Treasuries, recession and market rebound. What the Street thinks

A short recap from the main guys in the Street

Treasuries overview

The Bloomberg US Treasury Total Return Index has lost about 13% this year, almost four times as much as in 2009, the worst full year result on record for the gauge since its 1973 inception. This has taken the 10-year treasury benchmark yield back close to the round 4.00% level that is a significant psychological milestone and near the 14-year high for the benchmark.

The next key test for yields is Thursday’s US CPI data point than tomorrow’s FOMC minutes, which may contain few surprises, given nearly all Fed members are on the same page in supporting the current tightening regime.

Volatility has skyrocketed and hedging operations are as expensive as ever.

Institutional investors (governments, insurance companies, pension funds) have been quitting buying bonds, also due to the currency-protection costs. Instead, some central banks became seller of treasuries. Especially in emerging markets, where banks are forced to sell USD to save their currencies.

This is the 4th worst bear market for bonds in history and yet there are no buyers.

At last, Fed is continuing the QT. Its balance sheet will be reduced to US$ 5.9 trillion from US$ 8 trillion before 2025, reducing furthermore the demand on the market.

Everywhere you turn, the biggest players in the US $23.7 trillion US Treasuries market are in retreat.

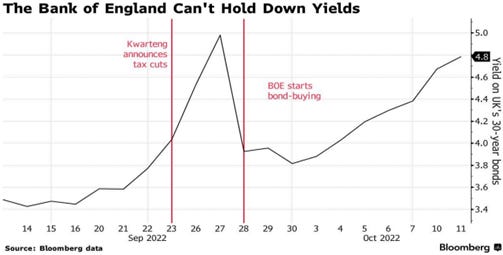

In UK, Tuesday 11th October was a rocky ride for markets, which were trying to post a rally until a steep sell-off developed late in the session as Bank of England Governor Andrew Bailey warned that UK pensions must get their house in order by Friday, sticking with the end date of the Bank of England’s emergency intervention.

On Wednesday morning, the FT reports that the Bank of England may be willing to extend those measures, helping to stabilize sentiment. In the meanwhile, Yields are rising again.

Fed pivoting & recession. Analysts opinions:

Goldman Sachs says it’s “too early” to price in a dovish pivot from the Federal Reserve as the economic outlook isn’t bad enough yet, and rates markets remain volatile. Fluctuations in the rates market have meant that expectations for potentially higher return on equities over relatively safer assets have been compressed, strategists including Cecilia Mariotti wrote in a research note Monday, maintaining an underweight on stocks. Speculation Fed policy will turn friendlier toward equities has seen the S&P 500 Index eke out gains from time to time over the past 12 months, but all those rallies have been sold into with the gauge making new lows every time.

JPMorgan Chase CEO Jamie Dimon joins recession crowd. Jamie Dimon told CNBC he expects a US recession in the next 6-9 months as the global economy faces "serious" headwinds. Europe is already in a recession. As for equities, the JPMorgan CEO said the S&P 500 "may have a ways to go" in its decline. "The S&P 500 could yet fall by another easy 20% from current levels. The next 20% would be much more painful than the first”. Financial Times

JPMorgan says investors should expect a 5% sell-off in the stock market on Thursday if CPI comes in above 8.3%. Thursday's CPI reading could spark a 5% sell-off in the stock market. That's if the inflation measurement comes in above 8.3%, which would be ahead of consensus estimates for an 8.1% reading. Alternatively, a CPI print below 7.9% could spark a 3% rally and bolster calls for a Fed pivot. Business Insider

Paul Tudor Jones is getting ready for a recession. The famous macro trader said in an interview yesterday that his trading firm is getting ready to deploy its recession playbook. The key dynamics according to Tudor Jones are recessions last 300 days, equities fall 10% on average, short-term bond yields will start to go down before bottom in equities, term premium will increase both in equities and bonds, earnings multiples will compress, and the Fed will either halt or slow rate hikings.

On earnings…

Stocks face brutal earnings season with all eyes on Apple: around 60% of respondents to the latest MLIV Pulse survey said the S&P 500 will be dragged lower because of poor earnings. About half said they expect equity valuations to pull back even further from their 10-year average.

US Banks to set aside US$ 4bn as loan loss provisions. As Q3 earnings season approaches, the largest US banks are expected to collectively increase their loan loss provisions by about US$ 4.5bn, according to analysts’ estimates from Bloomberg. The banks include JP Morgan Chase, Bank of America, Citigroup, Goldman Sachs, Wells Fargo and Morgan Stanley. FT notes that this is an indication that the banks are expecting to have to cover higher credit losses from bad loans as a result of the expected economic contraction; moreover, the KBW Bank Index (a benchmark stock index of the banking sector) has dropped about 22%, 2% more than the S&P 500 Index, which further reflects investors’ worries that credit losses will outpace increased interest income.

Ken Usdin, a banking analyst at Jefferies said:

“The overall economic outlook has deteriorated somewhat and therefore it would be natural to expect some incremental pick-up in bank reserving actions”.

On the other hand, US bank executives are confident on overall US credit quality, stating that defaults are below historical norms.

Bernstein - Earnings downgrades are almost halfway there in Europe? Bernstein Strategy team continue to think there is further downside for markets as earnings and outflows have not yet capitulated.

"A European earnings downgrade cycle on average lasts 8 months and we are 4 months in. 12m fwd EPS for the market is now down 5% from its June peak, the average peak to trough decline in 12m fwd EPS seen during past downgrade cycles is 12%, suggesting 7% more EPC cuts at the market level if this is an ‘average cycle’. However, if industries have to curtail gas consumption by 20-30% this could translate to a larger cut to earnings, we estimate in the 12-18% range. Some sectors have already seen peak to trough cuts in earnings in line with previous cycles, however, Materials, Financials, Communications, Consumer Discretionary, Industrials and Energy have not yet".

Morgan Stanley - Even Wilson could see stocks bouncing. Mike Wilson expects the market can chop back and forth and even drift higher before it becomes obvious that earnings forecasts are too high. Dynamics include deteriorating funds clashing with oversold markets, pervasive bearishness, and technical support at the 200-wk moving average.

JPMorgan’s Marko Kolanovic:

“The positive relative case for large cap UK stocks remains, as they trade at a record valuation discount, offer the highest dividend yield, and derive the bulk of their earnings base from overseas”.

Goldman Sachs trading desk – It’s not all doom and gloom.

We’re seeing the highest proportion of insider buying in Stoxx600 for 10 years.

Cash levels for mutual funds are extremely high, positioning in Europe is extremely low.

PE dry powder is at all-time highs.

Employment remains (thus far) sticky and high.

US equity futures position % open interest remains at lowest since GFC, vol control funds equity allocation at 5th 10y%ile. CTAs are now flipping to buy, which could contribute to a large right tail asymmetry.

But a separate note says that Goldman Sachs see retail near capitulation:

“After opening up their Q3 quarterly statements over the weekend, retail has finally blinked. Capitulation is near. This is the last standing asset owner, who has not sold, [and] is moving money right now”.

BofA clients were big buyers of US equities last week, adding a net US$ 6.1 bn. That's the third largest inflow since the bank started tracking the data in 2008, and analysts said it may suggest clients believe stocks are at a bottom. The bank's own view, however, is that not yet that rosy:

"Flows suggest investors believe market may have bottomed: client flows into US equities last week were 3rd-largest since '08 […] Our view? More volatility likely ahead".

Separately, BofA's strats out bullish on US small caps, particularly small-cap value (over growth).