Soft landing? What does the street think

Analysts views on what is happening this weeks: CPI, PPI, treasuries...

Street view on Economy and rates

Morgan Stanley – most bullish bear ever. We had "best recession ever" and now Mike Wilson becomes the most bullish bear ever. Mike Wilson expects near-term uncertainty to give way to an earnings recovery. For December 2024, Mike forecasts a 17.0x P/E multiple on 12-month forward EPS (2025) of US$266, which equates to a 4,500 price target ~12 months from today. Mike sees a strong earnings growth environment in 2025 (+16%Y), as positive operating leverage and tech-driven productivity growth (AI) lead to margin expansion.

Morgan Stanley and Goldman Sachs go toe to toe on their view for when the US Federal Reserve will cut interest rates! MS think the central bank will start cutting rates in June 2024 with an end destination of 2.375% by the end of 2025, whereas GS is less bearish and more aligned with the Fed seeing the first 25bps reduction in Q4 2024, with rates settling at a 3.5%-3.75% target range.

Morgan Stanley: 3.95% target. Rates strategist Guneet Dhingra expects US Treasury yields to move lower over the forecast horizon, with 10-year Treasury yields trading around 4.20% by 1H24 and 3.95% by the end of 2024. For 1H24, he expects 10yr yield to go down, driven by the following factors: 1) 10yr yield becomes increasingly de-coupled from growth as Chair Powell emphasizes the role of rising labour supply 2) Cooling growth as the economy feels the impact of higher rates and labour market weakens 3) The perception of Treasury oversupply gets de-bunked as US Treasury shows increasingly flexibility around coupon supply 4) Fiscal policy, which played a key role in lifting growth and yields higher in 2023, does not provide any further impetus heading into the US elections in 2024.

Goldman Sachs says that a still-bright world has dark sides. These are the risks they think are worth keeping an eye on. 1) the higher-for-longer rate environment could cause more vulnerable EM sovereigns to lose market access, lead to a further rise in Euro area sovereign stresses, and complicate the policy trade-offs facing policymakers in China and Japan. 2) this rates environment may expose areas of vulnerability in the US related to smaller companies’ access to finance, continued pressure on some credit provision by small banks, and subdued mortgage, housing, and commercial real estate activity. 3) the deteriorating public debt profile in DMs is a growing concern. 4) rising geopolitical concerns and, in particular, the risk of an escalation of the war in the Middle East could lead to significant increases in energy prices.

Goldman Sachs: “The hard part of the inflation fight now looks over […] the heaviest blows from monetary and fiscal tightening are well behind us […] We expect the FOMC to […] cut in 2024Q4 once core PCE inflation falls below 2.5%. We then expect one 25bp cut per quarter until 2026Q2 […] Two key risks remain .. a spike in oil prices […and] the risk that something could ‘break’ in the new rate environment. The risks are real but manageable, in part because the Fed would be at liberty to cut in response next year and will have plenty of room.”

Goldman Sachs said “go long” on commodities as demand is set to improve. “We believe that a fading monetary policy drag, receding recession fears, and reduced industrial destocking will support demand and spot prices in 2024,” it said. The bank cut its 2024 Brent average price forecast to US$ 92 from US$ 98.

JPMorgan vs JPMorgan: Marko Kolanovic (PhD): "we believe that equities’ risk-reward remains unattractive: restrictive monetary policy is likely to remain in place for some time, equity valuations are rich, and consumers are likely to begin to retrench given a fading liquidity buffer, high rates across a range of consumer loan products, tightening lending standards, and rising delinquencies"; Andrew Tyler (head of Market Intel desk, i.e. people who actually trade): "we remain tactically bullish given stable growth with a disinflationary trend, positive earnings growth, positive technicals, a shift towards a soft landing narrative, and the end of the Fed’s hiking cycle. Amid heavy macro catalysts this week and the risk of US government shutdown this Friday, we may see slight pullback, but we still hold the view that we would buy that dip".

Analysts after CPI

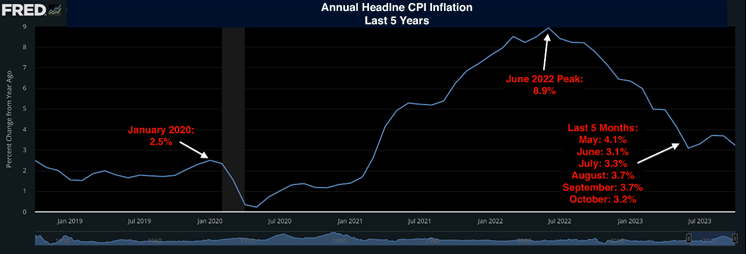

October CPI came in below expectations on both the headline and the core measures. Headline M/M prices were flat in October, beneath the expected +0.1% rise and cooling from September's +0.4%, while the Y/Y eased to 3.2% from 3.7%, beneath the 3.3% forecast. The core metrics were also soft: Core M/M rose 0.2%, softer than the prior and expected 0.3%, while Core Y/Y rose 4.0%, beneath the prior and expected 4.1%.v Gasoline and car prices drove much of the decline, but rents inflation also resumed its downtrend.

Following the inflation report, swaps put the chance of another Fed hike at almost zero, while pricing in about a 50-bp cut by July. The Fed’s Austan Goolsbee said the figures showed progress, but there’s “still a way to go.” Jamie Dimon warned inflation “might not go away that quickly.” Ken Griffin said the US central bank risks “losing credibility” if it cuts too quickly. Barkin is "not convinced inflation is on a smooth glide path down to 2%". Cathie Wood said deflation is already underway.

Market is now pricing in 100bps of rate cuts next year.

JPMorgan's David Kelly on CPI: It is notable that almost 90% of the 3.2% year-over-year increase in CPI for October came from rent, owners’ equivalent rent and auto insurance, categories that are all likely to see much lower inflation in the year ahead.

TS Lombard's Blitz: CPI follows a cooling economy. 1) October CPI data reflects a slowing economy, diverging from September's signs of recovery. 2) Macro factors, transitioning from COVID disruptions, are predicted to increasingly drive CPI. 3) Economic uncertainty persists; Q4 growth forecast at 1.5%, influenced by rate hikes and liquidity adjustments. 4) Notable declines in discretionary spending, evidenced by reduced airline fares and hotel rates in the October CPI.

US 10y drops 18bps to 4.46% after inflation data which should eliminate any expectation that the Fed will raise rates again in December or thereafter.

HSBC: We expect the first Fed rate cut in Q3 2024. We maintain our US Treasury yield forecasts well below consensus. It is likely that the next 100-150bp move in yields is down rather than up. We expect the USD to remain strong in 2024, aided by soft global growth.

Nick Timiraos: The October payroll report and inflation report strongly suggest the Fed's last rate rise was in July. The big debate at the next Fed meeting is shaping up to be over whether and how to modify the postmeeting statement to reflect the obvious: the central bank is on hold.

DataTrek: Higher for longer is over. 1) a zero monthly headline inflation reading such as yesterday has been very rare over the last 2 years 2) the 3.2% headline annual rate suggests we are back on the right track in terms of seeing lower inflation in the future 3) “Shelter” comprised 58% of this month’s core inflation reading, and without this component core inflation would have been just 1.1%. That, of course, is far below the Fed’s 2% target.

The most crowded trade for 2024: BofA’s latest fund manager survey showed investors were dumping cash to hold the biggest overweight position in bonds since 2009. The “big change” was not the macro outlook, but expectations that inflation and yields will move lower in 2024. 61% of Fund Managers are predicting that long-term bond yields will be lower in 2024. This expectation surpasses even the peak of the Global Financial Crisis when only 40% of managers expected lower long-term bond yields the following year.

Goldman Sachs: Too much optimism on rate cuts...? "Markets are front-loading rate cuts particularly in the US, which we view as overdone". Chart shows policy rate changes priced across G10 economies.

Bonds turning and turning again (Bloomberg)

10-year Treasury yield is higher than it was last Thursday, 9th November: a date before inflation report.

However, PPI data should have supported a continuing fall in yields. Excluding fuel, producer price inflation dropped to its lowest since early 2021, and is now close to the Fed’s target of 2% for CPI. It also came in below forecasts after several months of disappointing investors.

Should we be surprised that the bond market had second thoughts? The history of the last two years, as inflation and then policy rates took off, suggests we shouldn’t. Henry Allen, macro strategist at Deutsche Bank AG in London, identifies seven attempts by the market to take yields down in response to a Fed pivot in the last two years. All of the first six proved not to be pivotal.

Many think that we could see a soft landing scenario, but if we say that a soft landing is a period of rising rates that doesn’t lead to even a quarter of negative economic growth, then there has been precisely one in the post-Volcker era.

That soft landing came while globalization was taking hold as the Clinton administration feasted on the “peace dividend” from the end of the Cold War and moved the federal budget into surplus. None of those things apply now, so a soft landing looks implausible.

But today, Fed keeps being hawkish both due to the (still) high inflation and for the loose conditions caused by the rally in stocks and bonds of the last two weeks.

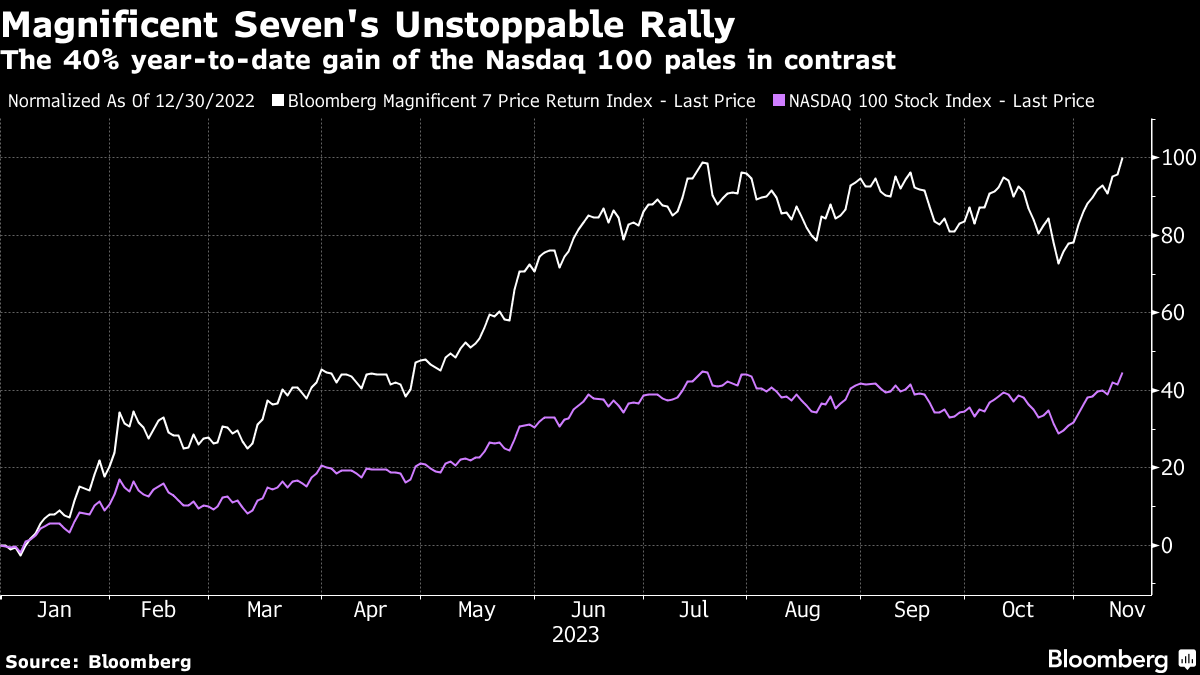

However, it seems that investors are ignoring these signals and keep hoping in rates cuts. In fact, despite an already +100% of Bloomberg magnificent Seven Price Return Index (an equal-dollar weighted equity benchmark comprising Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia and Tesla) and +40% of the Nasdaq, they still are long tech and underweight banks.

The optimism is evident. Investors polled said they are the most overweight tech relative to banks since November 2020, around the time vaccines against Covid-19 were rolled out. Not only that, they also snapped up tech stocks at the fastest pace since May 2023 and are now their most overweight that sector since November 2021. All the attention given to the narrowness of the market hasn’t dented their ardor:

With less than 30 trading days until the end of year, it’s hard to imagine what could kneecap the Magnificent Seven after a spectacular rally. At this point, the inertia carrying it to Jan. 1 is hard to overcome, as fund managers will be anxious to have these stocks to show off in their portfolio a year-end. But in this environment, news tidbits can whipsaw markets, as we’ve just witnessed. For the very short term, it’s perhaps safest to expect their luster to continue, at least in the US — but also to get ready for far more appealing opportunities elsewhere.

Thinking about The Magnificent Seven, we may want to remember the great movie, in the end only 3 survived! Just saying...