US new home sales fell 12.6% & supply surged

New home construction will slow down

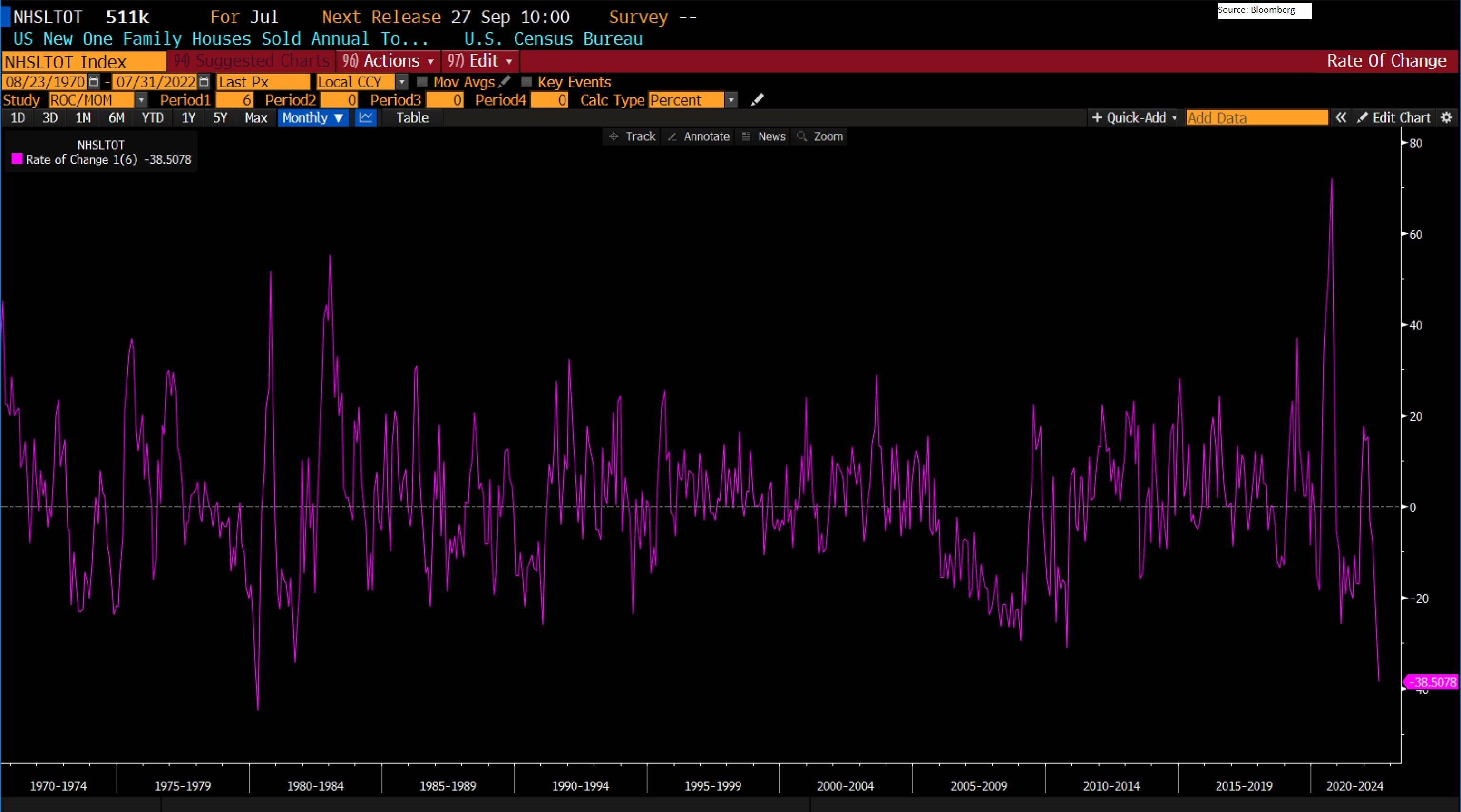

Yesterday, US new home sales fell 12.6% in July to 511k, beneath the expected 575k and the prior 585k, and as such printed the slowest pace of sales since January 2016 including pandemic lows. New home sales for the last six months at -39%: you have to go back to 1980 for a six-month fall greater than this.

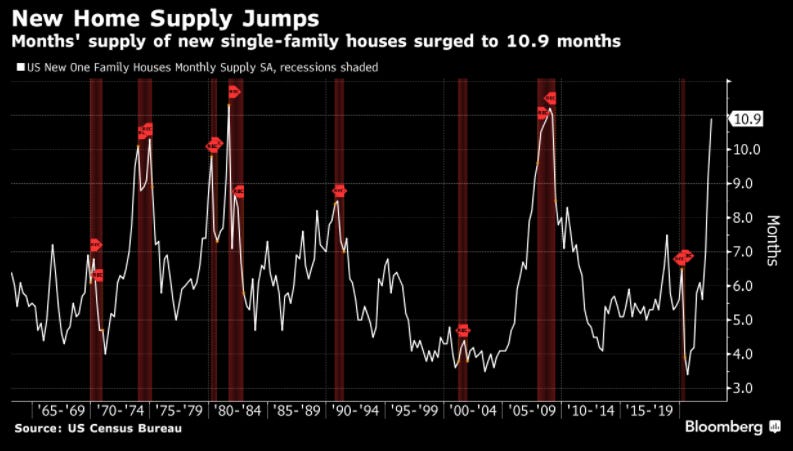

Additionally, new home supply rose to 10.9 months (previously 9.2 months), increasing for eight consecutive months, hitting its highest level since 2008. In other words, at the current sales pace it would take 10.9 months to exhaust the supply of new homes in the US, the most since 2008 and nearly double the figure at the start of this year. Every time monthly supply of new houses has exceeded 9 months a recession has ensued.

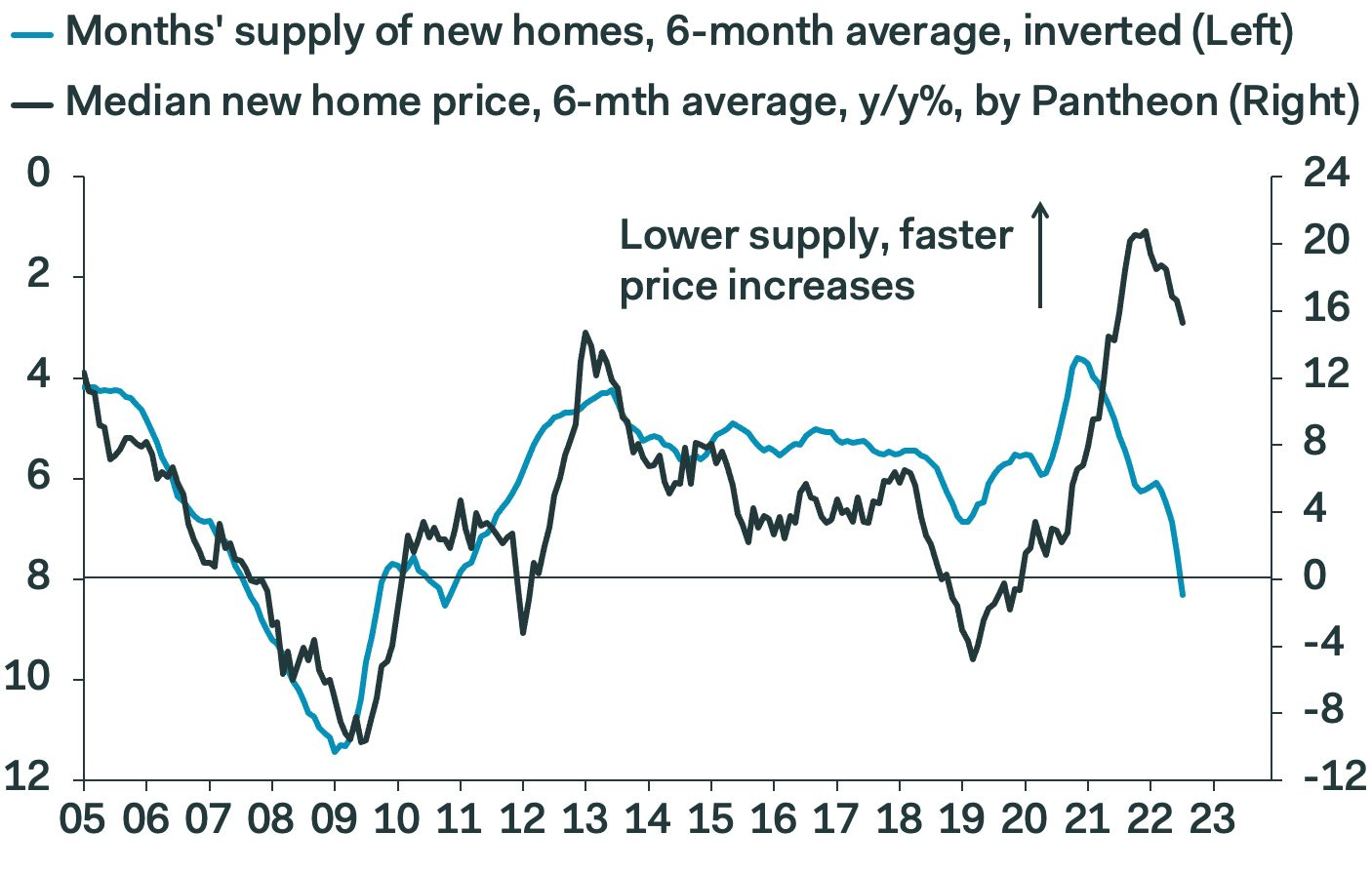

Oxford Economics note, “despite slowing sales and higher inventory, both median and average home prices rose sharply in July, after falling in June.” Continuing, the July data is the latest evidence of the continued deterioration in housing activity, and as such looking ahead, OxEco adds it “indicates there is downside risk to our forecast for a moderate sales decline in Q3. Significant price decreases will be needed to keep a floor under new homes sales.”

But as pointed out by Pantheon Macro, house prices are not decreasing sufficiently: “The housing market is in much worse shape than the Fed has been willing to admit. But policymakers have made it clear that inflation is their primary objective, and housing is collateral damage.”

The median new house price in July was US$ 439,400: +8.2% YoY (last month was US$ 402,400). While that was a deceleration from the double-digit growth seen early in the year, average house prices jumped 18.3% YoY in July.

In absolute terms, none of the houses sold last month were below US$ 200,000.

With this level of house prices, it is unlikely that we will see the house market collapse but Robert Frick, a corporate economist at Navy Federal Credit Union, is not so optimistic:

“Given builders are pulling back plans to construct more homes, we won't be building our way out of the current housing crisis for years”.

As inventories of new homes rise, a pullback in prices is probably coming, Frick said, although there's a limit to how low they can go given the cost of materials, land and labor that get baked into builders' costs.

Glenn Kelman, Redfin CEO (a full-service real estate brokerage), states that the housing market correction is being faster than expected due to the institutions participating into real estate. They made housing more like the stock market, where brokerages have to “race to the top” or “race to the bottom”.

He suggests prices could tumble faster than 2008 because investors are quicker to cut losses than somebody who is living in the home.

Finally, the Fed monetary policy is estimated to become even more aggressive in order to fight inflation, but its effect on the housing market is already observable.

Matthew Walsh, an economist at Moody’s, agrees:

“The Federal Reserve is getting what it wants. The housing market needed to cool, and higher interest rates were the only thing that was going to accomplish that.”

This resulted in higher mortgage interest rates (at 5%): the monthly mortgage payments necessary to buy a house have increased and buyers stopped searching for new houses. This is another reason why the home affordability is dropping.