts unchanged on the week. The survey shows outright long positions have now dropped from 39ppts in November to current 20ppts, the lowest since May. Meanwhile, client neutral positions have now grown to the most since April.

In the week up to Jan. 16, hedge funds were notably bearish 10-year note futures and stretched their net short positioning in the contract to a record, according to CFTC positioning data released Friday. On the week, net short 10-year futures position was extended by US$ 4.4m/DV01, to a short of almost 1.58 million futures.

There has been a notable shift in long-end skew to favor put options, as traders are paying a higher premium to hedge a selloff in the long-end of the curve over the past week. Some of the long-bond options put premium may be partly starting to reflect potential for a CTD shift in the long-bond futures contract and hedging around such a scenario. JPMorgan: mitigate CTD extension risk by buying bond puts.

Very nice, thank you!