Summer Chill: a look at the market

A recap of macro, equity and bonds environment

This week will be eventful as we will gather more information from Central Banks meetings and many earnings reports. In particular, we will have more hints on future effects of inflation.

About inflation, IMF is highlighting that overall global headline inflation seems to have peaked and core inflation has eased somewhat. However, if we break it down by region, we will find a divergence – with Emerging Countries close to their inflation targets, while Developed Markets are still a considerable distance away from achieving theirs.

Crescat Capital on inflation expectations:

“This is a chart of the 30-year expectation for inflation by the market. It's probably one of the most bullish technical setups that I have seen. A major breakout followed by 2-years of consolidation. Just when investors believed inflation was behind them, it is starting to show its teeth again”.

On the future effects, the Financial Times points out that the Federal Reserve needs to stay put on rates. With inflation falling, further tightening of monetary policy only heightens the risk of recession and financial instability. The trends provide hope that inflation can be meaningfully reduced if not defeated without choking off the economy, so long as the Fed does not overshoot.

On the other hand, the Fed expert Nick Timiraos said that US economic growth has likely been too firm in recent months for Fed Chair Jerome Powell to signal that Wednesday’s increase in the Fed’s benchmark short-term rate - to a 22-year high - will be the last of the current tightening cycle. The recent slowdown in inflation also makes it hard for central bank officials to firm up plans for any additional rate increase.

For the today FOMC meeting, the probability of the Fed raising interest rates again has reached 100%.

On the companies’ earnings, meanwhile, Morgan Stanley notes that two-thirds of S&P industry groups have seen earnings revisions decelerate over the past 2 weeks.

Mike Wilson also highlights that the earnings revisions breadth has decelerated and is now back in negative territory (meaning more downward than upward revisions for the out year).

Until now, Q2 earnings season saw 87 companies reporting. The good news: 78% of them beat estimates, by an average 6.2%. But we have to wait another week to see if we get a similar bounce as in Q1. The blended growth rate is -9.3% (worst since Q2 ’20). Per FactSet projections, earnings growth is expected to turn positive in Q3.

Equity

In the US, yesterday the S&P 500 raised to its highest level in 15 months, Brent Crude oil prices closed above US$ 83/bbl for the first time since April, and US HY credit spreads reached their tightest level in 15 months too. In addition, there was a significant milestone for the Dow Jones, which recorded a 12th consecutive gain for the first time since 2017. If we get a 13th today that would be the longest run since 1987, so one to watch out for.

There is no doubt sentiment among stock investors have soared with recession calls scaling back.

But most keep being bearish, as the great majority of big Wall Street strategists are implicitly predicting a terrible time for the stock market over the rest of this year.

At least, some are conceding they missed Q1 forecasts. Morgan Stanley's chief US equity strategist Mike Wilson, one of the most popular bears, sent a note to clients this morning admitting that he stayed bearish for too long so far this year.

He said he stuck with the pessimism for too long amid a rebound that has left equity benchmarks within spitting distance of erasing last year’s decline. Strategist underestimated valuation expansions, missed AI boom, but still sees cool inflation posing threat to corporate earnings. But his forecast for the S&P 500 remains 3,900, a level that has been left behind in the index’s 19% jump to around 4,560.

“We remain pessimistic on 2023 earnings. Inflation is now falling even faster than the consensus expects, especially the inflation received by companies. With price being the main factor that has held sales growth above zero for many companies this year, it would be a material headwind if that pricing power were to roll over”.

JPMorgan Marko Kolanovic, who turned into one of Wall Street’s most noted bears this year, it’s all still a recipe for a rout. The strategist warned that the delayed impact of aggressive interest-rate hikes by global central banks, dwindling consumer savings and a “deeply troubling” geopolitical backdrop are poised to spur fresh market declines and volatility.

“We acknowledge that we cannot time this inflection near term, but there are no data points that would prompt us to change our methodology or conclusions”.

Kolanovic still thinks a selloff is coming thanks to a delayed impact from rate hikes and a "deeply troubling" geopolitical backdrop, but he admits he doesn't know when.

"The level and increase of stock concentration in S&P 500 now is at 60-year highs. [...] This could be indicative of a bubble, and other anecdotal evidences point to an AI-driven bubble as well".

From a positioning perspective, JPMorgan said that momentum correlation indicator suggests one of the sharpest rises in Momentum crowded risk in several years, approaching August 2018 and February 2021 levels. Both of these periods preceded two quick and strong factor rotations in the market.

Is US equity overvalued?

Fidelity’s Timmer said:

The market seems to be over its preoccupation with the Fed, no longer pricing itself off the Fed cycle. Instead, it’s pricing in an anticipated earnings recovery. If earnings growth reverts to its historical trend of 6%, at an equity risk premium of 4.2% the market is fairly valued at 20x. But with the gap between the rate cycle and the anticipated soft landing getting wider by the day, a lot needs to go right here for the rally to be justified.

At 20.2x, much of the early cycle playbook has been priced in. There is more room for gains based on the typical 40-50% expansion in multiples during the early phase of recoveries (which would take the S&P 500 to 21-22x), but the Fed might throw some cold water on the bulls if it stays higher for longer. A recession, if and when it hits, could hurt too.

Berenberg highlights US equities trade above a 12-month forward P/E of 20x for only the third time in the last 50 years; the last two times that US equities have been this expensive were both liquidity fuelled bubbles. Tech is now trading at a 54% premium to the market:

“We struggle to recommend an overweight in tech for the second half, and believe stock picking increasingly matters, particularly since the five largest tech companies account for nearly 56% of tech's total capitalization (and the top 2 account for 33%), three of which are at very high relative valuations (95%+) vs. history. Our reluctance to recommend an overweight stems from the sector's combination of historically high valuations but average expected five-year relative growth looking forward. However, it is tough to be underweight tech given the sector's strong momentum, historical outperformance (62% of the time in the last 20 years), and potential for falling interest rates in next 6 months. We recommend a market weight in tech, and that investors maintain a balanced 'barbell' between expensive/growth and inexpensive/value tech stocks".

If P/E levels reach again the pandemic levels, equity could go up again and if it reaches a +15% it would be hard to fall at the bearish analysts target levels.

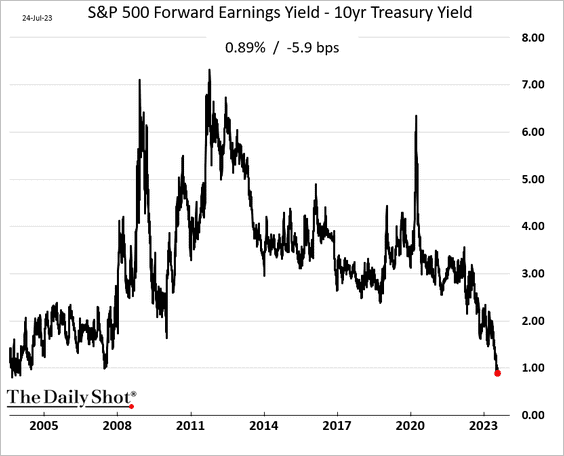

One of the biggest headwind for the future equity performance is the lowest S&P 500 risk premium in more than 20 years.

Equity markets are almost priced for perfection

Citigroup said that there are so many bulls in the US stock market that any disappointment on the economy or earnings poses a risk to the rally. “Overall positioning risk remains elevated and of concern, with notional levels still near long-term highs, if the current economic and earnings outlook were to abruptly surprise to the downside”.

Bonds

TD Securities saw that global bonds saw their 17th consecutive week of inflows, reaching a total of US$ 1.4bn for the week to July 19th, primarily driven by US$ 1.2bn inflows into the US market.

And bond traders bet on ‘Nirvana’ in new decoding of Yield Curve. Ed Yardeni says that the yield curve is signalling the slowdown in inflation that typically accompanies a recession but not the actual recession itself. He calls this the “Nirvana scenario” – all the gain (an end to nasty price increases for consumers) without much pain (a spike in unemployment or a major hit to the stock market). And that’s manifesting itself in the Treasury market the exact same way that a looming recession would: high yields on short-term debt and lower ones on longer bonds as traders anticipate the Federal Reserve will start cutting interest rates next year.

“It’s conceivable that the interpretation of what the yield curve is saying here is that the Fed managed to succeed in bringing inflation down. The economy has proven to be remarkably resilient and the Fed may not have to raise rates much higher”.

Over at BofA, strategist Meghan Swiber is on board:

“The curve shape is more a function of expectations for declining inflation than a deterioration in growth.”

Economists at Goldman Sachs are urging investors to dismiss the yield-curve’s inversion, saying it’s more reflective of other long-running market trends. And the recent, sharp rally in stocks signals investors have come to the same conclusion.

Meanwhile, JPMorgan shows US junk loan getting downgraded at increasing pace: America's US$ 1.4tn risky corporate loan market has been hit by the biggest slew of downgrades since the depths of the Covid crisis in 2020, as rising borrowing costs strain businesses piled high with floating-rate debt. FT

Finally, Apollo’s Torsten Slok is not shy in talking about the credit deterioration ahead of us: a default cycle has started, and markets are not paying attention. "Markets are not taking the ongoing rise in default rates for HY and loans seriously, see charts below, and many investors argue that “this is just a normalization,’ or “these are companies nobody has heard about.”

Great overview! Thank you!

great coverage, thank you!