Tech earnings: Meta, Google, Microsoft

Leaders of tech sectors reported disappointing results

While investors are waiting for AAPL 0.00%↑ and AMZN 0.00%↑ earnings, market has already being hit by the other tech sector giants’ reports.

Meta’s market value has collapsed by US$ 520bn in the past year and is on the brink of getting booted from the ranks of the 20 largest US companies. It trades at a 50% discount to the Nasdaq 100, the steepest ever:

Meta plummeted 20% on Wednesday 26 October post-market after its revenue forecast missed estimates due to a shaky ad market. Spending was way above expectations and the company said hiring will "slow dramatically" this quarter.

Operating losses will grow significantly year over year, but Mark Zuckerberg asked for patience, saying the focus on the metaverse will pay off.

Meta Platforms Inc Q3 2022 (USD):

EPS US$ 1.64 (exp. US$ 1.88)

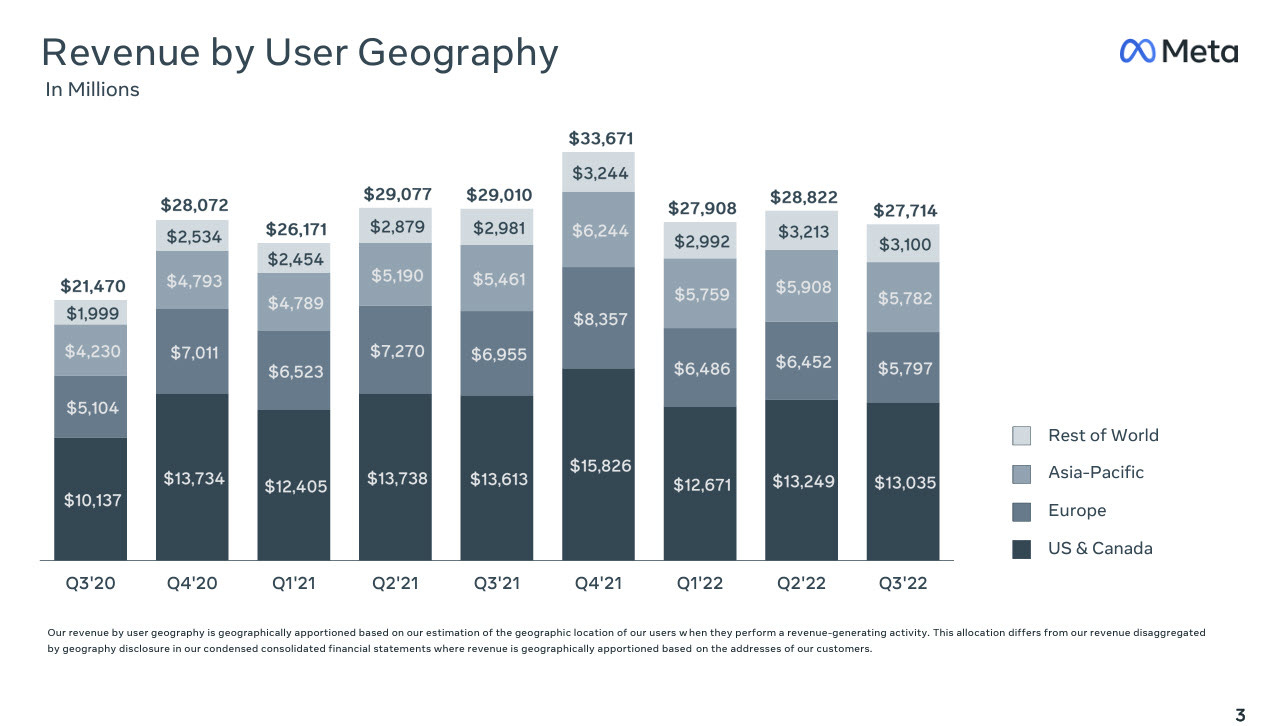

Revenue US$ 27.71bn (exp. US$ 27.38bn)

Facebook DAUs US$ 1.98bn (exp. US$ 1.86bn)

Facebook MAUs US$ 2.96bn (exp. US$ 2.97bn)

META average price per ad -18% (exp. -15.3%). Co. said it faces near-term challenges on revenue, and sees reality labs op losses in 2023 significantly higher. CFO said revenue from large advertisers remain challenged, while revenue among smaller advertisers remain more resilient.

Facebook revenues fell 4.5% over the last year, the largest decline in company history.

Meta’s report is the latest sign of trouble in the online advertising market, which is getting hammered by factors including Apple’s 2021 iOS privacy update and fears of an impending recession. Those concerns have caused companies to slash their marketing and ad campaigns.

Moreover, competition from competitor TikTok increased as Jefferies shows that IG Reels engagement significantly lags behind.

"While TT's lead over META is concerning, we would argue that the differential in time spent also represents an opportunity for META to address the highly engaging short-form video market".

On Tuesday 25 October, Jefferies cut Meta target price to US$ 200 from US$ 225 after lowering their full-year 2023 revenue growth estimates to 5% from 7%, citing macro uncertainty, ahead of the company’s third-quarter results.

However, Jefferies' was maintained at Buy and its analysis indicates it can flip from a revenue headwind to a tailwind by FY24.

"In the n-t META faces tough 2H comps, but the stock set-up becomes more attractive in 1H23 as comps ease and Reels monetization becomes material. The macro impact on ad budgets creates uncertainty, but could be reflected in the stock's all-time low valuation (12x FY23 EPS)".

Microsoft posted its weakest quarterly revenue growth in five years, throttled by the surging US dollar and a slump in sales of Windows software to personal-computer maker

On Tuesday, Microsoft shares down 7% on worsening outlook. FY23 Q1 (ending 30 September) revenue was US$ 50.1bn vs est. US$ 49.6bn and EPS of US$ 2.35 vs est. US$ 2.29, but it was the forecast for the current quarter that negatively surprised the market. Microsoft expects the slowdown in PC sales and rising energy costs to hurt operating margin, and the company has more or less introduced a hiring freeze to keep costs under control.

Economic uncertainty is hurting sales of PCs as well as advertising revenue, which affected Microsoft’s Search and LinkedIn businesses. CFO Amy Hood:

“While we are not immune, of course, from macroeconomic impacts, we really feel good about the businesses we are investing in, the strong growth rate, the position in the market”.

Hood said higher energy prices are increasing the cost of delivering cloud services, mainly in Europe, an issue that is having a greater impact than Microsoft had expected. She anticipates that will continue into the second half of the company’s fiscal year.

Credit Suisse reiterated with Outperform rating at Credit Suisse on Wednesday, but cut target price to US$ 365 from US$ 400. CS revised down their revenue 2023 and 2024 full-year revenue/EPS estimates for the company, saying that they believe Microsoft’s full-year guidance for its commercial business to grow approximately 20% year-on-year implies a meaningful slowdown in the deceleration in Azure growth in the second half of the year into the mid-30% range.

On Tuesday, Alphabet shares down 7% on big Q3 miss. It turned out that Snap’s worse than expected results last week were a good leading indicator on Google’s performance in Q3. Revenue came in at US$ 69.1bn vs US$ 70.8bn and operating income was US$ 17.1bn vs est. US$ 19.7bn as the operating margin is coming under significant pressure q/q and y/y. Revenue growth in Q3 at 6% y/y is the slowest pace since Q2 2020.

Revenue growth slowed to 6% from 41% a year earlier as the company contends with a continued downdraft in online ad spending. Other than one period early in the pandemic, it’s the weakest period for growth since 2013.

At Alphabet’s most important financial engine, the search and related businesses, sales rose less than analysts estimated as spiralling inflation crimped growth in digital advertising. Philipp Schindler, chief business officer for Google, said the company saw a pullback in spend on search ads from certain areas such as insurance, loans, mortgage and cryptocurrencies.

YouTube ad revenue slid about 2% to US$ 7.07bn from US$ 7.21bn a year ago. Analysts were expecting an increase of about 3%. Alphabet reported overall advertising revenue of US$ 54.48bn during the quarter, up slightly from the prior year.

Google also cancelled the next generation of its Pixelbook laptop and cut funding to its Area 120 in-house incubator. And last month, Google said it would be shuttering its digital gaming service Stadia.

However, these could be short-term cyclical headwinds, driven by the macroeconomic environment such as FX rates. These issues are cyclical and long-term story could be different, as the company increased investments into R&D, marketing, and headcount. Mark Mahaney, an analyst with Evercore ISI, wrote in a note Wednesday:

“It’s surprising to us that Google continued to hire and invest aggressively throughout Q3, knowing that macro trends were deteriorating. Instead, perhaps Google should have frozen hiring and cut back expansion plans in [the first half of 2022] as Amazon did.”

Tomorrow, AAPL 0.00%↑ and AMZN 0.00%↑ will report their earnings and we will get another move in markets.