Recession is coming!

Fed moves, Powell statements, market reaction and analysts' views

Hawkish pause

The Federal Reserve, as expected, halted its cycle of raising rates last night, keeping them within the range of 5% to 5.25%. However, the central bank's projections suggest that two more rate hikes are likely to occur later this year. Jerome Powell downplayed the significance of the dot plot forecast but acknowledged that inflation risks continue to lean towards the upside, and any reductions are not expected for "a couple of years." Jeffrey Gundlach from DoubleLine holds the belief that the Fed will refrain from raising rates in the near future, suggesting that they may have already implemented slightly excessive tightening measures.

Nevertheless, the revised median rate projection indicated an additional two 25bp rate increases by the conclusion of 2023, demonstrating a significantly more hawkish stance than expected. The initial market response waned to some extent during the press conference as Powell hinted that the hikes might not be as assured as previously thought, citing the emergence of factors required to mitigate inflation. The GDP forecast for 2023 was raised to 1.1% (from 0.4%), implying that the prospect of further rate hikes hinges on a reasonably positive growth presumption.

As it stands, investors are anticipating that the US Federal Reserve will persist in raising interest rates, and the majority do not foresee any reductions taking place until late into 2024. According to a survey conducted by Instant MLIV Pulse, 70% of the 223 respondents believe that Chair Jerome Powell and his colleagues have not yet concluded the campaign of rate hikes initiated in March 2022, triggered by the spike in inflation during the pandemic. Conversely, 30% of the respondents stated that rates have reached their peak..

Asked when the Fed will start reducing rates, about 56% said it won’t do so until the second quarter of 2024 or beyond, while around 35% pencilled in a decrease in the opening three months of next year. A 10th predicted the fourth quarter of 2023.

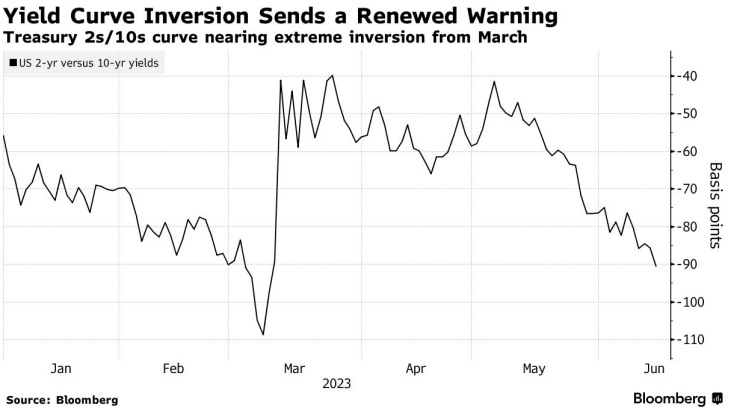

Bond market adjusted and started pricing an incoming recession. The risk is real: short term treasuries have been sold and the spread between 2y and 10y is now at around 90bps.

What can we grasp from Powell comments?

We can summarize the FOMC in 3 key phases:

Markets scared by the dot plot (indices -1.5%)

Powel “calming” them stating there will be a pause to see the effects of the interest rates (indices recovering)

Hawkish signs: core PCE still high, no cuts in 2023 and yet too see if it will be possible to cut in 2024 (indices flat)

Let’s see some important statements.

Powell expressed that nearly all FOMC policymakers deem it suitable to implement some additional rate hikes within this year, while most policymakers anticipate continued subdued growth. He also acknowledged that although inflation has moderated to some extent, it remains well above the 2% target, with persistent inflationary pressures. Achieving a return to 2% inflation still requires substantial progress. Additionally, Powell clarified that the Fed's projections do not constitute a definite plan or decision, and they will make decisions on a meeting-by-meeting basis.

During the Q&A session, Powell emphasized that the key concern is determining the extent of further tightening. He highlighted the rationale for gradually increasing rates, albeit at a more moderate pace. The topic of adopting an every-other meeting approach was not discussed, and Powell expressed that the July meeting is expected to be active. Initially, Powell referred to the decision as a "skip," but swiftly corrected himself by stating that it should not be characterized as such. He asserted that by allowing for a more gradual tightening approach, the risk of going too far is mitigated. He further mentioned that reducing rates would be appropriate once inflation subsides, but emphasized that rate cuts are not warranted within this year, and none of the policymakers projected a rate cut for the current year.

Powell indicated that rate cuts are likely to be implemented in the coming years. On Thursday, Treasury yields experienced a slight decline, with 10-year yields increasing by two basis points to 3.81%. Swaps traders currently estimate a roughly 50% probability of a 25 basis point increase in the Fed rate by the end of the year, after having almost entirely priced in a rate cut at the beginning of June.

What does the street think?

Bernstein

It seems clear that a rate hike is coming in July barring a significant deterioration in the data—specifically the next employment report.

Because I expect the labour market to weaken as the economy slows later this year, I believe that the July rate hike will be the last one. But if the labour market does not weaken, I will be wrong and they will continue hiking. I do not expect a rate cut this year; it would take a true hard landing for that to happen.

The underlying picture today is that the economy appears on track for a soft landing—either a mild recession or no recession at all. As long as that is the case, the Fed will not face an imperative to cut rates and, until inflation is meaningfully marching toward target alongside a weaker labour market, it will be inclined to raise rates. The market has (appropriately in my view) removed rate cuts from its pricing for 2023. The first cut is now not fully priced until March of 2024.

Goldman Sachs

"We have not made any changes to our forecast of one additional hike in July to a peak rate of 5.25-5.5%. The combination of the hawkish surprise in the dots and the hint at an every-other-meeting pace strengthens our confidence that the FOMC will hike in July and makes a possible second hike more likely in November than September, though neither is in our baseline forecast".

We saw a continuation of downside resetting lower post FOMC. Single stock skew is at 2021 levels and SPX index skew is close to 5 year lows. We agree with Goldman's hedging logic here " From a micro standpoint, collaring longs looks attractive given flat skew (put vs call) - for either protection or stock replacement".

JPMorgan

The outcome of today’s FOMC meeting was hawkish, and peculiar: while the Committee unanimously voted to leave rates unchanged, a large majority of FOMC participants anticipate at least two more rate hikes this year, and only two see the current setting as the appropriate terminal rate. So why not just go ahead and hike today? Chair Powell said it was a continuation of the process of slowing down the speed of hikes. He tried not to tip his hand on July but given how many on his committee are inclined to hike multiple times this year, it may be hard to get them to pause for more than one meeting. As such, we now look for one more 25bp hike at the July meeting. We continue to believe the lagged effects of rate hikes will weigh further on growth, and don’t believe the median’s two further hikes will be needed.

Bank of America

Our forecast is now as much a “growth recession” as it is a “mild recession”. In turn, we revise our outlook in favour of a more gradual back up in the unemployment rate and a slower pace of disinflation. We now forecast core PCE inflation to end the year 40bps higher at 3.8% 4Q/4Q and 20bps higher next year at 2.4% 4Q/4Q. We think price stability will be achieved in early 2025. We have the unemployment rate peaking at 4.7% in 4Q 24, a bit below our prior peak and three quarters delayed.

We look for an additional 25bp hike in September for a terminal rate of 5.5-5.75%, though the Fed may decide the last hike should come in November per the Chair’s guidance that the Fed would prefer to move every other meeting as it assesses the effects of prior rate hikes. Finally, we now think the first rate cut and the end to QT comes in May 2024, versus March 2024 in our previous forecast.

Santander

Risk-off mode in the wake of the FOMC meeting. Any pivot by the Fed has been long-grassed after a June pause with clearly hawkish tones. Not only have we seen an aggressive revision of the dot plot, which now clearly shows two additional rate hikes this year (nine dots at 5 5/8, four at 5 3/8, three above 5 5/8 and only two at the current level). But economic forecasts have also been revised up, accompanied by a sharp increase in core inflation forecasts for this year too (from 3.6% to 3.9%). And Jerome Powell's statement and tone clearly suggested further hikes this year. Perhaps, as our economists note, following a “pause-hike-pause-hike" pattern similar to the one we are now seeing in Canada and Australia. In short, bad news for the credit market pending the mood at the ECB today as it announces (or is expected to) a penultimate 25bp increase. As was the case in December, following the market rally, it seems clear that central banks do not believe that the sound market situation, with the S&P 500 in bull market and European markets, especially that of Germany, at record highs, is helping to combat inflation.

HSBC

US rates strategy: We continue to expect a volatile range trade in the near term. The FOMC seems unlikely to support a dovish view in the near term. We continue to see the 10-year's yield as roughly bounded in a 3.5-3.8% near-term range.

Credit strategy: We retain our neutral stance in US credit. In our view, now is not the time to materially shift risk from Treasuries into US corporate bonds. But neither should investors be too bearishly positioned.

Multi-asset strategy: Given such high levels of uncertainty, we would argue that despite the more hawkish statement, "dots," and forecast changes, the outlook on risk assets has not changed significantly. As such, we think positive activity surprises and better-than-expected earnings delivery could also continue, clearing the way for a continued rally in risk assets.