Stocks at a crossroad, bonds can shield vs market volatility

Risk assets could continue to see weakness

"Sometimes people don't want to hear the truth because they don't want their illusions destroyed"

Friedrich Wilhelm Nietzsche

Let’s dive in the latest macro developments and key market drivers

This summer, US stocks have experienced one of their best summer rallies, gaining 12% in Jul/Aug, despite the worrying macro conditions of the market: inflation, central banks hiking rates, European energy crisis, geopolitical tensions and others.

The positive narrative we heard since mid-June is that US inflation has peaked, rates should hit a terminal rate of 3.25% in the first quarter, a recession is inevitable and central bankers will be forced to pivot and cut rates in the second half with inflation – mostly driven by energy – coming back below 4% by then. We doubt the Fed is already done with rising rates.

Many were waiting for this equity market pullback, but many more were caught off guard by the rebound strength, creating calls for a “brand new” bull market. While investors have enjoyed the recent rally, we are not keen to buy this narrative; on the opposite, we want to highlight the excessive comfort level of the equity market compared to the dire status of the global economy.

Market can stay irrational for a long time, but it always “mean revert” toward its fair value. This time we have the central banks in play and investors should never fight them.

In the latest run, the stock rally has broadened: the share of S&P stocks closing above their 50-day moving averages recently surpassed 93%, the highest level since the summer of 2020.

A swath of stocks has participated in the market’s recent rebound, typically an encouraging sign of a rally’s durability. Yet few investors are willing to call a market bottom, especially after such a punishing year. A widely followed technical indicator for market breadth recently hit a key milestone: the share of S&P 500 stocks closing above their 50-day moving averages rose earlier this month to 93% – the highest level since the summer of 2020 – and held above 90% for most of last week, according to FactSet.

Wells Fargo's Chris Harvey: “The fundamentals are less impressive. With earnings almost done, operating margins are tracking ahead of Q1's but energy stocks account for 90% of the upside. Other sectors have seen margin declines, like staples, info tech & communication services.”

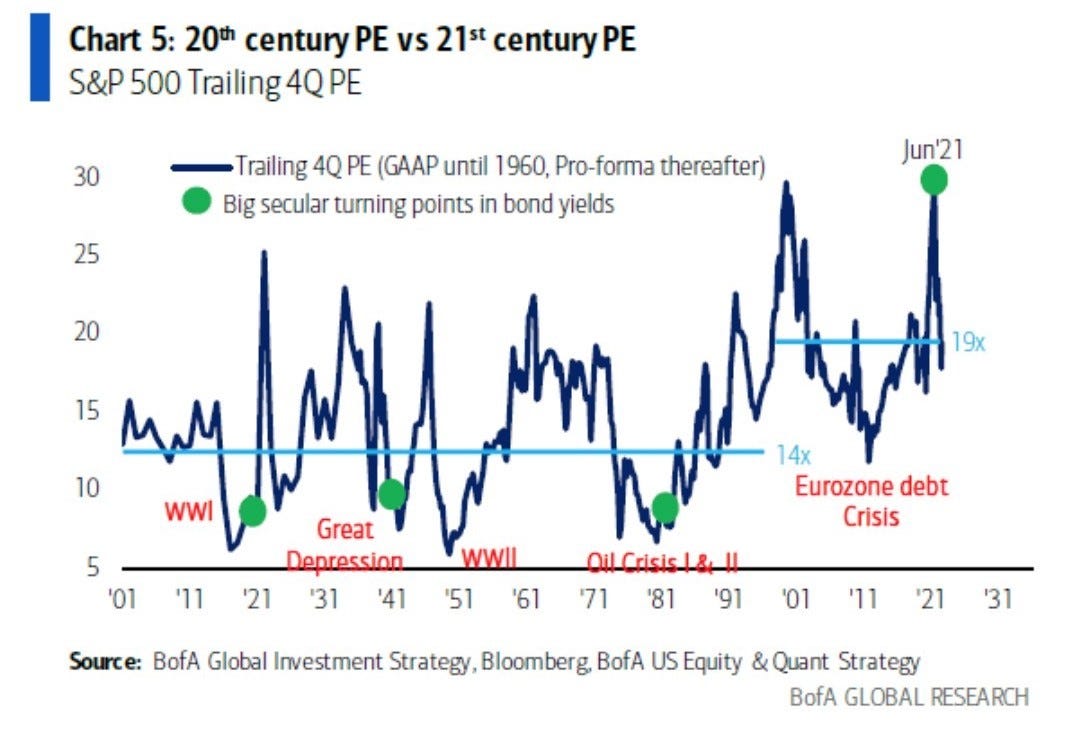

BofA sees 3,300 SPX as P/E declines to historic 15x on the back of shortages in labor, energy, places to live (rent), food, materials, inflation to stay high. "S&P500 companies generated $220 of EPS per 12 months; applying a 20th century PE of roughly 15x gets you to an S&P500 index of 3300, applying a 21st century PE of 20x gets you to an S&P500 of 4400; there’s your range. However, everything in last decade is now reversing."

Still, according to another BofA report, the S&P 500 is only pricing in a 20% chance of a recession now vs. 75% at the peak of Russia-Ukraine fear.

The S&P 500 has struggled to close above its 200-day moving average during the past week. Historically, failing to break the 200-day moving average could lead to a decline for equities in the incoming months. This level (currently around 4,300) is an important one to watch. Additionally, the current rally has failed to break the downtrend that has been in place since the beginning of the year:

What happened in the past under the same conditions?

In May 2008, S&P 500 could not break the resistance and began plunging until reaching the bottom of 57% in March 2009. The same happened in the bear market of 2000–2002: 200 MA not broken and huge decline (of 49%).

What about sentiment?

Technical sentiment is moving net bearish and fundamentals back towards the lows. Bond survey likewise back towards the bearish side, with technicals dropping from bullish to neutral, and renewed doubts on the fundamentals. Overall the concern from these two surveys would be a repeat of bonds and stocks down. Combined surveys macro/fundamental gauge remains weak, downtrending. Consistent with the global PMI dropping below 50. Here the charts from the insightful Topdown Charts:

Don’t forget the VIX

Yesterday we had a market sell-off, taking a breadth from the rally. And we also had an important VIX breakout. Another key variable to watch.

On a macro level, the framework challenges even the most optimists

Federal Reserve officials appear determined to bring inflation down by causing a recession. Terminal rates are likely to hit 4% or more. Low unemployment and wage pressures mean that even if energy and commodity prices cool, other forces will keep CPI high.

Meanwhile, UK and European inflation continues to rise with monthly numbers continuing to surprise to the upside, primarily for a huge increases in energy prices (gas) and food, as the hot dry summer takes its toll on agriculture.

UK CPI hit 10.1% last month, with food prices rising by double-digit amounts. The next quarter or two is going to get a lot worse for European consumers and for manufacturers with high energy needs. Yesterday, Citi reported that UK inflation is on course to hit 18.6% in January (Citi updated forecast), the highest peak in almost half a century, due to soaring wholesale gas prices.

Finally, German benchmark electricity price jumped >25% on Monday to pass €700 per megawatt-hour for the first time. The level is about 14 times the seasonal average over the past five years. The surge came on the back of another leg higher in natural gas prices which rose over 13% in Europe amid concerns around the next scheduled 3-day maintenance of the Nord Stream 1 pipeline. Priced in dollars per barrel of oil equivalent, German electricity is over US$ 1,000/ barrel! A madness!

Another concern is the Euro continues to fall below parity with the Dollar. Now, 1 Euro is worth only US$ 0.9900. This is the first time in 20 years that the dollar is worth more than the euro.

Fed’s hawkish reality check continues to fuel a dollar rally (still considered a safe haven currency), with the greenback yesterday hitting 5-week highs. Stronger dollar continues to act as a wrecking ball for risk assets, with equities crumbling, and commodities continuing to slide.

In this context, the Fixed Income can come to support. Companies’ bonds have performed well after bottoming in mid-June, gaining 4.6% in the US and 3.4% globally. High quality bonds can offer a potential flight-to-safety, when the risk assets like equity, high yield bonds and crypto are weak.

Christian Hantel, a portfolio manager at Vontobel Asset Management, points that especially high-grade bonds would benefit from falling government yields:

“The potential damage to investment grade seems limited. In a risk-off scenario government bond yields will go lower and lessen the effect of wider spreads.

There is a lot of risk around and it feels like the list is getting longer and longer but, on the other hand, if you are underweight and even out of the asset class, there is nothing more you can do. We have been getting more questions about investment-grade, which signals that at some point we should get more inflows.”

Worth also noting that overall, US corporate debt to equity is currently very low. Non-financial debt as a share of equity (25%) is currently at the low end of historical range.

That’s why we continue to sponsor the idea to increase the portfolio allocation toward higher quality bonds. The interest rates curve inversion (where the yield of short term rates are higher than longer ones) combined with a decent credit spread on BBB-/BB+ ratings (around 200bps) can offer on average an yield of more than 5% in USD and 2.5%-3% in EUR. Screening further it is possible to find bonds with great yields, good credit metrics and low duration, that can shield against periods of market volatility.

Contact us for more detailed information on bond selection and our views.

Buckle up with the Jackson Hole approaching (starting on Thursday), as this event could create further market volatility. Market expects Fed Chair Powell to emphasize the Fed’s commitment to restoring price stability.

Our bias remains skewed toward eventual market weakness in the weeks/months ahead with the S&P 500 at risk of breaking the 4,000 level.