Tesla is really an unusual stock

Why is TSLA still hot despite the bad news and earnings below consensus?

Tesla shares are down almost 20% in the past 3 weeks. Tesla shares sank 6% afterhours on Wednesday with the released of uninspiring financial reporting and, then, the shares fell another 10% on Thursday after SpaceX launched its Starship rocket for the first time, but fell short of reaching space after exploding in mid-flight. The equity moved from US$ 200 at the end of March to close to US$ 160 yesterday, thus falling almost 20% in 3 weeks.

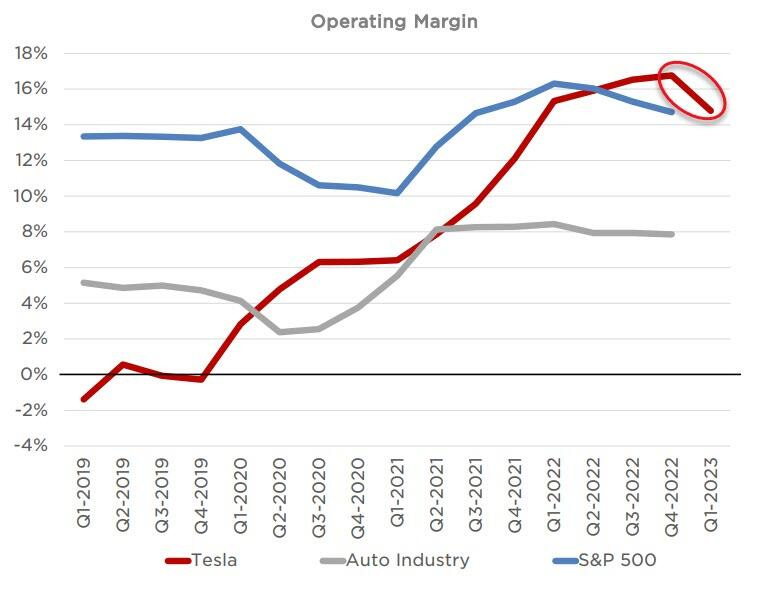

The EV giant’s results showed its operating margins fell, and this is in the face of Tesla saying more EV price cuts are to come. Elon Musk has indicated he is willing to sacrifice Tesla’s profits in the short term in an aggressive push for market share, with the aim of making more money later when the company’s cars are fully autonomous and can earn extra fees by operating as “robotaxis”. Musk’s comments on the earnings call on Wednesday pushed Tesla shares lower, adding pressure on top of worries about falling demand (FT).

Musk said on March 1st, investor day:

The desire for people to own a Tesla is extremely high, the limiting factor is their ability to pay for a Tesla.”

What added to Tesla’s continued margin squeeze is that it slashed the base price of its Model 3 to below US$ 40,000 in the US for the first time in years – That’s a US$ 7,000 cut from the start of the year.

Not surprising that few analyst changed the share target price:

RBC cuts target price to US$ 212 from US$ 217, citing the price cuts made by the company is weighing down the margins despite higher volumes of sale.

Citi is neutral and cut to US$ 175 from US$ 192. Tesla’s Q1 margin miss confirms that price cuts were not offset to the extent previously expected. For investors, an entry point will require more conviction on near-term demand “since some of the softness could be related to company specific factors/exposures”.

TD Cowen is market perform with target price cut to US$ 150 from US$ 170. Price reductions were a headwind to gross margins this quarter. Cutting estimates on a lower ASP and margin outlook.

Piper Sandler remains overweight wit target price at US$ 300. The weakness in shares can be attributed to a decline in gross margins, “owing largely to Tesla’s aggressive pricing strategy”. “It’s wrong to focus on gross margin miss” and Tesla should bounce back once the dust settles.

Finally, Goldman Sachs view on Tesla is that the short-term equity price upside gone. 1) "We are Buy rated on Tesla shares. We lower our 12-month price target to US$ 185 from US$ 210, which is based on 45X (unchanged) applied to our updated Q5-Q8 EPS estimate including SBC"; 2) "We lower our EPS estimates for 2023/24/25 including SBC to US$ 2.20/US$ 3.65/US$ 4.75 from US$ 3.20/US$ 4.66/US$ 6.00 driven primarily by lower ASPs and automotive gross margins..."; 3) "As an illustrative analysis to frame downside risk, if Tesla were to trade at a ~25X multiple (roughly a PEG of 1X) on our new 2024E EPS estimate including SBC, its implied valuation would be roughly US$ 90."

Goldman Sachs's Scott Feiler then asked: "Why is it not down more?". Feiler notes that the focus from bears is on both the gross margins miss (~170 bps) and the FCF miss. The one counterpoint he highlights is "almost all investors we spoke to expected some level of GM miss, and the question was just magnitude."

We think the bigger focus should actually be for peers/industry margin dynamics, as they spent the first few paragraphs of their release/presentation talking not of slowing demand, but of looking at unit economics from their peers and seeing this as an opportunity for themselves.

Feiler added that they think TSLA is making a clear attempt to pressure peers:

They lowered prices in the US ~6 times already this year, the question is why? They highlight that they “see this year as a unique opportunity for Tesla. As many carmakers are working through challenges with the unit economics of their EV programs, we aim to leverage our position as a cost leader. They make it further clear this is a market share grab by saying “Our near-term pricing strategy considers a long-term view on per vehicle profitability given the potential lifetime value of a Tesla vehicle.”

In the meantime, the competitor BYD announced this week that they are launching a ~US$ 11,400 electric vehicle. Morgan Stanley said “No wonder Tesla keeps cutting price.”

So far, the rush to sell as many cars is working: Tesla closed its first quarter with record deliveries hitting over 423,000 units worldwide, but that’s still less than what the automaker produced (440,000): the stock of unsold cars increased by another 18,000. In addition to those accumulated in previous quarters, for a total of 78,000 unsold cars. This is in a context of price reduction (and so decreasing margins)! Compared to the prices of a year ago, Tesla's average car prices have fallen by 29%, and car stocks continue to rise... This means that there is no demand. Tesla lowers prices, but for now, sales volumes are not increasing as Musk would like.

Let’s take a quick look at the reported numbers:

Revenues US$ 23.33bn (exp. US$ 23.29bn); up 24% Y/Y

Adj. EPS 0.85 (exp 0.85); down 21% Y/Y

Operating margin decreased Y/Y to US$ 2.7bn (-11.4%) in Q1, down from 16% the previous period and 19.2% a year ago (despite lithium price falling 72%)

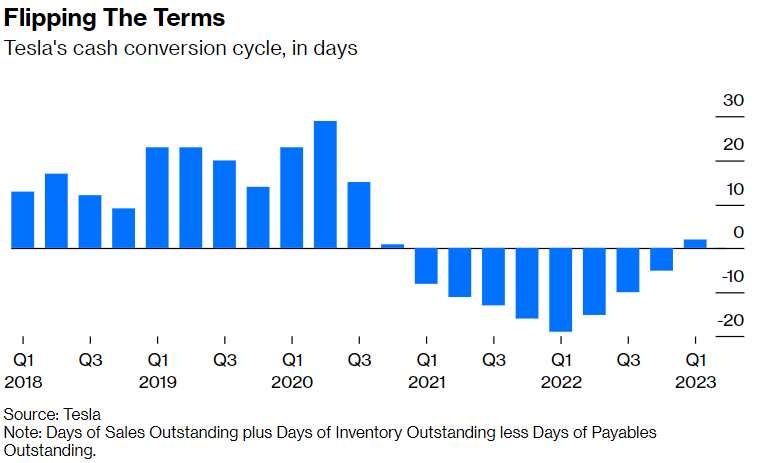

Free Cash Flow US$ 441m, missing estimates at US$ 3.24bn (down 80% Y/Y). Without the regulatory credits this quarter, Tesla’s FCF would have been negative.

Tesla still sees FY production 1.80m vehicles (exp. 1.84m)

Automotive gross margin was missing for the first time in a while

Then, the day after the report, Tesla increased prices of its premium Model S and Model X SUVs in the US by US$ 2,500, or about 2% to 3%. That comes two days after the EV maker lowered the prices of its Model Y SUV and Model 3 sedan for a second time this month.